Guggenheim Investments

2024 Election Uncertainty Could Drive Fixed-Income Outperformance

Rising economic policy and geopolitical uncertainty may favor higher quality fixed income in this election year.

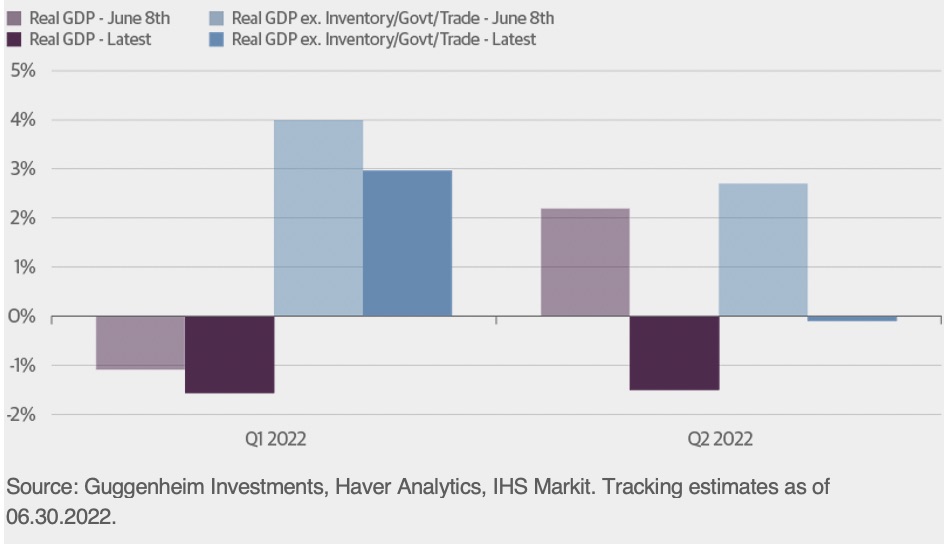

First Quarter 2024 Fixed-Income Sector Views

History shows that when the Federal Reserve (Fed) is paused and easing, longer duration higher quality fixed income has outperformed riskier assets, as well as money market instruments.

Macro Markets Podcast Episode 47: Investing as the Fed Prepares to Start Rate Cuts

Matt Bush and Evan Serdensky share their updated outlook following the latest FOMC meeting and the January jobs report.

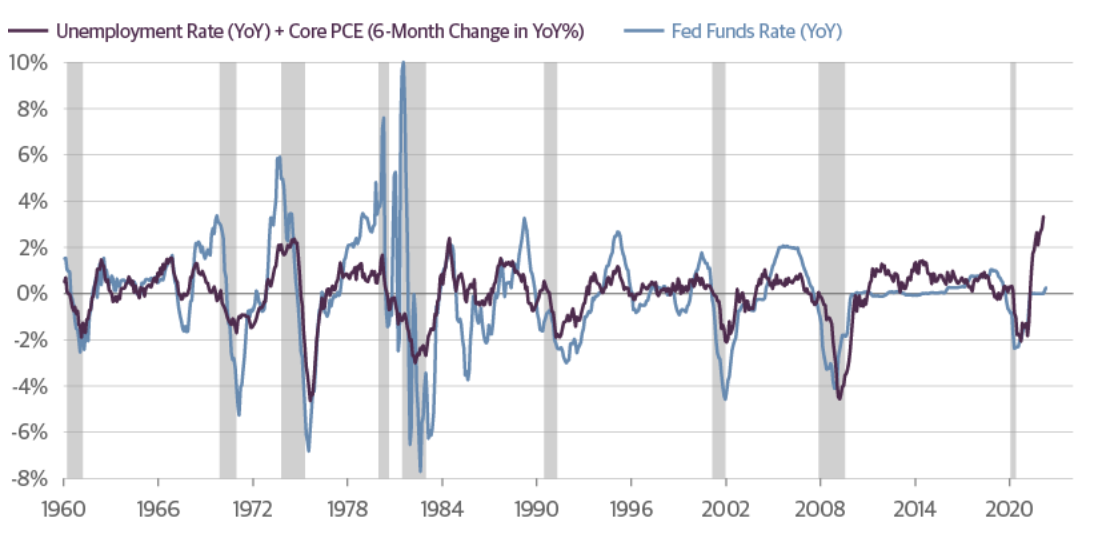

Learning from Turning Points in Monetary Policy

History shows that monetary policy drives investment performance. When the Federal Reserve (Fed) hikes or cuts the fed funds target rate in response to economic conditions—or stays on hold while it assesses the data—performance will differ by sector.

Higher-Quality Leveraged Credit Should Benefit from Fed Easing Cycle

Implications for credit investors.

11 Macroeconomic Themes for 2024

Guggenheim Investments’ Macroeconomic and Investment Research Group identifies 11 macroeconomic trends we believe are likely to shape monetary policy and investment performance this year.

Macro Markets Podcast Episode 45: Macro and Market Outlook for 2024

Anne Walsh joins Macro Markets to discuss opportunities and risks in what promises to be an eventful 2024.

Positioning for the Fed Pivot

Steve Brown, Chief Investment Officer, Total Return and Macro Strategies, shares insights on Fed policy and our house view on the possible pace and size of rate cuts going forward.

Policy Conditions Are Tighter Than They Appear

Anne Walsh, Chief Investment Officer for Guggenheim Partners Investment Management, joins CNBC to discuss Federal Reserve policy and its effect on credit markets heading into 2024.

Macro Markets Podcast Episode 44: Corporate Credit Review and Preview

Maria Giraldo discusses the performance of the corporate credit sector this year and the rationale for our cautiously optimistic outlook for 2024.

Fourth Quarter 2023 Fixed-Income Sector Views

In this issue of Fixed-Income Sector Views, our Sector Teams identify positive technical trends that have helped to support spreads, but remain vigilant for signs of credit deterioration as the slowing economy and the bite of higher rates start to be felt by issuers.

Macro Markets Podcast Episode 43: Post-FOMC/Jobs Report Update

Adam Bloch, Portfolio Manager on our Total Return team, and Matt Bush, Guggenheim Investments' U.S. Economist, update our economic and market outlook.

Technical Support Remains Strong but Fundamental Pressures to Grow in 2024

Credit challenges to come as the economy slows.

Third Quarter 2023 Fixed-Income Sector Views

Recent data and policy developments have fallen firmly in the soft-landing camp, and market performance has reflected this shift. Notwithstanding recent stronger-than-expected economic activity, we continue to believe a downturn is in the pipeline.

Credit is the Next Shoe to Drop

Anne Walsh, Chief Investment Officer of Guggenheim Partners Investment Management, joins Bloomberg TV to discuss the latest inflation data, the economic cycle, and portfolio positioning.

Use This 'Goldilocks Market' to Prepare for Its Eventual End

Talk of Goldilocks has taken hold in the markets, and with it the risk-taking allure of not-too-hot and not-too-cold investing conditions.

Macro Markets Podcast Episode 38: Value and Nuance in CMBS

Karthik Narayanan, Head of Securitized Credit for Guggenheim Investments, and Tom Nash, a director on our Commercial Mortgage-Backed Securities (CMBS) sector team, join Macro Markets to discuss drivers of performance, current conditions in real estate, and where they are finding value in CMBS and in other types of structured credit.

Quarterly Macro Themes Research Spotlight on What’s Next

Quarterly Macro Themes, a quarterly publication from our Macroeconomic and Investment Research Group, spotlights critical and timely areas of research and updates our baseline views on the economy.

Bond Investors Getting Paid for Patience

Anne Walsh, Chief Investment Officer for Guggenheim Partners Investment Management, joins Bloomberg TV to discuss fixed-income market opportunities, managing climate change risk, and the Fed’s path forward.

Macro Markets Podcast Episode 36: "It's a bond picker's market."

Anne Walsh, CIO for Guggenheim Partners Investment Management, discusses drivers of returns going forward. She also offers advice to young women looking to make a career in asset management.

Macro Markets Podcast Episode 35: A Deep Dive into Municipal Bonds

Allen Li, Managing Director and Head of Guggenheim Investments' Municipal Bond Sector Team, explains the structure and characteristics of the $4 trillion municipal market, the importance of technical dynamics, and where he is finding value.

Second Quarter 2023 Fixed-Income Sector Views

Markets are still facing uncertainties regarding the impact of the Federal Reserve’s aggressive rate hikes and quantitative tightening, a potential economic slowdown, and the likelihood of other unforeseen consequences of financial disintermediation.

Macro Markets Podcast Episode 34: Risk/Reward in High Yield/Bank Loans

Tom Hauser, Co-Head of Corporate Credit, discusses his current views on opportunity in leveraged credit. Economist Paul Dozier updates on the latest economic data.

A Vast Market in Private Credit

Anne Walsh, CIO of Guggenheim Partners Investment Management, joins Bloomberg TV from the Milken Global Conference to discuss the implications of ongoing issues in fixed income and how capital rationing favors private credit.

First Quarter 2023 Fixed-Income Sector Views

Valuations have reset after a volatile year.

10 Macroeconomic Themes for 2023

Guggenheim Investments’ Macroeconomic and Investment Research Group identifies 10 macroeconomic trends likely to shape monetary policy and investment performance this year.

Market Conditions Favor a Move Up in Credit Quality

Anne Walsh, Chief Investment Officer for Guggenheim Partners Investment Management, joined Bloomberg TV in Davos to discuss the outlook for credit as recession nears.

Minerd on the Fed and Investing Heading into 2023

Scott Minerd, Global CIO for Guggenheim Partners and Chairman of Guggenheim Investments, joins the year-end episode of Macro Markets on Fed Day for a wide-ranging discussion of the Federal Reserve’s execution of monetary policy, economic conditions, the investment landscape for risk assets, portfolio strategy, and more.

Fixed-Income Pain Giving Way to Opportunity

Anne Walsh, Chief Investment Officer for Fixed Income, on the economic and credit cycle, and on risk and opportunity across the fixed-income landscape.

Fixed-Income Sector Views

While the path to get us here has been painful, investable yields have the potential to meet the return objectives of pension plans, insurance companies, or other investors that may have been sitting on the sidelines—or taking undue risk within fixed income in a reach for yield.

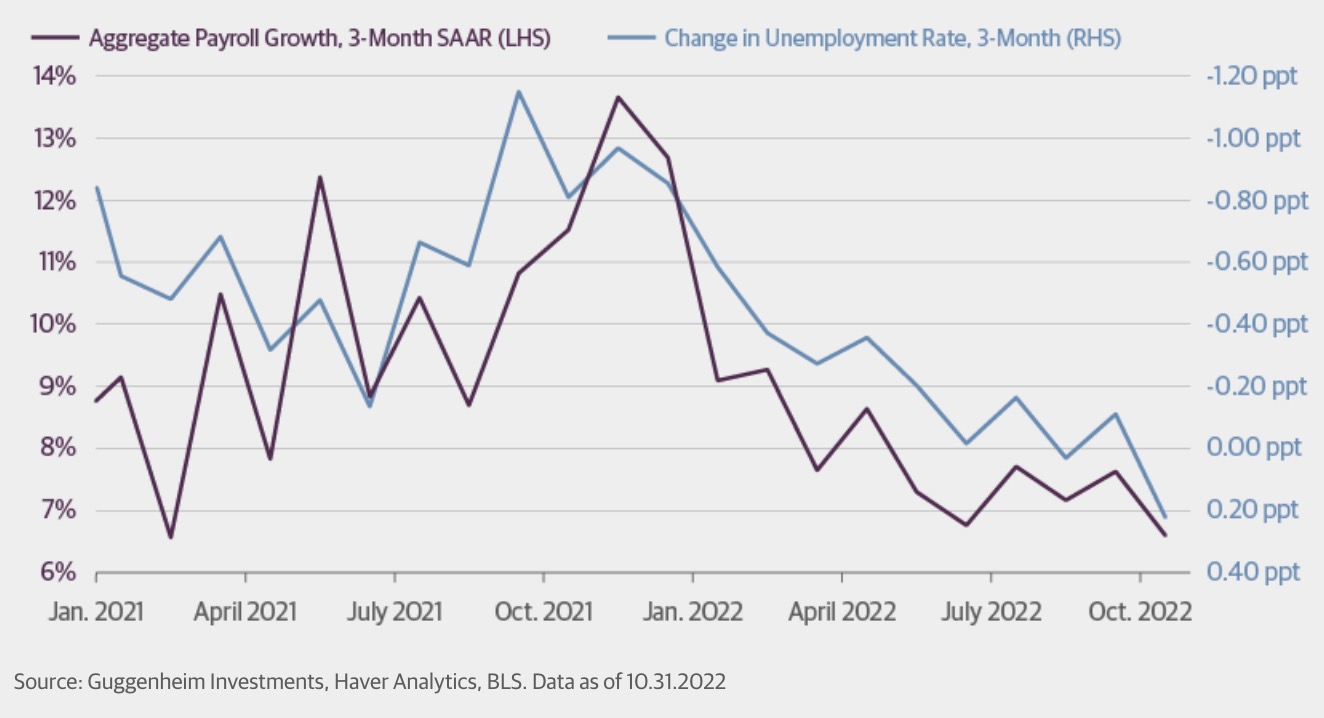

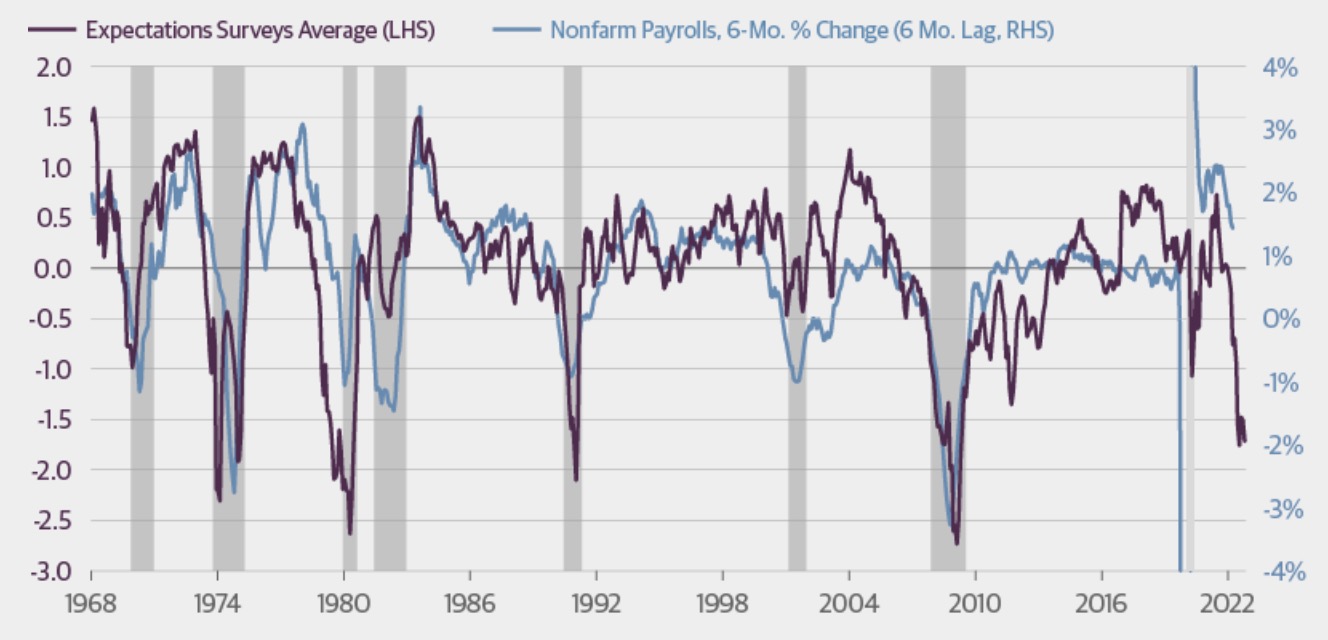

The Jobs Data Trend is Duration’s Friend

October jobs data suggests a cooling labor market.

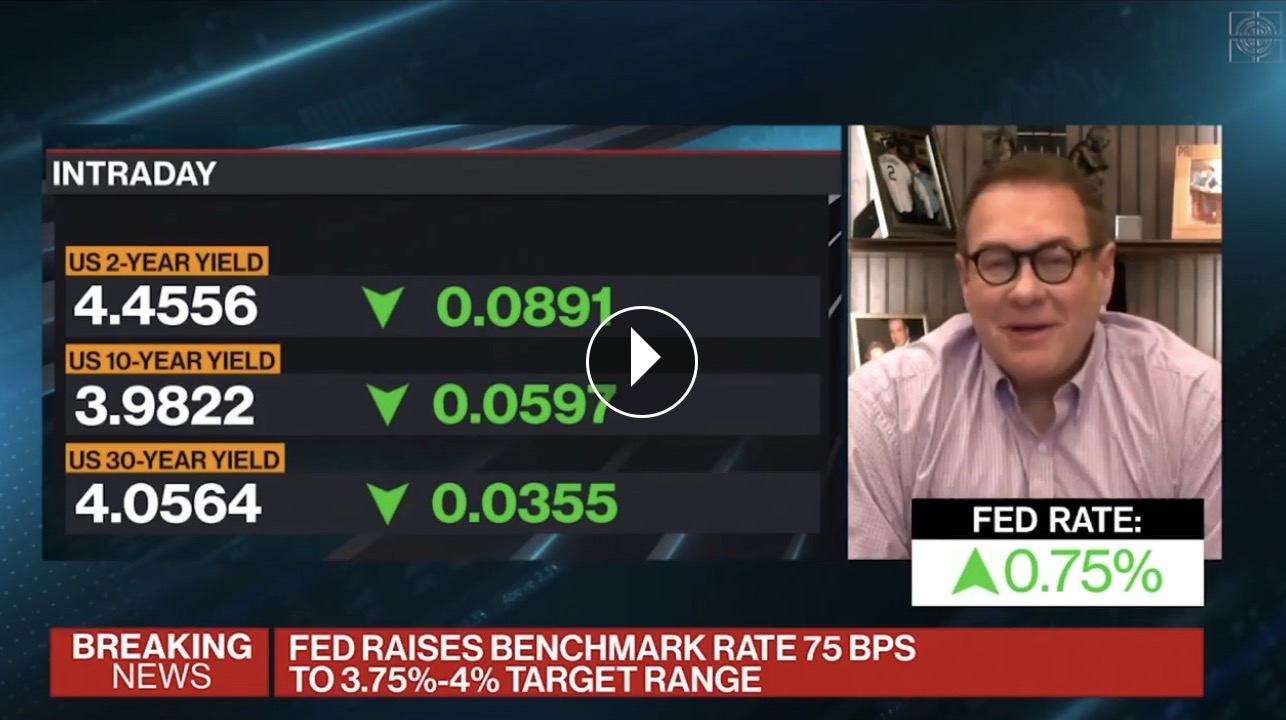

"I Would Not Call This a Pivot Today."

Scott Minerd, Guggenheim Partners Global CIO and Chairman of Guggenheim Investments, joins Bloomberg TV on Fed Day.

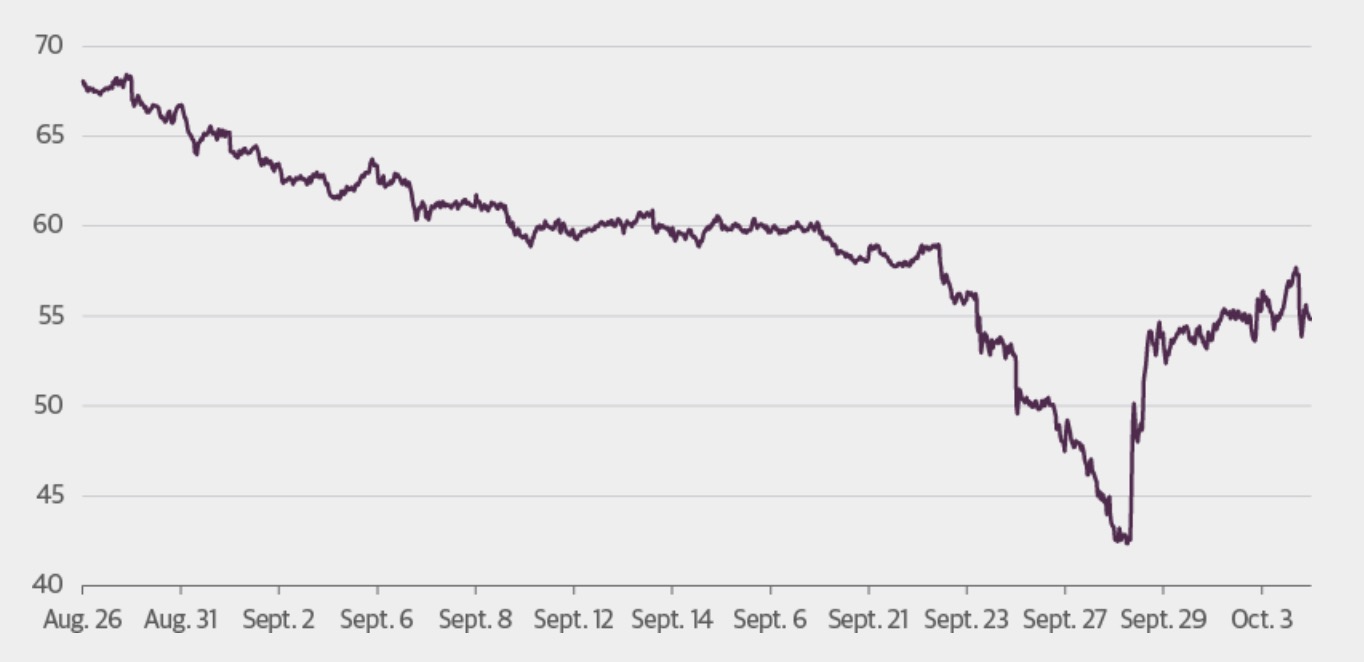

Weaker Payrolls Will Reward Pent-Up Demand for Fed Pivot

Weakening jobs picture will signal that Fed tightening is working as intended.

Macro Markets Podcast Episode 21: Measuring Sustainable Infrastructure

Jim Pass, head of project finance for Guggenheim Investments, and Kate Newman from the World Wildlife Fund talk about the most recent research collaboration between Guggenheim and WWF, a survey of infrastructure investors and developers.

Credit Yields Look Attractive Despite Rising Recession Risks

Signposts for credit investors as the next recession approaches.

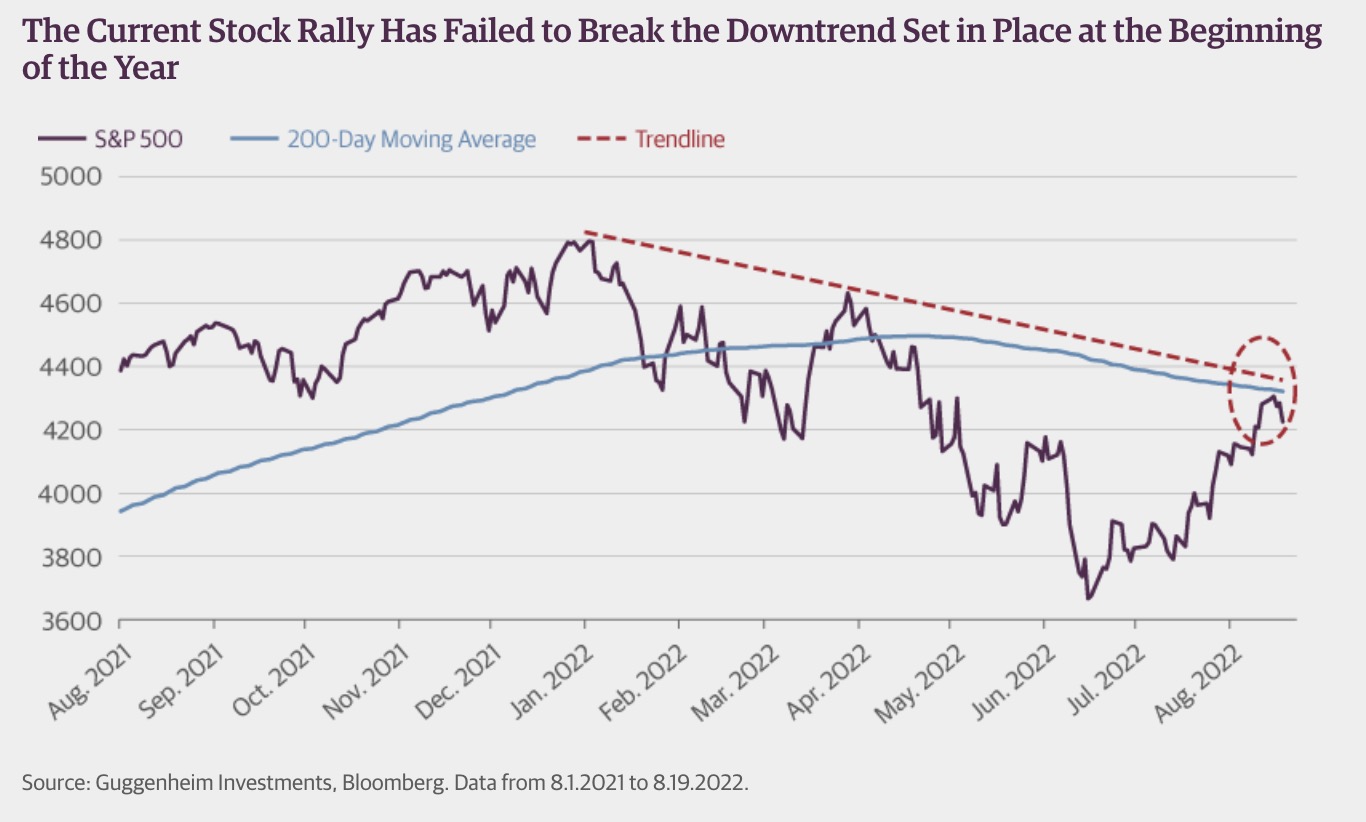

Stocks Are in Trouble if S&P Fails to Break Above its 200-day Moving Average

Deeper losses for equities may lay ahead.

For the Fed, the Devil Is in the Data; Agency MBS Update

U.S. Economist Matt Bush discusses the fast-moving economic data, and Managing Director Aditya Agrawal reports on developments in the Agency MBS sector.

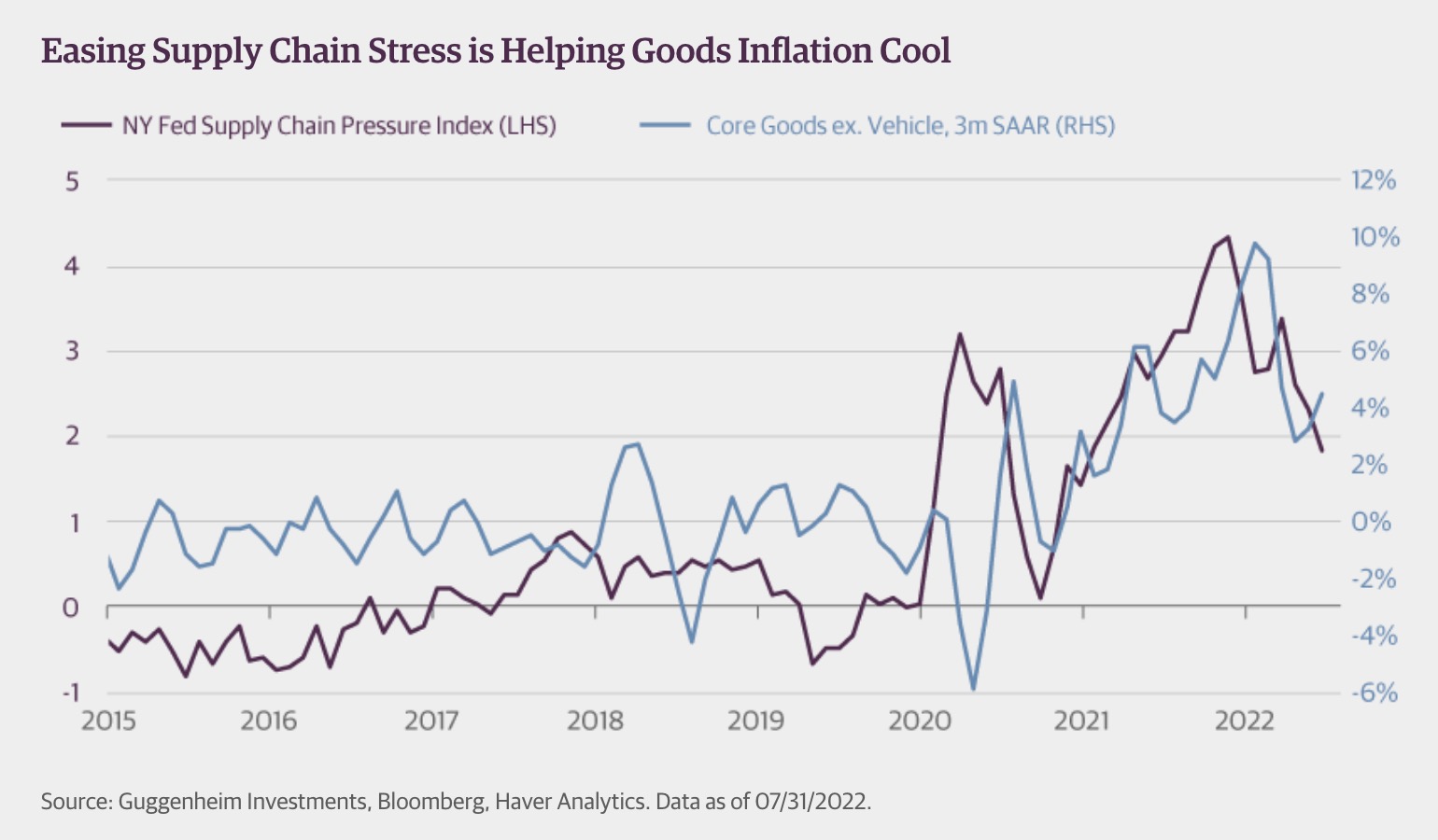

The Inflation Moderation We Expected Should Continue

Lower July CPI inflation is likely the beginning of a trend.

Macro Markets Podcast Episode 18: Investment-Grade Corporates and the Macro Backdrop

Managing Director Justin Takata discusses the technical and fundamental drivers of value in investment grade corporates, and U.S. Economist Matt Bush addresses recession timing and the possible progression of policy.

Recession Signals Flashing Red

The latest data suggest that we may already be in a recession.

Macro Markets Podcast Episode 16: Fed Watch: A Deep Dive into 75

Brian Smedley, Guggenheim’s Chief Economist and Head of Macroeconomic and Investment Research, discusses the impact of the Fed’s 0.75% rate hike on markets and the economy.

Despite the Gray Mood, Skies Are Only Partly Cloudy

The outlook for credit amid rising inflation, monetary tightening, and war in Europe.

“A Season of Pain”

Scott Minerd, Guggenheim Partners Global CIO, joins CNBC to share his views on the consequences of aggressive Federal Reserve tightening.

Fed Aggressiveness Following Delayed Liftoff Sets Up 2023 Collision

The risks of tightening into a downturn.

Inflation, Fed Tightening, and War – Implications for the Economy and Markets

Get insight into the current macroeconomic environment and its implications for the markets in an insightful panel discussion featuring Maria Giraldo, Strategist and Matt Bush, Economist from Guggenheim Investments’ Macroeconomic and Investment Research Team. This informative session will explore how Guggenheim sees the inflation outlook, where Federal Reserve policy is heading, and how investors should be positioned in this environment. Thoughts on the crisis in Ukraine and outlook for a post pandemic environment will also be given.

Looking at Yields in High-Yield Credit

A properly diversified credit portfolio should have exposure to both high-yield corporate bonds and bank loans.

Delta Impact on Consumer Behavior Will Delay Tapering Announcement

The resurgent virus should keep a lid on Treasury Yields.

Latest CPI Validates the Transitory Nature of Inflation Spikes

Falling demand will help limit the extent of more price increases.

A Better Way to Pay for Infrastructure Investments

A revival of the Obama-era Build America Bonds would raise funds with less taxes.

Still No Reason to Panic About Inflation

June’s Consumer Price Index (CPI) again surprised to the upside, adding fuel to headline-writers’ panic about inflation spikes and market speculation that the Federal Reserve (Fed) will need to act soon to rein in prices.

In the Recovery Phase of the Credit Cycle

Strong earnings growth, low default volumes, upward rating migration, and tighter spreads in the recovery phase of the credit cycle.

The Coming Disinflation

Supply chain disruptions may be a near-term challenge, but base effects will slow inflation next year.

Staying on Offense with Fixed Income

Get insight into the current macroeconomic environment and its implications for markets. This informative session will explore why Guggenheim believes the markets’ inflation concerns are overdone, how the Fed’s new framework virtually ensures several years of rates at zero, why investors should own duration and why a strong economy also bodes well for credit. Thoughts on the opening year of the Biden administration and the continuing impact of the COVID-19 pandemic will also be given.

Don’t Mistake Rapid Jobs Gains for a Strong Labor Market

Despite a strong March 2021 jobs report, full employment remains far away.

Don’t Look Now, But Bond Seasonality Is Turning Bullish

The summer months tend to deliver stronger-than-average returns for bonds.

A Successful Green New Deal Will Need Private Partners

A Green New Deal should not be viewed as a big government program, but as an opportunity to reinvent vast swaths of the U.S. economy while pursuing the laudable goal of carbon neutrality

The Fed’s Mixed Messaging on the Yield Curve

Fed Chair Jay Powell is giving conflicting guidance to bond investors.

Staying on Offense: Fixed-Income Outlook

Even as credit spreads have narrowed, further value remains.

A Drunk Man in the Snow: The Random Walk of Interest Rates

Investors’ reach for yield puts downward pressure on 10-year Treasury rates, likely rendering the current yield unsustainable.

High-Yield and Bank Loan Outlook - First Quarter 2021

Our positive 2021 economic outlook, combined with better-than-expected company fundamentals, supports strong credit performance and spreads.

In the Eye of the Storm

The relative calm we feel in the markets right now isn’t the end of the storm, it is just the eye.

The Long Road to Recovery

Scott Minerd, Chairman of Investments and Global CIO, discussed his outlook for markets and the economy with CNBC’s Brian Sullivan during the Milken Institute 2020 Global Conference.

The Impact of the Fed’s Corporate Credit Facilities

As a result of the Federal Reserve’s efforts to shore up credit markets, the leveraged credit sector has delivered stellar performance since the lows in March.

The Fed’s Roadmap

The Fed has increasingly unorthodox policy options if the economy remains mired in a protracted downturn.

Fireside Chat with Scott Minerd and Mike Milken

Scott Minerd, Chairman of Investments and Global CIO, and Mike Milken, Chairman of the Milken Institute, discuss at a Goal 17 Partners web event the government and private-sector response to COVID-19.

We Are All Government-Sponsored Enterprises Now

The support to corporate America during this economic shutdown risks the creation of a new moral obligation for the U.S. government.

Prepare for the Era of Recrimination

The unintended consequences and moral hazard of insufficient and misdirected policies.

The Emerging Emerging-Markets Crisis

Global capital markets are not pricing in the growing likelihood of rising EM corporate defaults.

Note to Clients: Where We Are Nibbling at Value

Allocating capital as the pandemic progresses; emerging markets may be next domino to fall.

The Faustian Bargain

The consequences of policymakers returning to the same tools employed in the financial crisis.

The Impact of ETFs and Index-Tracking and Passive Strategies on the Fixed-Income Market

There are three key areas where the allocation requirements of passive fixed-income vehicles have an impact on the market.

The Great Leverage Unwind

We entered into the current crisis with a whole financial system that had been incentivized by policymakers to take on excessive levels of debt and leverage. The turmoil we are seeing right now is the result of the unwinding of this leverage.

Value Is a Poor Timing Tool

Markets often overshoot, and just because things are cheap doesn’t mean they can’t get cheaper.

Necessary But Not Adequate

Without the right programs, this shortfall in credit availability will increase and it will further deepen the crisis.

Shock and Awe Falls Short

The Fed still has a number of tools at its disposal that haven’t yet been implemented.

Note to Clients: Meeting An Historic Challenge

In this remarkable period in our history, we must renew our resolve to the commitment to always do that which is true and noble for all. Together, we can meet this historic challenge.

The Butterfly Effect

If I had written a commentary on how 4,000 people dying from the flu would topple global financial markets, I think I would have been deemed insane. Yet today that is exactly the story.

Peace for Our Time

The cognitive dissonance in the credit market is stunning. I recently have had the feeling that I’m living peaceably in Britain during the 1930s while on the continent the Germans were building weapons, expanding their army and navy, and opportunistically grabbing land.

10 Macro Themes to Watch in 2020

Ten charts illustrate the macroeconomic trends most likely to shape Fed policy and investment performance in 2020 and beyond.

Global Central Banks Fueling a Ponzi Market

Ultimately, investors will awaken to the rising tide of defaults and downgrades.

The Risk Mitigation Advantage in Active Fixed-Income Management

Why active has the potential to outperform passive in fixed income.

Forecasting the Next Recession: Will Rate Cuts Be Enough?

History shows that once our recession forecast model reaches current levels, aggressive policy can delay recession, but not avoid it.

Forecasting the Next Recession: Will Rate Cuts Be Enough?

History shows that once our recession forecast model reaches current levels, aggressive policy can delay recession, but not avoid it.

Looking Past the Liquidity-Driven Rally

Credit spreads could get tighter in this liquidity-driven rally, but history has shown that the potential for widening from here is much greater.

Guggenheim’s Macro Outlook: Will the Fed’s Pivot Save the Day?

The Macro Outlook webcast featuring Brian Smedley, Head of Macroeconomic and Investment Research, will analyze a wide range of economic and market data that can help advisors navigate through a possible turning point in the business cycle. The following timely questions will be addressed: Will the Fed’s dovish pivot extend the expansion? Can we trust the recessionary signal of an inverted yield curve, or is it distorted by QE? When will the next recession begin, and how severe will it be for the economy and for markets? How should investors position in this environment?

This webinar will cover:

- Analyzing recent economic and market developments in a historical context

- What Guggenheim’s Recession Dashboard says about the timing of the next recession

- What Guggenheim’s proprietary asset allocation models say about how to invest in this environment

- Top themes for investors to watch

The Fed Should Hike Interest Rates, Not Cut Them

The Fed’s cure might make the disease worse without fixing the problem.

High-Yield Credit in a Fed Easing Cycle

High-yield corporate bond spreads and bank loan discount margins typically widen when the Fed is lowering interest rates.

U.S.-China Trade War: The New Long March

During the course of the last two years, we have consistently indicated that the course for the U.S. economy, along with risk assets and rates, was contingent on the impact of any unexpected exogenous events, most likely from overseas.

The Next Step for the Fed Could Be a Hike

Some believe we may have seen the Federal Reserve’s (Fed) last rate hike in this cycle, and that the next step from here will be a cut in rates as the economy loses momentum going into the first half of next year. I believe that view is plainly wrong.

Recession Outlook Summary

Recession fears resurfaced at the end of 2018 as a combination of negative data surprises, communication blunders by the Fed, slowing growth overseas, and rising trade tensions triggered a selloff in risk assets that led many in the market to fear a recession was imminent.

Late-Cycle Drama Is Unfolding

Risk assets will likely enjoy another rally while the Fed stays on hold, but the pause will only allow excesses to become more pronounced.

10 Macro Themes to Watch in 2019

Ten charts illustrate the macroeconomic trends most likely to shape Fed policy and investment performance in 2019 and beyond.

High-Yield and Bank Loan Outlook Report: Up the Escalator, Down the Elevator

An uptick in corporate defaults in 2019 will mark the beginning of a prolonged period of stress in the corporate bond market.

Sometimes Meteors Strike the Earth

What would be a normal seasonal correction is turning into the worst December selloff in equities since the Great Depression.

Fixed-Income Outlook: Jogging to the Exits

Guggenheim Investments’ recently published Fourth Quarter 2018 Fixed-Income Outlook reflects its investment management team’s view that the risk of a sudden widening in spreads next year is rising and could shock fixed-income investors who fail to position defensively now. “The key here is to manage this shift in a timely manner,” said Scott Minerd, Global CIO and Chairman of Investments. “Call it a jog to exit credit and liquidity risk.”

Fixed-Income Outlook: Jogging to the Exits

Preparing for the market turbulence that typically occurs in the run up to a recession.

Forecasting the Next Recession: The Yield Curve Doesn’t Lie

Our Recession Probability Model and Recession Dashboard continue to suggest a recession is likely to begin in early 2020. Investors ignore the yield curve’s signal at their peril.

High-Yield and Bank Loan Outlook

With the Federal Reserve (Fed) now targeting 2.00–2.25 percent on fed funds, tightening monetary policy is putting increasing pressure on corporate borrowers’ balance sheets across the leveraged credit landscape. We estimate that about 30–50 percent of the increase in short-term borrowing costs to date has passed through to the cost of debt for leveraged credit, depending on sector, and we expect this passthrough to increase over the next 12 months as the Fed raises rates.

Fixed-Income Outlook: Tail Risks Are Getting Fatter

While the U.S. economy remains on solid footing, exogenous risks threaten asset values, market confidence, and the strength of the U.S. economy.

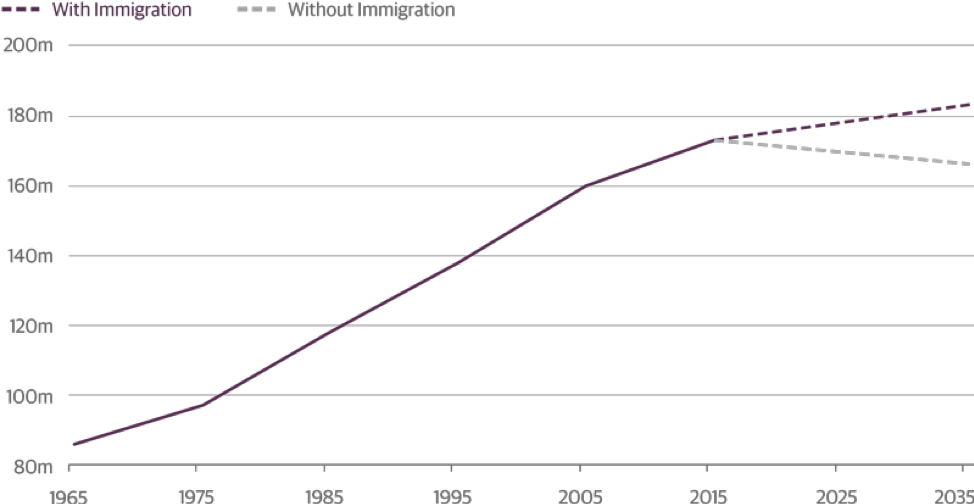

Welcome, Immigrants. The U.S. Really Needs You

To achieve long-term prosperity, rational immigration policy must become a priority.

Late-Cycle Boost and Boom

Investors should stay guarded for exogenous shocks that could pull the next recession forward and cause markets to reprice credit risk.

No One Wins a Trade War

If you want to see who the real victims of tariffs are, go look in the mirror.

Solving the Core Fixed-Income Conundrum

Shortening duration, maintaining an investment-grade portfolio, and generating attractive yields do not have to be competing investment objectives for core fixed-income investors.

Fixed-Income Outlook: Positioned for Choppier Waters

After several quarters of low volatility, tight spreads, and abundant liquidity, financial conditions are shifting.

Forecasting the Next Recession: Updating Our Outlook for Recession Timing

New developments in fiscal policy, the labor market, and the neutral interest rate suggest that the expansion could extend into the latter half of our recession range.

High-Yield and Bank Loan Outlook

As the Federal Reserve (Fed) tightens monetary policy further, we expect to see default rates higher next year. Loan recovery rates averaged 70 percent between 1990 and 2017 as a result of their secured status and seniority in the capital structure. Senior secured bond recovery rates averaged 58 percent over the same period, while senior unsecured bond recovery rates averaged 43 percent. We are concerned about distressed exchanges as the risk of re-default is high. About 7 percent of high-yield corporate bond issuers have defaulted in the past.

Seeking a Return on Sustainable Development

The Western Pennsylvania of my youth was a magical place, with bucolic parklands and architectural gems like Frank Lloyd Wright’s Fallingwater. The decline of the steel industry over subsequent decades has left this beautiful countryside scarred with abandoned mills and rife with the toxins and refuse of a dying industry. This experience informs my perspective when I think about how to tackle the problem of funding the estimated $2.5 trillion gap in annual global infrastructure needs: How can future development avoid the mistakes of the past?

Forecasting the Next Recession

The business cycle is one of the most important drivers of investment performance. As the nearby chart shows, recessions lead to outsized moves across asset markets. It is therefore critical for investors to have a well-informed view on the business cycle so portfolio allocations can be adjusted accordingly.

Bull Market Complacency Calls for Caution—and Action

Investors need to be vigilant, as stocks and bonds are expensive, volatility is low, and risks lay ahead.

The Keys to American Growth

After years of relying on monetary policy to stabilize the U.S. economy, policymakers have redoubled their commitment to stronger pro-growth fiscal policies. As post-election Washington sets its sights on growth-oriented reforms, policymakers should remember that economic growth in any nation is determined by the four basic factors of production—land, labor, capital, and entrepreneurship.

A Contrarian’s View on Inflation Fears

Longer-term bond yields are near their highs for this cycle, while the environment for riskier assets like high-yield bonds, bank loans and stocks remains positive.