Hoisington Investment Management

Quarterly Review and Outlook First Quarter 2026

Oil shocks hitting economies with weak demand and strained balance sheets are especially damaging. Firms cannot fully pass on rising costs, so margins shrink, layoffs increase, and investment falls. Tightening monetary and credit conditions would cause inflation to fade faster but job losses, failures, and fragile household finances to be much worse.

Quarterly Review and Outlook Fourth Quarter 2025

Concerns over accelerating inflation persisted throughout 2025. However, these anxieties were unwarranted as wage and price increases slowed in response to eight influential factors that also suggest that last year’s disinflation will persist in 2026.

Quarterly Review and Outlook Third Quarter 2025

The combined effects of declining capacity utilization in the United States and globally, the inherently deflationary power of artificial intelligence (AI), the Federal Reserve’s deliberate monetary restraint, and the liquidity-draining impact of tariffs will serve to impede economic growth and decrease inflation through 2025 and beyond.

Quarterly Review and Outlook

Five pivotal U.S. economic considerations, including tariffs, monetary policy, fiscal policy, debt overhang, and demographics, are aligning to depress economic growth for the balance of this year and into 2026.

Quarterly Review and Outlook: Fourth Quarter 2024

Factories across the world are growing increasingly idle. Global industrial capacity utilization (CAPU) has fallen significantly, and a rising unemployment rate has followed suit, signaling that the available factors of production globally are progressively more redundant.

Quarterly Review and Outlook Third Quarter 2024

Throughout history one of the most significant features of the global business cycle is the synchronization of individual country economies.

Quarterly Review and Outlook Second Quarter 2024

Amidst a widespread deterioration in the economic landscape, it is crucial to underscore the current detrimental roles of monetary and fiscal policy.

Quarterly Review and Outlook First Quarter 2024

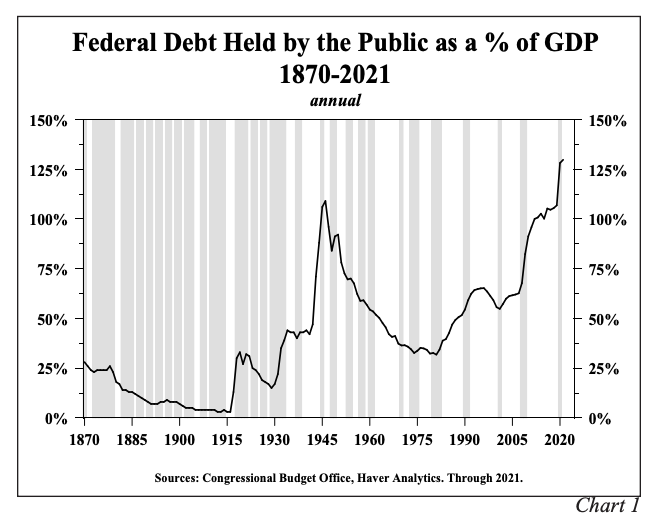

The dynamics of fiscal and monetary policy are now entering a new phase. Due to the emergence of negative Net National Saving (NNS), the law of diminishing returns can no longer fully capture the harmful effect of debt on economic growth.

Quarterly Review and Outlook Fourth Quarter 2023

In 2023, the Federal budget deficit exceeded private and foreign saving, resulting in only the eighth year since 1929 with negative net national saving (to be referred to as NNNS).

Quarterly Review and Outlook Third Quarter 2023

The long history of business cycles illustrates that rising inflation precedes recessions. Inflation accelerations don’t just happen, they are caused.

Quarterly Review and Outlook Second Quarter 2023

Monetary and fiscal indicators continued to tighten significantly in the second quarter pointing towards a material slowdown in the U.S. economy.

Quarterly Review and Outlook Second Quarter 2022

The Fed’s most pressing concerns are to not only reverse its monetary excess and misjudgment of inflation, but also to instill confidence that they will follow important provisions of the Federal Reserve Acts.

Quarterly Review and Outlook

Disaster is a strong but appropriate word that applies perfectly to the state of U.S. monetary policy.

Quarterly Review and Outlook

Real Treasury bond yields fell into deeply negative territory in 2021.

Quarterly Review and Outlook, First Quarter 2018

Nearly nine years into the current economic expansion Federal Reserve policy actions appear to be benign, as even after six increases, the federal funds rate remains less than 2%. Changes in the reserve, monetary and credit aggregates, which have always been the most important Fed levers both theoretically and empirically, indicate however that central bank policy has turned highly restrictive.