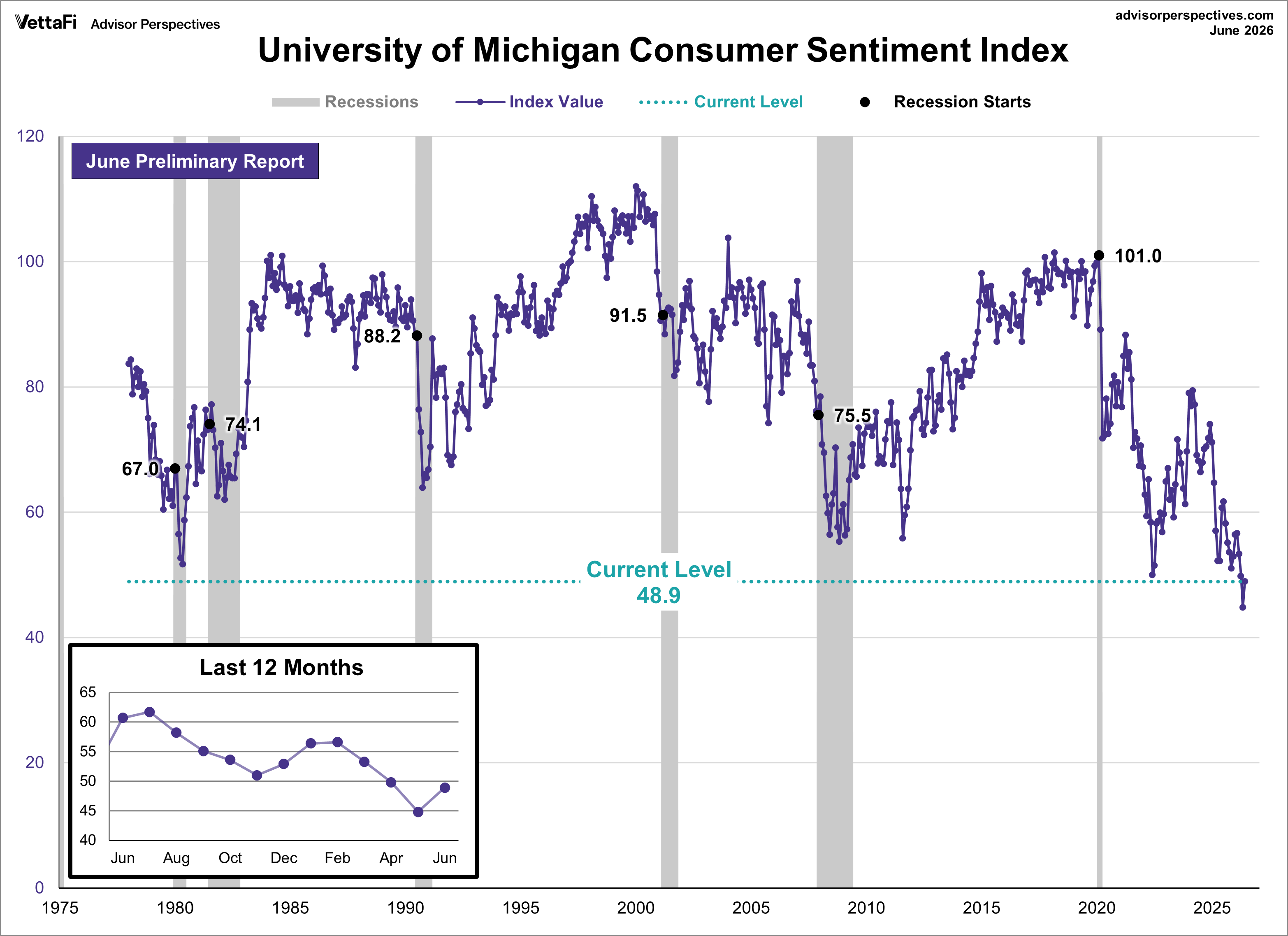

Consumer sentiment improved for the first time in four months but remains historically low amid ongoing inflation concerns. The preliminary June reading for the University of Michigan Consumer Sentiment Index came in at 48.9 marking a 9% (4.1 points) increase from April and beating the expected reading of 46.1.

Key Takeaways

- The University of Michigan Consumer Sentiment Index rose 9% to 48.9, beating the 46.1 forecast but remaining 41.6% below its historical 83.8 average.

- The current conditions index rose to 48.4 and expectations index rose to 49.3, beating forecasts despite dropping 25.3% and 15.1% year-over-year.

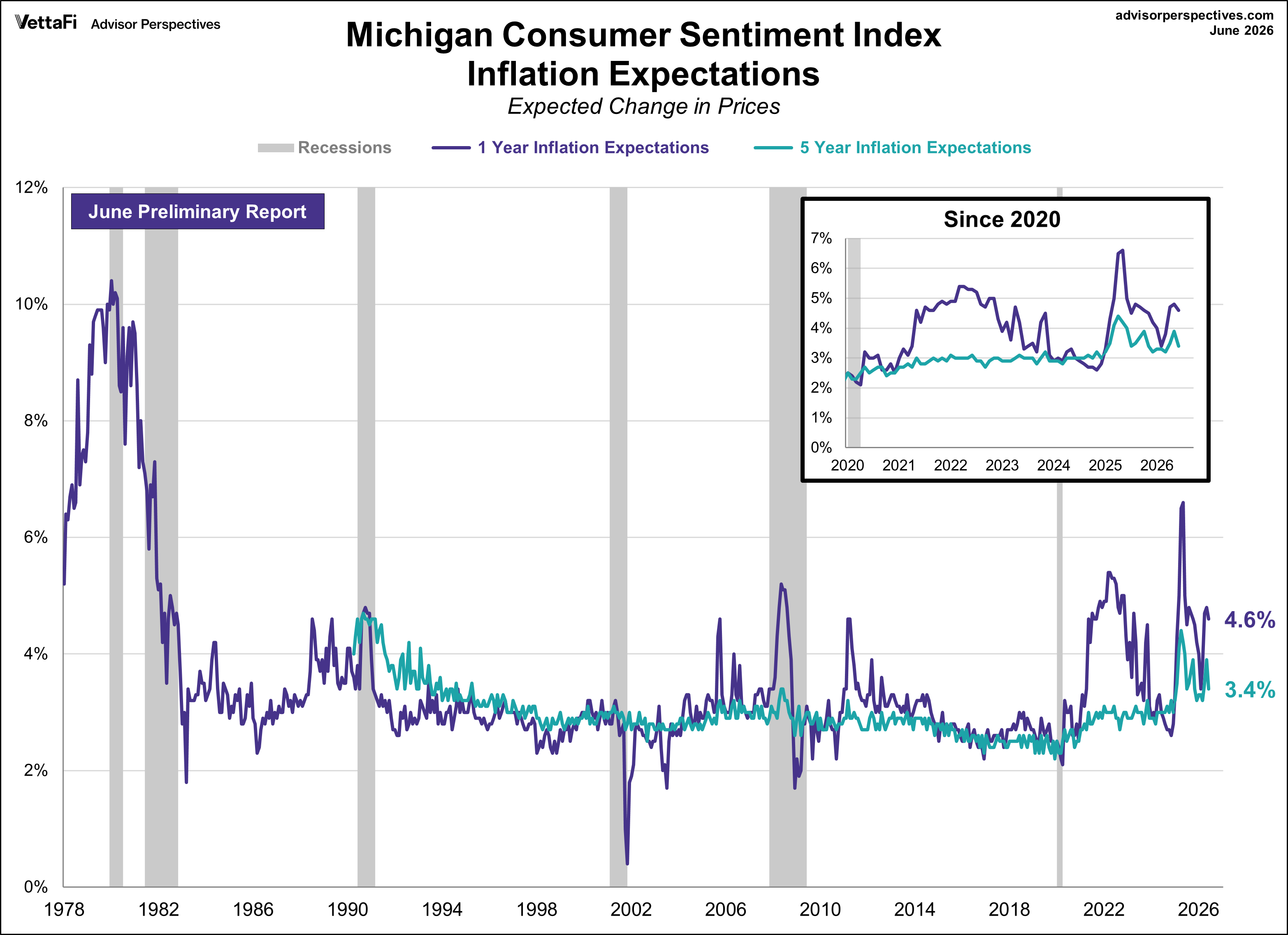

- Year-ahead inflation expectations fell to 4.6% and long-run expectations dropped to 3.4%, remaining notably higher than readings from 2024.

Joanne Hsu, the director of surveys, made the following comments:

This month, consumer sentiment ticked up about four index points, or 9%, with consumers experiencing some relief due to the early-month easing in gasoline prices. This measured improvement in sentiment was widespread, seen across age, education, and political party. Lower-income consumers exhibited a particularly strong sentiment increase, consistent with the fact that gasoline comprises a larger share of their budgets. Overall, assessments and expectations of personal finances and business conditions all rose this month. Even with June’s early gains, however, views of the economy are still relatively dour. Sentiment is currently 13% below January 2026 and 19% below a year ago, as consumers remain focused on kitchen table issues. They feel burdened by the recent escalation in inflation and worry that higher inflation could remain stubborn going forward, particularly in the short run. Interviews for this release were completed between May 19 and June 8.

Background on the University of Michigan Consumer Sentiment Index

The Michigan Consumer Sentiment Index is a monthly survey of consumer confidence levels in the U.S. with regards to the economy, personal finances, business conditions, and buying conditions, conducted by the University of Michigan. There are two reports released each month; a preliminary report released mid-month and a final report released at the end of the month.

The chart below provides a long-term perspective on this widely watched indicator. We have highlighted the index's value at the start of each recession. The current level of 48.9 is below the index's value at the start of all six recessions since its inception.

To put today’s report in historical context, consumer sentiment is currently 41.6% below its average reading of 83.8 (arithmetic mean) and 40.8% below its geometric mean of 82.5, based on data dating back to 1978.

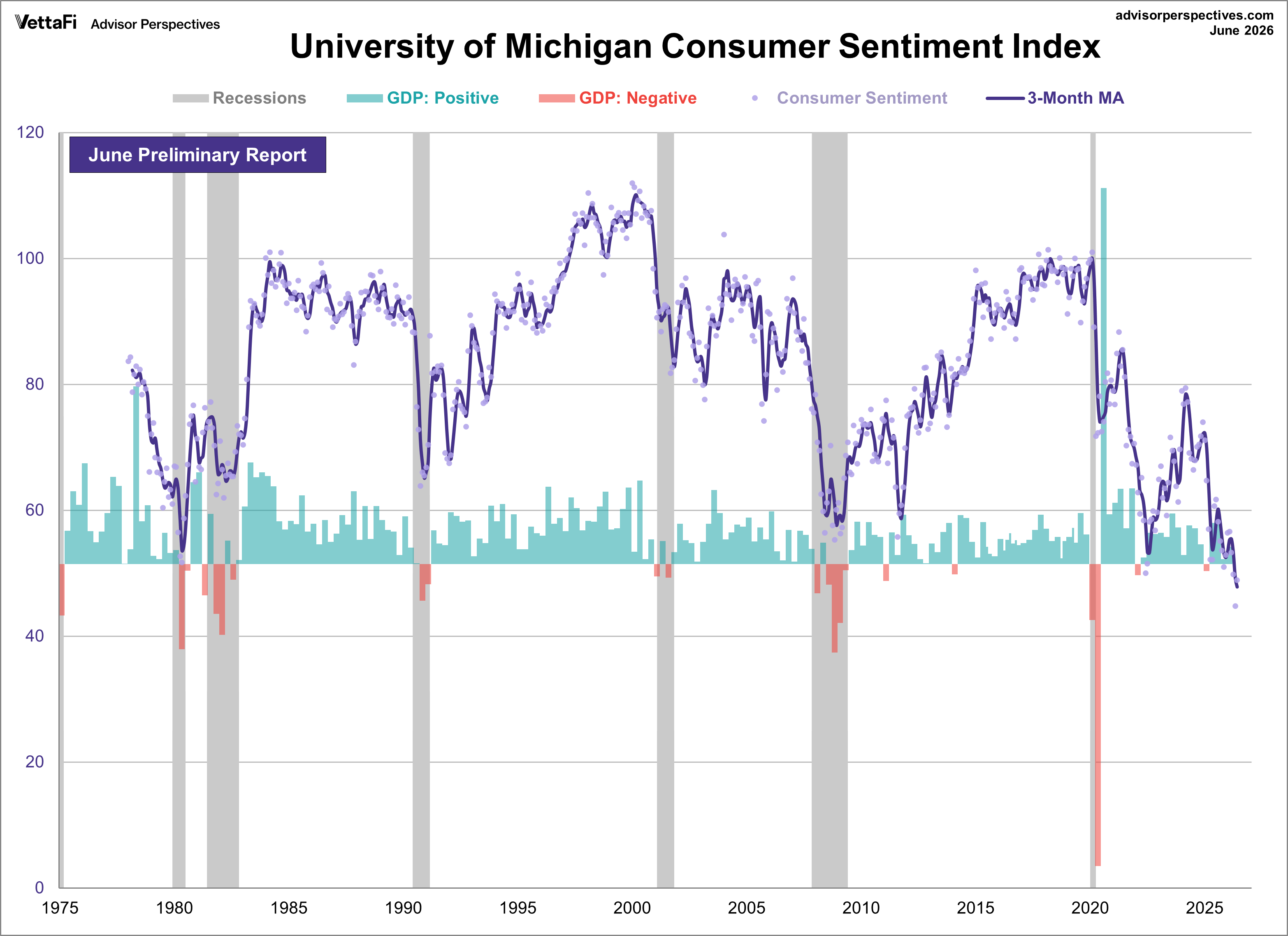

To visualize the volatility and its impact on the broader economy, the following chart includes a three-month moving average and real GDP. Historically, prolonged periods where the moving average remains at these depressed levels have closely correlated with negative GDP growth (the red bars below).

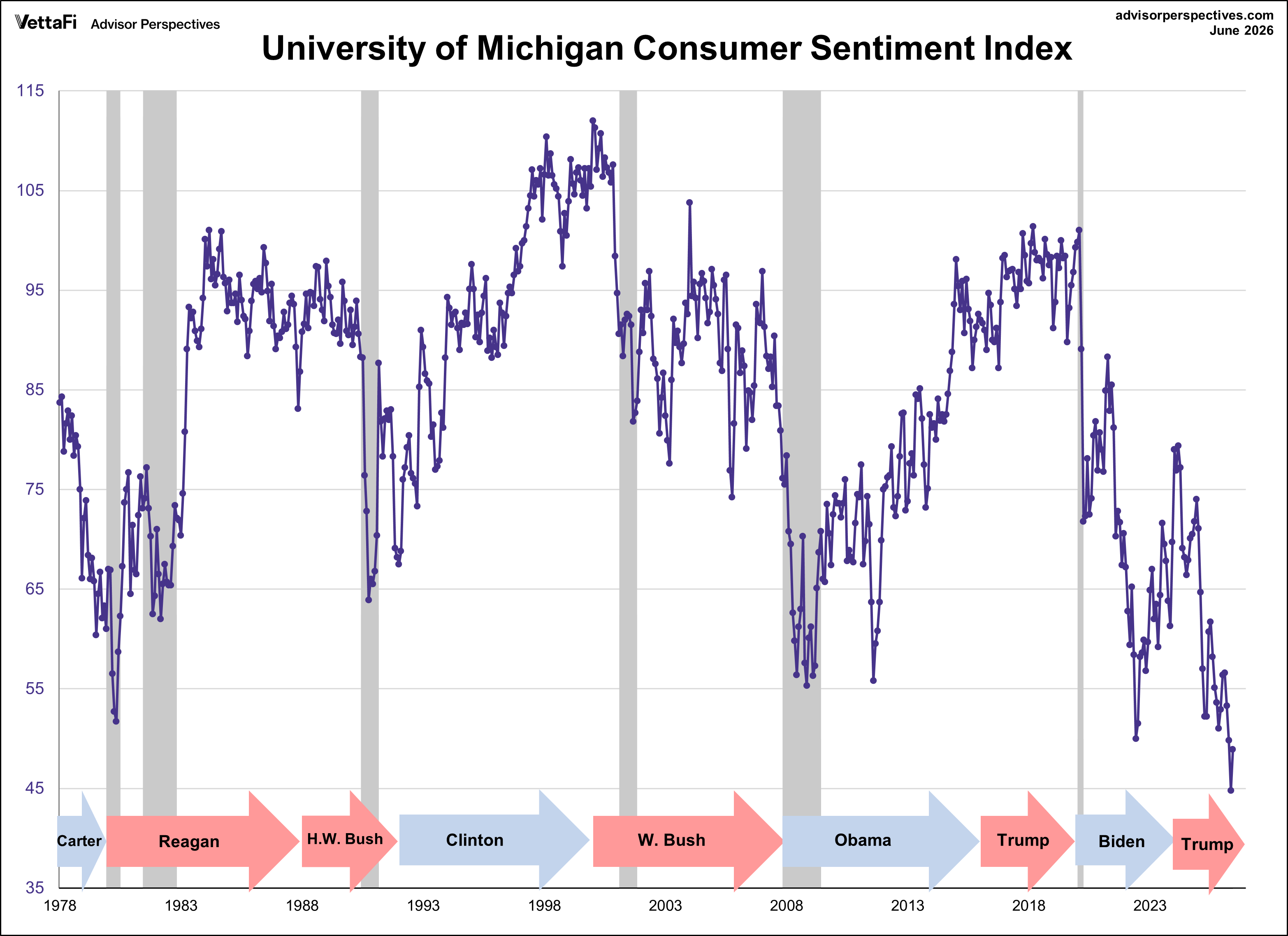

The Political and Presidential Lens of Consumer Sentiment

Each month, the survey results highlight sentiment within each political party. Sentiment is often viewed through a partisan lens, but the data shows that sentiment has fluctuated both positively and negatively under both Republican and Democratic administrations. As the chart below illustrates, the current "plunge" is a rare moment of bipartisan agreement, with declines seen across the political spectrum as energy costs hit every household.

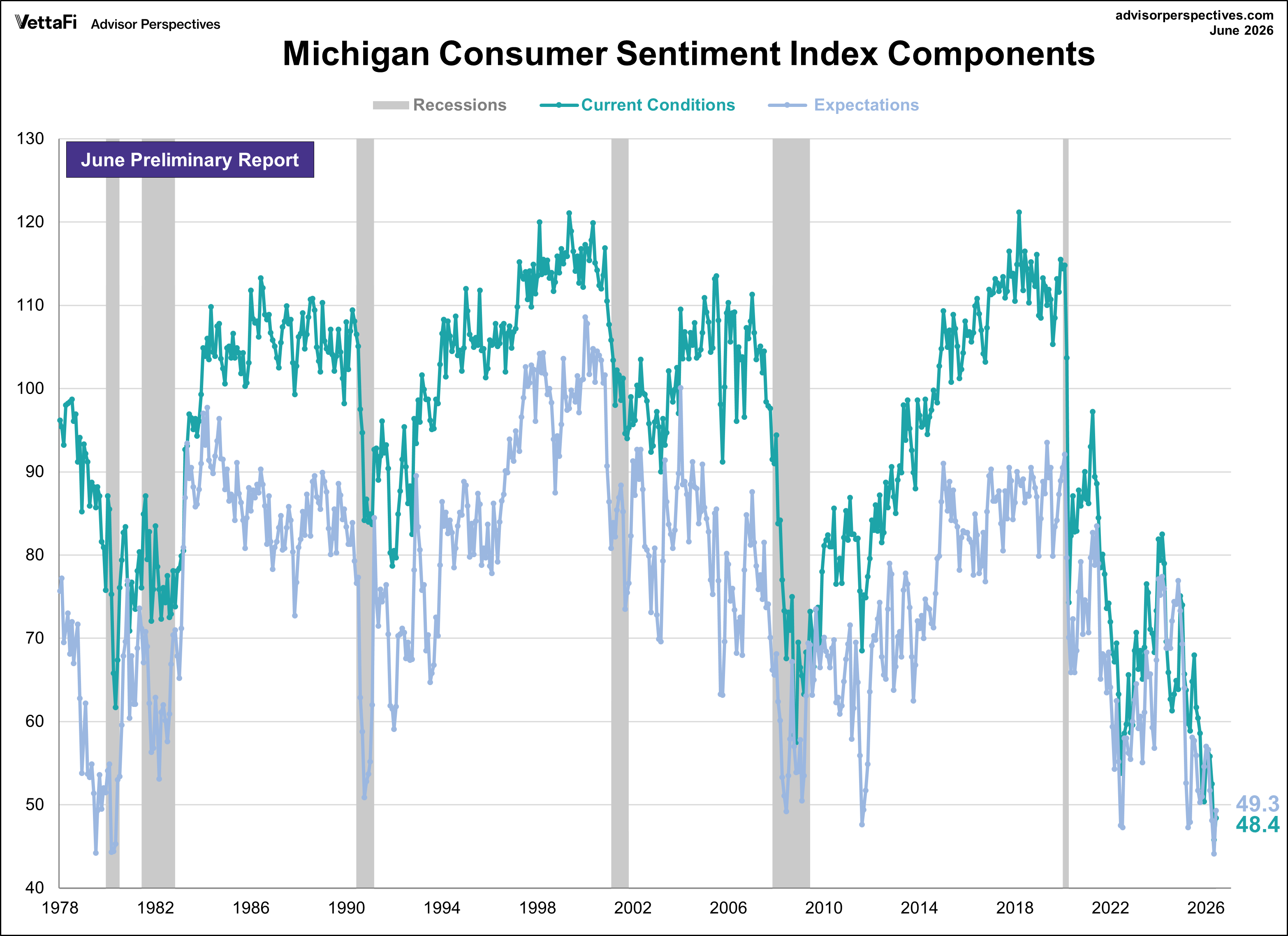

University of Michigan Consumer Sentiment Index: Components

The Michigan Consumer Sentiment Index consists of two sub-indexes: the Current Economic Conditions Index (CECI) and the Consumer Expectations Index (CEI). The CECI reflects consumers' views of their current financial situation and the overall economy, while the CEI gauges their outlook for the future.

-

Current Economic Conditions (CECI): Rose for the first time in four months to 48.4. This represents a 5.7% increase from the previous month but a 25.3% drop from a year ago. The latest reading was higher than the forecast of 46.2.

-

Consumer Expectations (CEI): Rose for the first time in five months to 49.3. This represents an 11.8% increase from the previous month but a 15.1% drop from one year ago. The latest reading was higher than the forecast of 44.3.

University of Michigan Consumer Sentiment Index: Inflation Expectations

Year-ahead inflation expectations inched down from 4.8% in May to a still-elevated 4.6% this month. The current reading substantially exceeds the 3.4% reading seen in February 2026 prior to the start of the Iran conflict, along with all 2024 readings. Long-run inflation expectations fell back from 3.9% last month to 3.4% in June, remaining notably higher than the 2.8% to 3.2% range seen in 2024.

The next update to this report will be published on June 26th.

Other Sentiment Indicators

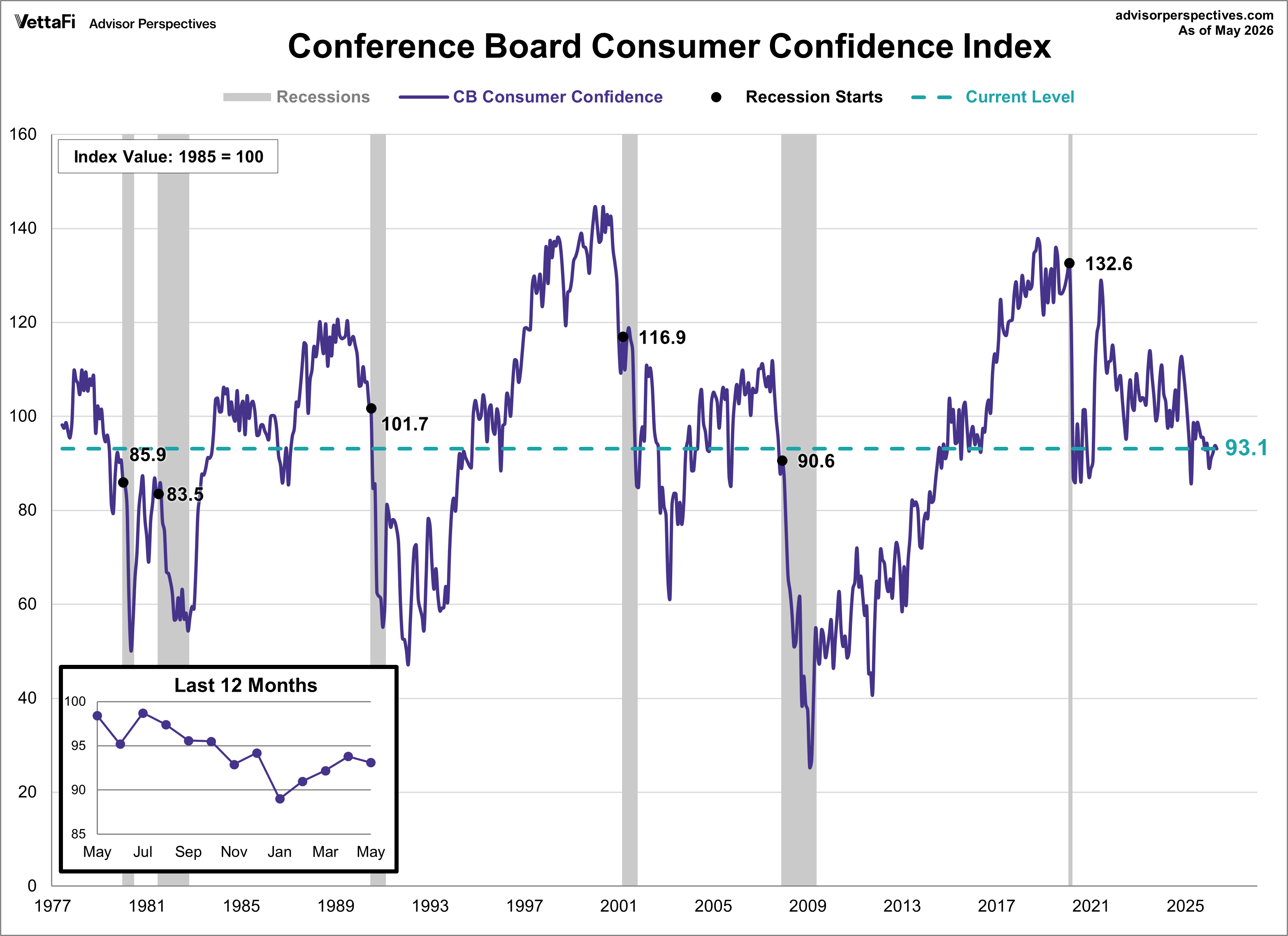

For an additional perspective on consumer attitudes, see the most recent Conference Board's Consumer Confidence Index. Both indexes gauge consumer attitudes toward the current and future strength of the economy. However, the Consumer Confidence Index is more influenced by employment and labor market conditions while the Michigan Sentiment Index is more focused on household finances and the impact of inflation.

The Conference Board index is the more volatile of the two, but the broad pattern and general trends have been remarkably similar to the Michigan index.

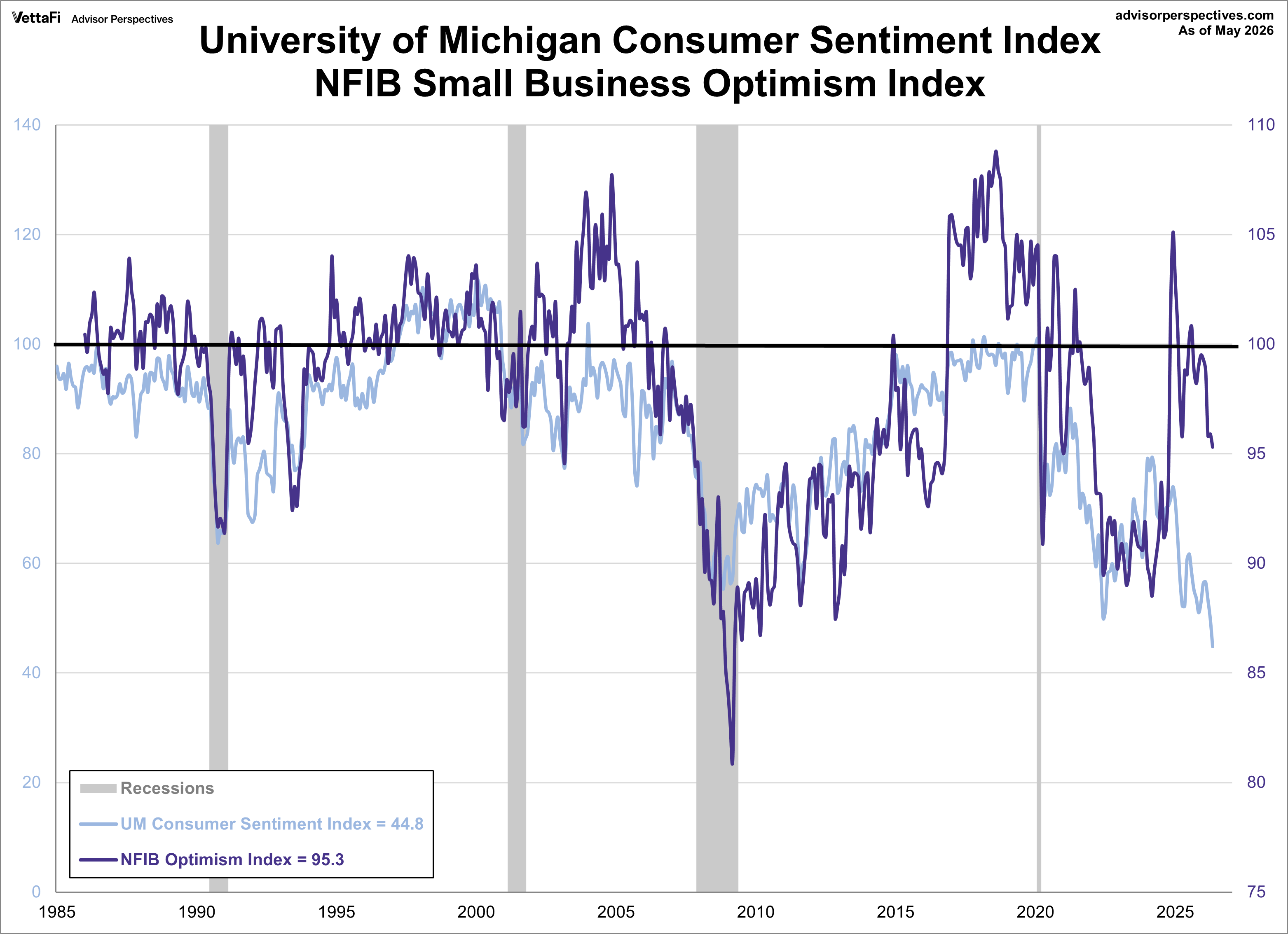

And finally, the prevailing mood of the Michigan survey is also similar to the mood of small business owners, as captured by the NFIB business optimism Index (monthly update here).

ETFs associated with sentiment include: Consumer Discretionary Select Sector SPDR Fund (XLY).

Read more updates by Jen Nash