Smead Capital Management

The Tsunami of European Bank Mergers

Most global investors are not attuned to what can be seen on the horizon, not far from shore. After the Great Financial Crisis, Europe was slow to address the underlying capital issues. Rather than guillotining the problems, they allowed a slow bleed to take place.

Tech Stock Climax

In my 45 years in the investment business, we’ve observed numerous peaks of excitement. In 1987, a bull market that started at a 1982 bottom below 800 on the Dow Jones Industrial Average (DJIA) peaked at 2,722. It then crashed 43% in 78 days.

Late-Stage Mania: “The Worst Thing Ever”

We are expecting inflation in energy prices and a decline in interest rates when the poop hits the AI mania fan. For these reasons, we are overweight in oil stocks and home builders. These industries prospered in the 1970s, once the stock market mania broke in late 1972!

A “Casino” Stock Market

There is a big difference between betting on something and investing in meritorious companies with long holding periods. Although we are no longer shareholders of Berkshire Hathaway, Warren Buffett shared some wisdom with everyone recently.

The Big Money Always Requires Faith

Shell (SHELL NA) announced last week that they are acquiring ARC Resources (ARX CN). Arc Resources is a gas business in the Montney Region of Canada and is a name that the investors of Smead Capital Management are fairly familiar with.

Building Runways for Planes That May Not Return

During and after World War II, Allied forces established airbases across remote Pacific Islands, bringing with them food, medicine, tools, and machinery that the indigenous people had never encountered before.

Stock Market Sabermetrics

Spring training started in Arizona recently and it reminded us of the 2025 World Series. The series ended a Major League season which was delightful and instructive.

The Kindness of Strangers: Drexel Burnham, Chesapeake Energy and OpenAI

Relying on the kindness of strangers has never been a good business or investment strategy, but it doesn’t mean that people don’t wish that it worked. The main issue with this hope is that it’s foolish to believe that other people’s grace and money will always be there.

Willie Sutton Meets Wayne Gretzky

There are two sides to the current stock market. One side, ignorance avoidance, requires us to know where the money is. The other side, stock selection, is to know where the money is going.

The 1999 and 2025 Rhyme

Mark Twain said, “History never repeats itself, but it rhymes!” Time magazine just came out with its “Person of the Year.”

The Price of Free

For over eighteen years, we have maintained the same investment discipline and the same eight criteria for stock selection. We have deliberately sought opportunity in the sectors and structures the market has decided are too complicated, too cyclical, or simply no longer fashionable.

AI Bubble: Feels Like the First Time

My first experience with a major economic/stock market bubble was the dot-com bubble of 1998-2000. Many investors forget that the Nasdaq and S&P 500 Index bubble that ended March 10, 2000, was the first bubble in a series of three bubbles.

Oil Stocks: Another Pastel Peepers

One of the things we have in common with Warren Buffett is that we started our risk-taking career handicapping at racetracks. Buffett handicapped the horse races in Omaha, and I handicapped greyhound races near Portland at Multnomah Kennel Club in Gresham, Oregon.

The Trump Economy

There has been a lot of controversy around the Trump administration’s policy toward the Federal Reserve recently. What is less obvious to most investors is what they’re aiming to accomplish. Trump continues to talk about getting rates lower, and this has been echoed in other parts of the administration as well.

S&P 500 Index: All Twisted Up in the Game

Is the U.S. economy “all twisted up in the game” with the S&P 500 Index dominated by technology/AI stocks? How much is investor confidence affecting consumer confidence? How much has the increase in financial advice and advisors been fed by the success of this stock market?

The Stock Market’s Berkshire Problem

Investors have talked a lot about the Buffett indicator since the Oracle of Omaha began commenting on it. Buffett compared the market cap of the US stock market to GDP.

Googling Earnings Quality

A wise man once said that generally accepted accounting principles (GAAP) is where you start. It may not be the most economic way of looking at a business for various reasons.

We’re in Good Company

When you have a significant underperformance period, investors have a good reason for wondering if you’ve lost your investing mojo.

Dead Investors Society

We have a truly inspiring corporate leader among the companies in our portfolio. We don’t believe the global equity markets have realized it yet.

Late 2021 Speculation is Back

Our long-time investors are probably wondering why we haven’t made any gains over the last 18 months.

Thank You Warren Buffett

In light of the announcement that Warren Buffett is stepping down, we thought it very useful to share some of the keynote talk I did at the University of Nebraska-Omaha Business School last Friday night (thanks to its wonderful director, Robert Miles).

Cutting Off Your Nose to Spite Your Face

In the Middle Ages, a common form of punishment was some form of mutilation, which included cutting off the nose of a prisoner or purposefully marring one’s own appearance before the arrival of conquering armies

Thursday’s Post-Mortem

We’d like to discuss our three worst-performing securities in the US portfolio to help our investors understand why we are sitting on our hands and allowing our discipline to proceed.

O-I-L-S, Oil Stocks

When you grow up with a father who worked in the brokerage business, you hear a lot of stories.

Been Here Before

Investors who have come to us in the last three to four years are probably wondering if we’ve been here before. By here, we mean a stretch of significant underperformance relative to our benchmarks. The answer is, yes. Let’s review those prior circumstances to see if we can learn something about where we might be headed.

Noah’s Stock Market

We believe that we must build a common stock portfolio which will float when the multiyear bear market creates a waterfall of selling among magnificent growth stocks and passive S&P 500 Index owners.

Index Mania: On Top of the World

Karen Carpenter was one the greatest singers of my lifetime. One of her biggest hits was called, “Top of the World.” The key line of the song says, “I’m on top of the world looking down on creation and the only explanation I can find, is the love that I’ve found ever since you’ve been around, you most put me at the top of the world!”

Bursting the Complacency Bubble

As we welcome a new year and its many possibilities, it’s important to reflect on where the markets and investor psychology sit on the pendulum of greed and despair.

Don’t Trust Antitrust

The Federal Trade Commission (FTC) recently blocked the merger of Albertson’s and Kroger, which are the two largest stand-alone grocery chains.

Déjà Vu All Over Again

For us as investors, we can say that this is déjà vu all over again as we practice our stock picking discipline.

Presidential Stock Market Euphoria

How does the euphoria for stocks in the days after the 1980 election contrast with today’s Trump election euphoria?

The Pictures Say It All

Dow Jones (publisher of The Wall Street Journal) announced that Nvidia (NVDA) will replace Intel (INTC) in the Dow Jones Industrial Average. Intel was brought in to replace Union Carbide four months and nine days before the peak in Intel’s stock price. Union Carbide became Dow Chemical via merger.

Inflation Mathematics

Two major labor unions, the Dock Workers Union and the Boeing Machinists Union, have attempted to reach an agreement with their employers on a contract. The dock workers agreement proposes an average 8.5% per year wage increase over six years, and the Boeing Machinists Union’s proposal is for an average 7.5% wage increase over four years.

When Buffett Meets Bannister

Barry Bannister, Managing Director and Chief Equity Strategist at Stifel, put out an excellent research piece on future returns based on what industry folks call the “equity risk premium.”

When Smart Money is Wrong

We learned a long time ago that we wanted to know what smart professional investors were doing. It’s always better to know who is smart rather than being smart yourself. Therefore, we’ve constantly kept track of insider buying, what great investors like Warren Buffett and Carlos Slim were doing, and what the most successful hedge funds were up to. A recent chart stopped us in our tracks.

Same as it Ever Was

We’ve always admired the great artistry of David Byrne from the Band Talking Heads. My favorite song of theirs is “Once in a Lifetime.” We think this song can tell our readers a great deal about how to look at our portfolio as we navigate an expensive and maniacal S&P 500 Index environment.

Markets Adapt to Your Style

My colleague Will Keenan recommended an outstanding book, The Professor, the Banker, and the Suicide King, by Michael Craig. The book is a short and entertaining read of how Andy Beal played the best poker players in the world heads-up. He not only gambled toe-to-toe, but he also reminded them that they were doing what everyone should think poker is: gambling.

Crowd Strike

One of the very popular technology companies in recent years has been CrowdStrike, Inc. It provides cybersecurity to numerous major technology companies including the top Artificial Intelligence (AI) players.

The Death of Stock Picking

In a recent The Wall Street Journal article, Jason Zweig correctly pointed out that 85% of active stock-picking funds and ETFs had underperformed their benchmark.

Cantillon Marries the Red Queen

Over the last four years, we have maintained that the U.S. middle-class consumer is on firmer ground than many believe. The first wave of inflation that seems to be receding is just that—the first wave of a set—and oil and gas companies are fundamentally well-positioned for the next decade.

Two Plus Two Still Equals Four

We are contrarians and oddly crave the moments when history, psychology and mathematics get defied in the U.S. stock market. We believe this is one of those points in time.

The Genesis of Our Stock Selection

We have gained a number of new investors and get regular vetting interest from investors who need to understand the roots of our stock-picking discipline.

Only Dave Cuts the Federal Budget

Back in 1993, a brilliant satirist by the name of Ivan Reitman produced a movie called Dave. It was the story of a life-threatening stroke besetting the President of the United States of America.

Buffett and Munger Mark the End of An Era

At the Berkshire Hathaway Annual Meeting we marked what we believe is the end of an era both for Berkshire and for the S&P 500 Index.

1968-1969: Buffett and Price Agreed

The most interesting thing about 1968-1969 was the agreement about the stock market future between the greatest growth investor at that time, T. Rowe Price, and the greatest value investor of all time, Warren Buffett.

DXYZ: An Old Form of Ignorance

Many investors are bullish, or not fearful, of the future of stock returns. At Smead Capital Management, we continue to explain to our investors how poor the outcomes will be. Some ask when this view will change.

Hit Them Where They Ain’t

As a child, baseball became the core of my life. Collecting baseball cards, watching games on TV, and playing in Little League and neighborhood games absorbed my time outside of grade school. Out of this came a desire to know baseball history and become a statistics junkie.

Saved by Zero

The U.S. Federal Government has set a net zero carbon goal by 2050. Tremendous resources have been applied with borrowed money to fund these goals and subsidize money-losing green investments.

Looking for the Outsiders

William Thorndike’s book The Outsiders has been considered a classic for some time now. His story teaches readers about the business performance of Henry Singleton, Katherine Graham, John Malone and Daniel Burke.

Lonely Contrarian Divergence

In previous missives, we have gone into considerable detail regarding the historic ascent of index concentration, coupled with the heightened prevalence of passive investing.

A Ticket to Purgatory

The Sherman Antitrust Act was created to stop our democratic republic from being ruined by “the concentration of capital in vast combinations.” The fear was that if too much of the success of industry went to too few people, our system would get disrupted.

Drivers and Stock Pickers

In studies, 90% of drivers think they are above average. We believe that 100% of the people who pick stocks for a living think they will be above average.

Chronological Snobbery

C.S. Lewis coined the term ‘chronological snobbery’. According to Lewis, the definition of chronological snobbery is “the uncritical acceptance of the intellectual climate of our own age and the assumption that whatever has gone out of date is on that count discredited.”

Stock Market-Interest Rate Rhymes

Warren Buffett regularly reminds his shareholders that interest rates are a gravitational pull to stock prices. History shows that the movement of stock prices and interest rates don’t necessarily happen simultaneously but play out over time.

70/20/10 Rule Redux

A friend of our stock picking discipline reminded us of a very important force in the stock market. It was called the 70/20/10 rule, and it was promoted by Roger Edelman, Richard Evans and Gregory Kadlec in an early 2013 Financial Analysts Journal article.

Stepping on a Rake

The year 2008 and the subsequent Global Financial Crisis (GFC) stand as a watershed moment in the annals of our capitalist society. It was a bailout prompted by poor capital allocation, deficient risk management, and unchecked greed.

Tech Stock Hail Mary

The most famous “Hail Mary” in American football history happened in 1984. On the very last play of the Boston College football game, an undersized quarterback named Doug Flutie threw a bomb into the end zone to teammate Gerald Whelan. Boston College had won the game!

Good Odds and Odd Goods

The paradox that this marriage potential created at the college was that the odds are good, but the goods are odd. This is the statement that can be made for common stock investing today.

No Dating Game for Buffett

Watching Warren Buffett and Charlie Munger Saturday in Omaha caused us to think about a very popular 1960s TV show called, “The Dating Game.” Hosted by Jim Lange, the game was played with the host on one side of a wall with a male or female contestant.

The Game Has Changed

In the early 2020s, the stock market looked much like basketball used to: a big man’s game. As examples, money management firms like Vanguard and Blackrock lumbered to higher heights of assets while the passive firms swallowed more market share.

Buying Unwanted Assets

To kick off the beginning of 2023, there continues to be a bias we see in equity investor portfolios. These portfolios have many of the traits investors see at the endpoints of the economy like software, consumer products and computer chips.

Cutting Your Way to Prosperity

What must happen to make these stocks attractive to investors like us?

Tech is Bullish on Oil

The news of the shocking OPEC+ announcement of a supply cut is saturating the minds of investors and market prognosticators.

Funding Unprofitable Growth

We have been reminding everyone that we believe we are unwinding a financial euphoria episode that Charlie Munger called the biggest of his career, “because of the totality of it.”

The 2022-2023 Regime Change

The events that began with Thursday’s tumult in financial stocks and precipitated the FDIC takeover of Silicon Valley Bank and Signature Bank were swift.

Musings from Buffett’s Letter

There were many good things to think about from Warren Buffett’s letter to shareholders which came out recently. In this piece, we’d like to drill down on two subjects that Buffett highlighted.

Drilling for Oil on the NYSE

As a young stockbroker in the 1980s, I was very enamored with T. Boone Pickens.

Ramblings From My Idol, Charlie Munger

On February 5, 2023, Charlie Munger sat down as the Chairman Emeritus of the Daily Journal Corporation (DJCO) to answer questions from shareholders and the public.

A Sharpe Rebuke

We are closing in on what we think may be the question of the decade. If a majority of stock market capitalization in the US is passive or indexed, does this cause problems for stock markets?

Recession Fear Investing

A recession is two consecutive quarters of economic contraction.

Unreliable Contrarianism

It appears to us at Smead Capital Management that investors are behaving in a way that will damage their capital and cause them to suffer stock market failure.

Companies Still SOIL-ing Themselves

I was reminded in a recent read of Robert Hagstrom’s book, Warren Buffett: Inside the Ultimate Money Mind, how Warren Buffett and Charlie Munger define the economic earnings power of a business.

Home Builders’ Sentiment

The Wall Street Journal reported last week that the National Association of Home Builders’ (NAHB) sentiment about the future was 33% and at its lowest since 2012.

The Good News: Einhorn is Finkle

In the 1994 comedy film, Ace Ventura: Pet Detective, Lt. Einhorn is the female leading the Miami police’s investigation of the disappearance of the Miami Dolphin’s mascot, Snowflake.

Humpty-Dumpty Stock Market

The era of the dynamic sales growth tech company, with a religious quality to its leadership, appears to be over.

Dial P911 for Value in Porsche and VW

If you were walking down the street and saw a $100 bill just sitting near the curb, would you pick it up?

Newton’s Law of Stock Market Motion

Newton's First Law of Motion states that an object in motion tends to stay in motion unless an external force acts upon it.

Humming All the Way to Reno

The investors in the Smead International Value Fund have asked our team at Smead Capital Management what looks attractive today.

At This Moment

We are at the point in this nasty bear market where those who are buying the glamour tech stocks of the last ten years (on the way down) are at a crucible.

First World Problems

The investors of Smead Capital Management have been hearing us talk about ‘First World Problems’ recently.

The Strategic Squeeze

Thanks to reading Spencer Jakab’s book, The Revolution That Wasn't, we've been thinking about what it is like to be in a short position when overwhelming demand affects prices.

Do As I Say

The current stock market circumstances have created an incredible contrast between what investors say they think about the stock market versus what they are doing with their capital.

Suffering Slings and Arrows

We believe one of the hardest things to do in common stock investing is to hold winners for a long time. This is especially true with what are normally cyclical industries.

Two-Headed Investment Monster

As we’ve hit the halftime mark for the investment year 2022, we are faced with a daunting two-headed monster.

Love is in the Air

Chairman and largest shareholder, Harold Hamm, is trying to own our shares of Continental Resources (CLR US) at a price of $70.

Buffett, Jones and Hamm: An Oil Wisdom Trifecta

Someone once said, “Better than being smart is knowing who is!”

Don’t Cry for the Most Wealthy

Over the last four years, we have argued that the glamour monopoly technology companies have a low multiplier effect in the U.S. economy

When Quality Fails

Academics argue that there are three proven factors of investing: Value, quality and momentum.

Buffett’s Buying Oil Stocks

After listening to the Berkshire Hathaway Annual Meeting on April 30, 2022, we thought it would be appropriate to frame the aggressive buying of Occidental Petroleum (OXY) and Chevron (CVX) in the first quarter of this year.

Generals Marching Without Soldiers

In 1980, when I came into the investment business, investors were very conscious of trading ranges that had existed the prior 16 years.

The Race for Space

Moving forward beyond the pandemic of 2020, the theme the world woke up to is that people want more…more home, more land, more entertainment, more goods.

Energy Desperados

As a firm, we refrain from delving into politics and political debates.

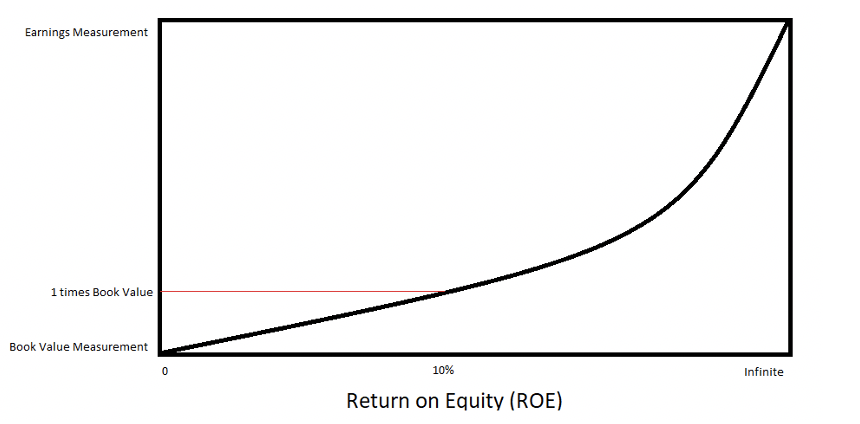

Buffett’s ROE Game: Coke in ’88 and OXY in ‘22

The news of Berkshire Hathaway’s purchases in Occidental Petroleum (OXY) has been seismic in our minds, but to most investors it has been but a whimper

Stock Market TAMnation

Totally Addressable Markets (TAM) are at the heart of what Charlie Munger calls the biggest euphoria episode he has ever seen in his career. We believe that the coming stock market failure emanating from the over-pricing of the U.S. stock market is closely tied to TAM.

Buffett’s Latest Inevitable

Warren Buffett released his 2021 Berkshire Hathaway Annual Letter on Saturday, February 26, 2022. He seemed to want to talk about almost anything besides the stock market.

Tombstone of High Returns is High Volatility

A couple of weeks ago, we gave a presentation at the first annual Smead Investor Conference near our headquarters in Phoenix.

Alpha Creation: Long Duration

We operate under the premise that alpha can be generated by stock selection, courage, concentration, and long-duration holding periods.

Failed Experiments

We were watching CNBC recently and an analyst mentioned what practically nobody besides us has said.

Housing Goes from Graham to Munger

Ben Graham is ascribed as being the father of value investing.

Occidental Petroleum’s Wirth

On April 12, 2019, Chevron (CVX) and its CEO, Mike Wirth, offered $33 billion dollars to buy the common shares of Anadarko Petroleum.

Outlook 2022: Polar Opposites

There are three pillars of investing for us at Smead Capital Management.

True Religion in Value

Most professionals who employ our strategy are wide-asset allocators

Lessons From the King of Capital

We have been reading a book written by David Carey and John Morris called King of Capital. It is the story of the Blackstone company and its key founder, Stephen Schwarzman. An economic history from the 1980s through today is included and lays out some excellent reminders of certain disciplines which can create wealth in picking public companies to invest in.

No Doubt Investors

In the depths of the lockdowns in March and April, we were together at home, day after day. The U.S. Federal Reserve Board pumped large amounts of liquidity in our economic system. The U.S. Federal Government followed by providing large amounts of fiscal stimulus in PPP loans...

Pulling The Punch Bowl

Overall common stock index performance can be a very confusing thing to most investors. From a cyclical standpoint, the history of stock price performance in the U.S. is closely associated with the Federal Reserve Board. When the Federal Reserve Board reverses an accommodative interest rate policy, it is affectionately referred to as “pulling the punch bowl.”

Aesop’s Marathon

Warren Buffett and Charlie Munger always refer to Aesop as the originator of investment logic. His first dictum was “a bird in the hand is worth two in the bush.” His second dictum was the fable of the “Tortoise and the Hare.”

Energy Bandwagon and Bankers

In 2014, famed UK stock picker Terry Smith wrote a piece, titled Shale: Miracle, Revolution or Bandwagon?, in most ways mocking investors excitement in the oil and gas business in the United States of America.

Bond Market Education

During our quarterly webcast last week (October 21, 2021), someone asked us a great question. They asked, “Does the ten-year Treasury bond rate at 1.65% and an inflation rate of 5% teach us that inflation will be transitory?” It is an important question because the majority of economists and market strategists are betting that inflation is transitory.

The Gestalt of the 2020’s

Today’s atmosphere is one that we rarely see as investors. This is not like junk bonds in the 1980’s or the run up in Valeant Pharmaceuticals and the other generic drug companies in the 2010’s. There is not a narrow way of looking at today. It is broad.

Zuckerberg’s Choice

We have entered the phase when the body politic and public opinion are aware that Facebook is disturbing our society. This is very important to us as investors, because the big tech companies make up a disproportionately large part of the S&P 500 Index.

Inflation is a Wolverine

The media and the economics profession are treating inflation like it is a friendly puppy dog. They think you can take it out of its pen and play with it for a while. The popular theory is that you bring it out in a severe dip in economic activity and when the economy gets back on its feet, you kindly ask inflation to crawl back into its pen like any good puppy dog would do.

Incentives Pivot from Greed to Fear

The talk of inflation today looks much like housing did in 2007. Evidence is mounting everywhere that this is a real long-term problem that is only getting worse. You can read this in the media, but yet security prices don’t reflect how damaging this may be.

How Bizarre

Let us share some of the “bizarre red-blue lights flashing” in the S&P 500 Index.

The McNealy Problem

Investors often ask our team at Smead Capital Management what we spend our time on. We believe reading is the best use of our time to learn and think about the way that we can profitably apply capital for our investors.

Berkshire: Pinch Hit Weschler

We have argued for years that the biggest mistake being made by Berkshire Hathaway was not giving shareholders access to the thoughts and investment discipline of their two talented stock pickers, Ted Weschler and Todd Combs. After all, Buffett calls the shareholders “partners” and has not allowed his partners to understand anything about the strategies and results of upwards of $30 billion of shareholder capital.

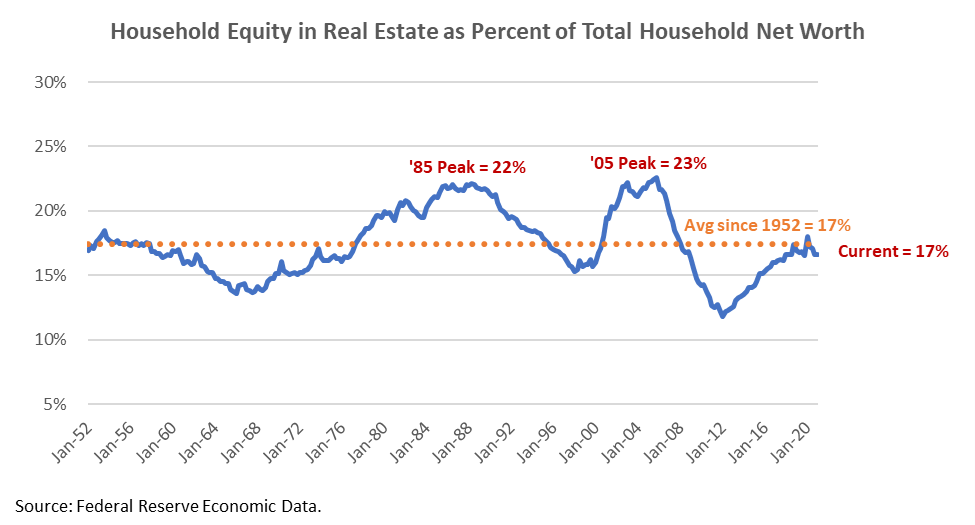

Housing: Driver of Average Wealth

We have been in many discussions with our investors, people in the media and the investment management industry on where housing is today.

COVID-19: Summer 2020 versus Summer 2021

In the summer of 2020, we didn’t know quite a few things about how Americans would react when they got their social and entertainment choices back.

Quail Pricing in Oil Assets

On the insistence from a friend and a colleague, I watched the movie There Will Be Blood over the weekend.

Tech: Always and Forever

We’ve been thinking about John Locke’s “Law of Fashion” in the context of the U.S. common stock market.

The Law of Fashion

The great philosopher, John Locke, brilliantly captured the way the world works.

Value Investors are Still Rolling Stones July 6, 2021

Most millennials have never seen an era where value has done well.

Good Medicine at Bargain Prices

We have been long-term owners of Amgen (AMGN), Merck (MRK) and Pfizer (PFE) among the major pharma/biotech companies

Taking Lumps for Alpha

Now that investors are reconsidering active stock picking and are especially interested in value stock strategies, let’s analyze where excess stock market returns come from.

Engulf and Devour

As Amazon prepares to buy MGM Studios and announced an effort to put pharmaceutical stores all over the U.S., we are reminded of one of my favorite comedy movies, Silent Movie

Today’s Stock Market Illusions

My recent reads have been stuck in the 1960’s, including Adam Smith’s The Money Game and Andrew Knowton’s Shaking the Money Tree.

Repeating Discovery’s History

“History doesn't repeat itself, but it often rhymes.” – Mark Twain

Inflation: It’s Just the Start

To say that we were surprised by some of the discussion at the Berkshire Hathaway Annual Meeting would be an understatement. The conversation Warren Buffett and Charlie Munger leaned into on inflation was possibly the most interesting. Warren and Charlie gave large credit to Larry Summers for his willingness to stand alone on the effects of today’s fiscal and monetary policy on prices. We thought this was an ideal time review Buffett and Munger’s discussion and see what conclusions we could draw.

Buffett: No Fish in the Barrel

The Berkshire Hathaway Annual Meeting was a mixture of caution, wisdom and honesty.

Star Trek Stock Market

Now that the leaders of the most popular tech companies are going into outer space, we thought it appropriate to consider the return implications of this urge to “explore strange new worlds.”

Ground Control to Major Tom

As we have been holding calls with prospective and current investors of our firm, we have been arguing that the stock market is underwhelming the success of the economy.

Winning the Peace

Even before the war is over, the winning side needs to consider how to “win the peace” which will follow.

Dumb and Dumber III

Dumb and Dumber was a 1994 movie which tells the story of Lloyd Christmas (Jim Carrey) and Harry Dunne (Jeff Daniels)

Animal Spirits at Cocktail Parties

My generation, millennials (those born from 1980 to 2000), have been noted for much of the last 10 years to be a risk averse group.

Hopelessly Devoted to Technology Stocks

Today’s stock market looks like the love affair between Danny and Sandy at Rydell High. Sandy is “hopelessly devoted” to Danny, even though he is the leader of a Los Angeles high school gang.

Buffett’s Annual Letter: Sins of Omission!

Warren Buffett’s annual letter was great in all the easy ways and disappointing in the ways that matter the most to his shareholder partners

Beating Bobby Fischer

We think this is an excellent time to ponder the thoughts of Buffett and Munger.

Simon Says

The object of the game was to get to the finish line first and then become the leader the next round. The stock market has its own game of “Simon says” and that is in the mall property world.

Vexing Today’s Convex Pricing Behavior

Fortunately, human behavior has a history of repeating itself at extremes. The worst buying decisions are made at the top. Just like bonds, the convexity is true when yields rise going forward. It’s a slippery slope and could be vexing.

Tesla and GameStop: Pass the Dutchie?

We have enjoyed watching what happens in the late stage of a financial euphoria episode play out in the escapades of millennial investors on Reddit, who seem to “rule the nation.” While politicians, regulators, the media and others try to sort this out, we thought some historical perspective might be helpful.

The January Effect

There have been a small number of consistent alpha-creating axioms in the U.S. stock market over time. Value beat growth over long time frames, tech stocks hit bottom in the summer and crowded trades separate you from your money, to name a few.

Outlook 2021: “Frenzy” is the Opposite of Bull Market Stew

Our outlook for 2021 is formed by the need to get away from the crowd and to expect some very stormy weather in the U.S. stock market. We are not afraid of drowning. Therefore, we will review the circumstances at the bottom of the market in 2009 with today’s market to see where the crowd is and where we need to go to avoid the coming storm.

Throwing Caution

As we begin 2021, the investing public is tied up in a “frenzy,” to quote Charlie Munger from a recent interview. This “frenzy” can be captured a couple ways.

From the Impatient to the Patient

As we enter 2021, it appears that Buffett had things upside down in 2020. The things which had gone up the most by the end of 2019, went up the most in 2020.

Famed Climatologist Charlie Munger

We were fortunate to watch a recent interview Charlie Munger did with Cal Tech as a distinguished alum. We consider him to be one of the most successful contrarian investment thinkers on the planet. At 96 years of age, he has no fear of being politically incorrect. We contrast this with the mountain of writing, media and rhetoric associated with the topic of climate change.

Net Present Value Bargains

There appears to be a few huge statistical bargains available in the stock market based on the simplified version of Benjamin Graham’s intrinsic value calculation.

Reminiscences of an eBay Operator

My wife brought me a box of ornaments that my mother has given to us over the years. I decided to check what I could sell them for on eBay (EBAY). What a great way to look at what is going on in equity capital markets!

People Need People

In all this tech euphoria and COVID-19 quarantining, investors are missing a key fact. People need people.

One Helluva Party

As Buffett said, this looks like “one helluva party” with the individual investors, professional investors and insiders all joining in the fun. As a former fraternity member in college, the best parties were always when you couldn’t find anyone missing. It wreaks of that today in the stock market.

WFH is a WKF

We came up with a theory many years ago to address how important psychology is to owning common stocks. We found that the risks go up in a stock market, or in an individual stock, when a “well-known fact” (WKF) was acted on in the extreme.

Cherry Picking is Tempting

When you run an equity portfolio which is concentrated in 25-30 common stock selections, there are usually three stocks which stick out as particularly attractive at any given time.

Humility Produces Alpha

Our experience tells us that we have hope from the indignity and humiliation of the present circumstances.

Energy in Dreman’s Icahn-ic Green Wing

David Dreman’s book, Contrarian Investment Strategies, was gospel to investors when it was first published in 1979. Investors had been decimated by markets going nowhere over the prior 10 years. Stock investors were ready for something new. Dreman had produced a lot of success as an investor and wanted to share his gospel of contrarian value investing.

Breaking Big Tech

We recently read Peter Doran’s book, Breaking Rockefeller, which is a fabulous economic history of the world from 1840-1920 and focuses on how the monopoly created by John D. Rockefeller was broken from 1890-1910. We also watched a documentary called, “The Social Dilemma,” which explains, through the eyes of some of the social media creators, how incredibly damaging the monopolies, created by internet technology, are to society.

Antitrust: The Truth Will Set You Free

Anyone who owns U.S. large cap stocks must understand what can happen from the actions of the government to enforce the laws on the books for antitrust. Contrary to popular opinion, these laws are not set up to primarily protect consumers from being gouged on price by someone with a monopoly.

Smead’s Folly Becomes Newsom’s Folly

We became extremely bearish on energy in 2011. At the time, we saw interest in Seattle for hybrid and electric cars. This convinced us that 10% of the cars on the road nationwide might be hybrid and electric by 2020.

Quality is Missing the Point

I got very excited when I came across an excerpt from Jordan Ellenberg’s book, How Not to Be Wrong. His book was written to teach readers how much logic and common sense is provided by math. He tells the story of Abraham Wald during World War II, who worked for the Statistical Research Group (SRG).

Company-Specific Macroeconomic Multipliers

An interesting contrast was drawn on September 15, 2020 between Lennar’s (LEN) earnings call and statistics on revenue per employee at Apple Corporation (AAPL). Lennar described strong growth out into the future in a measured way, because they believe that the prior decade created a home supply deficit due to underbuilding.

There Is No Alternative (TINA)

We hear numerous market strategists talk about stocks which are going up because “there is no alternative” to owning them. In the Wall Street vernacular, this goes by the phrase TINA.

Value’s Lifeblood is Performance Chasers

While listening to Rob Arnott on a recent Morningstar podcast, I became enamored with something that Arnott was emphatic about. He pointed out that the structural advantage of being a contrarian isn’t being smarter. Every winning purchase in the stock market comes as an opportunity cost to the seller.

The Inflation Cocktail is Being Mixed

Since the inflation cocktail is closely related to value stock outperformance, we are very excited about our future value investing possibilities.

Value in the Four-Minute Mile

Due to the pandemic, there is a sense of permanence on Wall Street to what has transpired. This permanence focuses on the changes that we have seen in the recent five months in our daily lives. These changes include shopping online versus shopping in-person, getting takeout versus sitting in a restaurant and working from home instead of talking sports around the water cooler with our colleagues.

Economic Normality: When? Sooner? Never?

In the time since COVID-19 hit the economy and stock market, there has been three phases. First, the question was ‘when’ will the economy return to pre-COVID normal? Next came ‘sooner or later’? Recently, we have moved to ‘will the economy ever come back’? For long-duration investors like us, what are the investment implications in where we are now in a U.S. stock market with many securities priced for ‘never’?

True Stories of Financial Euphoria Circa 1998-1999

When you are in a financial euphoria episode, like the one we are in currently, it is hard to visualize the impact it has when it breaks. Historically, it is the leading cause of stock market failure. We thought it would be helpful to discuss the secondary impact of the euphoria on common stocks.

The Fear of Stock Market Failure

The stock market is a big place with thousands of investments that you can make as an investor. It’s a frustrating place. There is a myriad of investing disciplines that you can seek out. As a millennial, my generation is learning this for the first time. Don’t kid yourself for one second: they will destroy wealth.

To Hell and Back

Everyone who owned common stocks in the U.S. went through hell in the first quarter of this year. The 36% decline in the S&P 500 Index in February and March was the fastest 36% decline of my lifetime. This hell was especially damaging to those of us who have a positive view of the U.S. economy over the next ten years.

The Boy Who Cried Wolf

The nice thing about being the boy who cried wolf is that you look stupid before you are proven correct and you look smart when you are right, but nobody believes you until it is too late.

Sins of Omission

With markets extremely difficult and volatile as we work through COVID-19, we thought it would be good to review important parts of our investment discipline. One way to do that is to consider stocks we found via our eight criteria for stock selection and did not keep long enough to get to their ultimate rewards.

Amazon vs. eBay: A Case Study in Business Models

On June 4, 2020, eBay (EBAY) released a business update to make investors aware that the quarantine circumstances have caused their business to perform “significantly better than expectations,” compared to their earnings report on April 29, 2020.

1972 + 1974 = 2020

The oddity of today’s stock market is exactly what any God-fearing value manager should pray for. There are very few scenarios in the last 50 years that can be used to model or forecast what is currently going on.

American Pie

A series of charts and historical evidence exists in late May of 2020 which shows that the S&P 500 Index and the vast majority of institutional investors of all shapes and forms have concentrated their investments in the most popular stocks in the stock market.

Only the Lonely Can Play

Great investment opportunities are lonely. History shows us the crowd behaviors to avoid and the investment market circumstances to capitalize on. We believe we are at one of the great junctures, where the crowd thinks they unequivocally know the future.

Gruesome Stocks

We are big fans of Buffett’s theories about businesses with low capital requirements and the ability to throw off cash to owners. Unfortunately, he recently emphasized indexing and didn’t shy folks away from today’s glamour tech stocks which require more and more capital

Searching for Peter Lynch

Late last year, there were three people that we observed as optimistic about the prospects of the oil business. These people were Warren Buffett, Sam Zell and Peter Lynch. In revisiting their comments before and after the shutdown of the economy, we can see that two of the three have significantly altered their opinion.

Berkshire Hathaway Annual Meeting 2020: Buffett Contradicts Himself

Warren Buffett has been arguably the best asset allocator and value stock picker of the last 60 years. We are normally thrilled to sit in his classroom. Quite frankly, we were baffled by the Berkshire Hathaway Annual Meeting held on Saturday in Omaha.

The Façade of Financialized Demand

The capital markets are a highly complex system, where perturbations can cause a tidal change. Every business around the world has been affected by Covid-19. For a profitable business anywhere, this is a calamity. For a business that was losing money before this, it’s a tombstone.

Munger’s Phone is Not Ringing

You have to love The Wall Street Journal writer, Jason Zweig. His extremely inciteful “Intelligent Investor” column could be called “Jason’s Wet Blanket,” because he seems to throw a wet blanket on most investment disciplines in U.S. stocks. This week’s wet blanket is designed to create even more desperation for value investors via his interview with Charlie Munger.

The Willingness to Look Foolish

This smashing of economic hopes, right before one of our brightest demographic phases, could be a bonanza which only those of us who are willing to look foolish can acquire.

The Blutarsky Moment

The year after I graduated from college, the movie Animal House debuted in 1981. With everything falling apart for the Delta fraternity, including grades and double-triple probation, all looked lost. At the point when others would give up, senior fraternity member, John Blutarsky, gave a spirited call to arms by reminding everyone that the U.S. didn’t give up when our Naval operations at Pearl Harbor were bombed on December 7, 1941.

Panic Selling Exacerbates Bargains

This year feels so much like late in 1981, late in 1999 and late in 2008 to us. The first reaction by investors was to flush whatever they had left in economically sensitive stocks. Then, as if there hadn’t been enough torture for value investors today, Saudi Arabia decided to chop the knees out from under the oil industry in the U.S.

Beware Lazy and Sleepy Investors

Investors have been awoken to the carnage of the last three weeks. These circumstances, while unenjoyable, may be hiding the actual problems with today’s market. The unforeseen circumstances of today are no different than the past.

Viral Collapse of Economic Optimism

Those of you who have been with us recently know that we are calling the recent decline in value stocks a capitulation in a value investing depression. The coronavirus has sucked all the economic optimism out of a market which has hugged tightly to large growth companies providing reliable sales or earnings momentum.

Berkshire Hathaway: No Urgency in the Urgent Zone

To us, Warren Buffett is the greatest value investor of our time. He wrote the annual letter to his Berkshire Hathaway (BRK.B) shareholders on February 22, 2020. This letter happens to coincide with some of his worst relative performance in the last year to five years.

Ethics in Stock Picking

A truly interesting contradiction is developing in stock markets around the world. A number of major corporate executives are calling for businesses to be judged by something other than the net present value of their future earnings or other conventional business/investment metrics.

Buffett on Aesop and Cinderella

In the annual letter to Berkshire Hathaway shareholders in early 2000, Warren Buffett attempted to remind everyone why value investing works, despite the financial euphoria all around him at that time. We will revisit this valuable lesson and draw implications for reviving enthusiasm for value investing at a point eerily similar to early 2000.

The Auto-matic Era Ahead: It’s Greased Lightning!

In a recent piece, Bloomberg journalist Keith Naughton laid out a wonderful counter-argument to the consensus of opinions for what the future looks like. His piece, “Millennials Could End Up Being a Boon to the U.S. Auto Market,” talks about the good news of the auto businesses future via Benchmark analyst Mike Ward’s research.

Beverly (Value) Hillbillies

Our definition of value is to buy meritorious companies at a significant discount to intrinsic value with a high margin of safety. Since doing this is more art than science, the margin of safety is important.

Antithesis of 1981

One of our favorite financial writers is Bloomberg’s John Authers. He recently wrote a tongue-in-cheek article about an investment company by the name of Hindsight Capital. In hindsight, or in the company’s case, Hindsight Capital, he talked about what the firm did and what you should have done over the last ten years to produce outstanding returns.

Newton’s Third Law in Action: ESG

One of the exciting buzz words among advisors and institutional investors is ESG, which stands for Environmental, Social and Corporate Governance. This subject is almost always granted a wonderful panel reception at any conference our firm attends as it is the topic du jour.

Riding Winners to a Fault

In a recent appearance on CNBC, we were asked about what we do with stocks we own which have run-up recently. They asked us how we plan to handle Disney (DIS), JPMorgan (JPM) and Target (TGT) after those stocks enjoyed strong price increases this year.

Teeter-Totter Stock Market

One way of thinking about the share price of a common stock is the price range as a teeter-totter. When the psychology of investors is very negative, enthusiasm for the company hits the ground. On the other end, when everyone is in love with a company’s shares, their end of the board can’t seem to get any higher. Where is the board end hitting the ground currently and who is stuck up in the air on a psychological high?

Keynes’ General Greatness from Chapter 12

In 1936, John Maynard Keynes penned his work The General Theory of Employment, Interest and Money. Most of the work was trying to strike against the consensus of economics. Many in the intellectual communities of the west believed in the classical theory of economics.

When Revenue Growth Collapses

In the revenue growth world of the last five years, this make-believe company would be a huge success story. They would tout a 100% growth in sales the second year and ask investors to ignore the doubling of the loss from $100,000 to $200,000 for the sake of growth.

Risk Blackout

In financial euphoria episodes, investors become immune to the risks of capital destruction by blacking out to their normal risk aversion. Usually these episodes come from extrapolating the recent past out many years into the future. What can we learn from other disciplines about blacking out? How did this happen with investors in the past and where are risks in the U.S. stock market blacked out today?

“Money for Nothin’”: Have we met Dire Straits?

When baby-boomer adults were in their twenties, we sang along with Mark Knopfler and Dire Straits. Their song, “Money for Nothing” defined the era of music videos. We got cable in 1981 and will admit that we were glued to the TV watching music videos of the bands and performers we loved.

Seeing the Baseline

We live in a world defined by change. Anyone in doubt need only wait a few days to be reminded. Humans endeavor to measure it, describe it, and develop strategies designed to control it.

The Milken Approach

Michael Milken rose to the top of Wall Street by way of the Wharton Business School with Drexel Burnham Lambert in tow. Milken’s work at Wharton was founded on the core theory that bond investors were rewarded by taking junk bond risk.

Battle Royal Markets

Over the last ten years we’ve seen the rise of the Battle Royal markets and the shift away from one-on-one investing. There are all sorts of different battle royal’s, but the ones I watched as a kid were the biggest events in pro wrestling...

Maverick Risk

It is human to want to win and we are pre-programmed as children to get what we want quickly. Then we become adults in need of good investment returns and we are forced to operate in longer time frames of five to ten years. Only mavericks want to do what is needed.

Money Goes Where Treated Best

We believe money always goes where it gets treated the best. A recent article detailing the most attractive places in the U.S. for millennials to buy a house included the following cities, and that has implications for investing, not just nesting.

Unforgettable and Uninvestable

One of the all-time classic ballad songs is Nat King Cole’s “Unforgettable.” The song gives us a great picture of what has been going on in the common stock market with meritorious companies which have been thrown in the bargain bin.

Hotel California

As rates fall to zero in most of the world, the line that has been ringing in our mind is “You can check out any time you like, but you can never leave!” This is a chorus investors have sung through their capital allocations. We believe the Eagles provided an excellent understanding of what today’s market is giving investors in their song, Hotel California.

Munger and Icahn Make Oil Investing “Easy”

If you examine the portfolio of the Daily Journal, run by Berkshire Hathaway (BRKB) Vice Chairman Charlie Munger, you will see three main stocks. In 2009, near the market bottom, Munger purchased shares of Wells Fargo (WFC), Bank of America (BAC) and U.S. Bancorp (USB).

A Wizard’s Spell

In a recent interview by CNN’s Fareed Zakaria with Bill Gates the founder of Microsoft, Gates reflected on the wizardry of Steve Jobs and his ability to “cast spells on people.” Since Gates was a tech-magnate in his own right, his “minor wizard” status gave him the ability to identify the spells Jobs cast on employees and the world at large.

The Price of Knowledge

The stock market has a history of torturing highly-valued knowledge. About every seven years a consensus forms around the fastest growing sector of the stock market, or the fastest growing country, or the fastest growing industry.

Political Football Stocks

In today’s missive, we would like to discuss the tribulation arising out of political scrutiny and the sectors or companies suffering at the hands of political football.

Value Investing: Business as Usual

For most millennials like myself the last ten years have formed what we believe the business to be: a bull market reinvigorated by the whims of the Federal Reserve Board. If anchoring is a powerful force in investor behavior, the anchor at the depths of our millennial beliefs is that value hasn’t worked.

The Risk Pendulum

A series of important factors in the U.S. stock market are in play which beg the question, “Are we at the beginning of a risk cycle or at an ending?” The answers will have a bearing on what to own and where to be positioned going forward. These thoughts won’t be exhaustive, but we hope to get you thinking on a few important subjects.

The Inevitables 2

As I watched this year’s Berkshire Hathaway Annual Meeting, one thing struck me. There was sheer enthusiasm around the annual shareholder meeting for anything tech-oriented. Yes, it was disclosed that Berkshire had taken a position in Amazon that Friday, but it goes deeper.

Did Vanguard Kill Wall Street’s Golden Goose?

Many are wondering why the market for Initial Public Offerings (IPOs) has performed so poorly, even though the flood of hot new ones came to market recently. It took three years to choke demand for money-losing dot-com IPO companies back in 1997, even though Federal Reserve Chairman Alan Greenspan called the mania for tech stocks in late 1996 an “irrational exuberance.” What has killed the goose which traditionally laid the golden eggs on Wall Street?

The Beyond Meat Market

We have written a good deal about the parallels of today’s market with the tech and telecom bubble of the late 1990’s. While no two time periods are ever the same, today’s rhymes are eerily similar in some respects, with the latest development in initial public offerings (IPOs) as the latest example.

Berkshire Hathaway Annual Meeting 2019: Who is Judas Iscariot?

Charlie Munger set the tone for the 2019 Berkshire Hathaway Annual Meeting. He said that people involved in creating cryptocurrencies, “honored the life and work of Judas Iscariot.” On many major subjects, questions were fired at Warren Buffett and Charlie Munger related to short comings which self-proclaimed expert observers see at Berkshire

Clash of the Titans

We believe the U.S. stock market will come down to a clash between one very positive forward-looking set of facts and a very negative set over the next ten years.

Today’s Profit Margin Distortions

Late in bull markets there is often a pervasive excitement that arises. At that time, not all profit margins are created equal. Financial euphoria can cause distortions in industries and businesses.

Stock Market Morality

The history of the stock market lays some reliable markers for long duration investors when it comes to these morals. First, in the long run, a basket of the cheapest of the stocks in the S&P 500 Index has outperformed the expensive ones by 3.6% per year...

The Potential Illiquidity Bonanza

We believe there is a severe lack of liquidity in the stock market and it shows itself both directions. Good news is overly capitalized to the upside and bad news is more heavily punished than in prior eras.

Illusionary Investing

My career started in 1994, which was a stealth bear market for stocks and an outright bear market for bonds. Fed Chair Alan Greenspan hiked rates seven times as he played catch up in response to a percolating economy that rediscovered its sea legs coming off the 1991 recession.

Underperforming Like It’s 1999

The singer, Prince, wrote about “partying like it’s 1999.” We can tell you that 1999 was no party unless you owned the most popular tech stocks and the hottest initial public offerings of the latest dot-com company.

Antitrust “Internet Style”

We consider ourselves excellent spectators of competition and look forward to March Madness this month. We are reminded that these very competitive games can’t take place unless there are rules and referees to officiate. Our long-time readers are aware that we have warned of the danger surrounding the aggregation of power by the monopolistic tech behemoths.

Just Do the Math!

We remember looking at demographic charts back in the 1990s which compared the population of the peak borrowing age group (28-40) with the peak savings age group (49-62). At that time, 10-year Treasury bonds were still yielding 7.5-8% and investors wondered where interest rates were going.

Buffett’s Annual Letter: Forest for the Trees

There is an old expression, “You can’t see the forest for the trees.” After reading through Warren Buffett’s 2018 Annual Letter to Berkshire Hathaway shareholders twice, we fielded questions from the media folks who reviewed the annual letter by focusing on very small trees mentioned by Buffett.

Channeling Warren Buffett

The most popular missives we write are associated with Warren Buffett’s annual letter to shareholders and the annual shareholder meeting in Omaha. This year we thought it would be fun to channel Mr. Buffett and attempt to write his letter for him.

Ph.D. in Used to Be

A popular song and a recent article in The Wall Street Journal reminded us of Edmund Burke’s quote and how important history is to the long-term success of common stock ownership.

All the Outcomes are Unknown

We go through life being taught far more certainty than is actually present. Life isn’t black and white, but instead various shadings of grey that end in black or white, only after the fact.

We See Dead Stocks

Financial euphoria episodes are a common occurrence in investment markets and the U.S. stock market. When a new one comes along, market participants accelerate their enthusiasm toward the end, which makes the shares of companies involved dead to us.

Dr. Jekyll Economy Meets Mr. Hyde Markets

In the famous book, Strange Case of Dr. Jekyll and Mr. Hyde, Dr. Jekyll and Mr. Hyde were one human being with a split personality. Dr. Jekyll healed people and Mr. Hyde murdered them. This economic environment and the U.S. stock market have the same kind of split personality.

Price for Clarity

The market hates ambiguity. That’s what we’re told, and on any short-term basis, we can see the market vote accordingly. In a world where investing has morphed towards algorithmic trading systems influencing daily volatility, many have come to accept this as a reasonable truth and participate by selling when things lose clarity or piling in when visibility is perceived.

C.I.a.P. Meets C.R.a.P.

Amazon recently announced that they are combing through the list of things they warehouse and sell to determine which items “can’t realize a profit” (C.R.a.P.).1 We found it very interesting how they are determining which items to pare from their website list.

Academia vs. The Real World – Part 2

We are revisiting our discussion of what the real world is like versus what academics claim in papers and debates. A good way of putting this is “Academia has a tendency, when unchecked (from lack of skin in the game), to evolve into a ritualistic self-referential publishing game.”

Academia vs. The Real World – Part 1

In preparation for a talk, I began to review Sir John Templeton’s track record with the Templeton Growth Fund (TEPLX), which he managed from 1954 to 1991. At the age of 34, with a father that broke into the investment business in 1980, I was very aware of Templeton’s success in his career, but unaware of how the results came to his clients.

The Tortoise Can Beat the Hare

Jessie Livermore was one of the greatest investors of all time. In the book, Reminiscences of a Stock Operator, Livermore explained that the single activity that made him the most money was, “sitting on my hands.”

Well Known Facts Can Hurt You

Our long-time readers are aware that we analyze the U.S. stock market through the prism of what we call “well-known facts.” A well-known fact is a body of economic information which is pretty much known to all market participants and has been acted on by almost everyone with available capital.

If I Fell, Again

Investors have called their five-year love affair with technology stocks into question over the last 35 days. For this reason, we at Smead Capital Management are calling in John Lennon and Paul McCartney’s beautiful ballad “If I Fell” to help answer the following questions.

Housing Consensus Dead Wrong

Most people tend to see what’s right in front of them, especially when it comes to housing affordability. Consider that most of the media organizations in the U.S. reside in the expensive coastal cities. These cities are suffering a decline in home values and contributing to a discussion on what higher home prices and higher interest rates could do to the number of new homes built nationwide.

Jerry Maguire Stock Market

The actor, Tom Cruise, is as enigmatic as the U.S. stock market. He has made many terrific movies over the years and today’s stock market reminds us of his classic sports movie, Jerry Maguire. Jerry was a top sports agent for a large agency and then suddenly, out of nowhere, was dumped out on the street with one client and a top college recruit to work with.

South Sea Forecast: Stockjobbing Becomes Technology

In 1720, the South Sea Bubble arose from what seemed to be good intentions. The South Sea Company was given an exclusive monopoly on the Spanish Americas in exchange for assuming a large part of England’s debt. The debt holders received preferred shares in the South Sea Company that paid 6% interest.

Framing the News

As contrarian investors and students of group-think crowd psychology, we look for investment opportunities in the way news is framed. There is an old Mark Twain saying, “Lies, damned lies and statistics.” We believe investors are getting mislead by statistics surrounding the U.S. economy and we will seek to dispel erroneous assumptions in search of long-term gains in the stock market.

Road Not Taken

We have written profusely about the investment myopia of today which has focused on “growth at any price companies” without regard to profits or free cash-flow. We do this because we know success in investing requires a healthy degree of discomfort for it to be profitable, and we know how much comfort today’s investor has found by owning what has worked.

Crowded Trade Exit

The recent action in the stock market seems to be governed by crowd psychology and reminds us of a theory we created in college called the “coat theory.” Back in the 1970s, the fraternities and sororities at my alma mater hosted several mixers so the students could get to know each other better.

Big Tech’s Three Identical Strangers

The U.S. government must determine how to deal with the negative consequences of some of the last decade’s most successful internet-based businesses. Alphabet, Facebook and Amazon grew up as strangers and have developed monopolies in search, social media and in e-commerce.

Disciplined Opportunism: Templeton and Price Revisited

For Templeton and Price to execute a “new era” approach today, we believe they would likely advocate avoiding the S&P 500 Index, mutual funds and ETFs, emphasizing growth stock investing and they would be very careful with ownership of anything related to technology. Price recognized that growth eras don’t continue forever and Templeton went wherever he thought he could make great money buying companies at depressed prices with positive economics. We believe our eight criteria for common stock ownership will shepherd us through this “new era.”

The Temperature of Market Leadership

At Smead Capital Management, we want to avoid excitement and expense in the marketplace. When a sector of the stock market gets white hot, there are usually a few stocks which dominate the market activity and see explosive price appreciation. We like to think that one of them becomes the thermometer of the market, in effect showing the temperature of the stock market.

Smoked in 1999 or Vaped in 2018 What You Pay Buying Shares Matters

It is no secret that the U.S. stock market has been completely addicted to discounting the future success of the most popular technology stocks. Momentum-based growth investing has had many bouts of success in the past, but this is the first episode in an era where indexed mutual funds and exchange traded funds (ETFs) were the largest aggregate owners of the largest capitalization companies.

Investment Humility and Economic Recovery

We make every effort to understand the way that investors go to extremes over what we call the “well-known fact” in the stock market. A “well-known fact” is a body of economic information which is known to virtually everyone in the marketplace and has been acted on by anyone with capital.

The Jim Carrey Parable

Today’s popular stocks have literally overwhelmed the stock market in the last four years and six months. To understand today’s financial euphoria, we will analyze three terrific movies made by the actor, Jim Carrey. In Liar Liar, The Truman Show and in Bruce Almighty, we learn morals which we believe should guide us in the long-duration investment process.

Global Dominance via Stocks, Not War

In the 1960’s, the slogan “Make Love, Not War” became a rally cry for anti-war protestors, but also typified their free love expression. They used the slogan to explain the harshness of the situation in Vietnam and to be countercultural to the capitalist and traditional way of life they saw in American society.

The Encore

The stock market has put on quite a show over the last decade. Including dividends, domestic stocks have nearly quadrupled since the bottom in March 2009. Most of the crowd missed the best parts of the broader show, but that hasn’t stopped the excitement being built around the encore.

The Voting Machine vs. The Weighing Machine

The patriarch of value investing, Ben Graham, once said, “In the short run the market is a voting machine, but in the long run it is a weighing machine.” His statement is just as profound as the day it was first spoken. However, it is timelessly mystifying to most investors.

2018: The Math is Simple

We believe the math of common stock investing is pretty simple. When you buy a stock without leverage, you can only lose your original investment. Your gains can be unlimited over the longest term (long duration). Most of the benefit (90%) of diversification is reached by owning a twelve-to-eighteen stock portfolio...

Zero Cost of Capital

Massive investor popularity can produce some pretty strange circumstances in the U.S. stock market. Mark Twain said, “History doesn’t repeat itself, but it rhymes!” Today’s strange occurrence has been called a “zero cost of capital” and it rhymes with what happened in 1999-2000.

Imagining the Stock Market in Ten Years

What will the next ten years look like in the U.S. stock market? As we often do, we refer you to one of our favorite songs, “I Can Only Imagine,” and a book by George Friedman, The Next 100 Years. We believe the best performing securities of the next ten years will be very different from the securities and the sectors which currently capture the “popular imagination” of investors.

Berkshire Hathaway Annual Meeting 2018: A Mirage of Feelings

Much like the 1975 Billboard top ten hit song, Feelings, Warren Buffett and Charlie Munger laid out their feelings on a variety of issues in Omaha at the Berkshire Hathaway (BRKB) Annual Meeting. We believe even the greatest investors of all time are being influenced by a mirage.

Stretching for Gilded Poles

Elon Musk is possibly the most interesting man in the world, in our opinion. His nobility comes from his past as a founder of PayPal, but his popularity only grows in this era as he seeks to tackle big projects that include the car business, space, mass transit and other subjects.

Mr. Market Grasps the Esoteric

We are reminded of Ben Graham’s Mr. Market analogy. In his analogy, the stock market is like having a business partner (Mr. Market) who offers to either buy or sell his half of the business to you, based on how the business is doing.

The Good Shepherd Investor

David was the King of Israel and the writer of many of the Psalms. He spent his formative years as a shepherd and framed his life’s work around the key concepts from his profession. Herds were the primary form of wealth back then, while common stocks are a primary form today.

Is Good Health Worth the Cost?

Healthcare companies overcome great risks to succeed, but can gain incredibly profitable businesses in the process.

The Heart of the Matter

I came across a book titled The Matter of the Heart by Tom Morris that is a great history of the medical accomplishments and advances for the human heart. Mr. Morris details eleven operations and their evolutionary success over the course of the book.

Betting Against the Flows

Money flowed into passive investment vehicles at an ever-increasing rate in 2017. It was a record year for these products designed to replicate a stock market index and agnostically own a basket of securities without discretion.

The World is Not Enough

A few weeks ago, I caught myself pulled in by an old James Bond classic, The World is Not Enough, starring Pierce Brosnan. In the movie, an oil heiress, Elektra King, is kidnapped. While in captivity, she becomes a victim to Stockholm Syndrome and plots with her captor to destroy an oil pipeline running to the Bosphorus Sea. There is a scene in the movie that encapsulates where we are in today’s stock market environment.

Buffett Whispers of Danger

In the 2017 Berkshire Hathaway Annual Letter, Warren Buffett told us what he is doing, and, in as quiet a voice as he could use, what he says to do. Our readers will not be surprised at our summation of Buffett’s letter, but here we go anyway.

Minority Report

In the movie, Minority Report, Tom Cruise plays a policeman in a world where crimes are predicted ahead of time. Cruise’s character gets accused of a future murder and he is forced to work incredibly hard to acquit himself of the anticipated crime.

Buffett’s, Bezos’ and Dimon's Tapeworm

Warren Buffett, Jeff Bezos and Jamie Dimon recently announced that their three companies will form a non-profit entity to attempt to drive down healthcare costs for them and possibly other companies. In the process of making the announcement, Buffett called the healthcare sector of the U.S. a “hungry tapeworm” in the economy.

Value Investing’s Dark Hour

Is the underperformance by most large-cap value investing strategies in this lengthy bull market the “darkest hour” for value investors? This is the longest underperformance stretch of four relatively poor stretches for value in the last 80 years.

Risk is Not High Math

Long term success in common stock ownership is much more about patience and discipline than it is about mathematics. There is no better arena for discussing this truism than in how investors measure risk. It is the opinion of our firm that measuring a portfolio’s variability to an index is ridiculous, because it is impossible to beat the index without variability.

Valuing Uncertainties

As we enter 2018, numerous uncertainties are dominating the minds of American citizens and investors. We are happy to weigh in on what we consider to be both un-useful and useful uncertainties as they pertain to long duration ownership of common stocks.

Confusing Brains with a Bull Market

It is hard to think about 1981, my first full year in the investment business. Three-month Treasury bills were paying 18%, longer-term Treasury bonds yielded 15% to maturity and cheap stocks got 20% cheaper. In the summer of 1981, we saw a stock market decline from an already depressed market trading at eight-times after-tax profits down closer to six times.

Gold Rush to Tech Rush

Over the weekend I stopped to watch the last part of a James Stewart Western called, The Far Country. It was the story of two cattle drivers who took their cattle all the way to the Yukon to get a piece of the late 1890’s Klondike gold rush.

Capitalizing Potential

A massive amount of stock market capitalization is tied up in companies based on both their potential market share and hypothetical future profits. The popular arguments in their favor come from looking at a company’s total addressable market (TAM). Sky high price-to-earnings ratios and massive capitalizations are common in companies with a large TAM as we finish up 2017.

Investing Like the Mafia 2017

As famed market strategist Richard Bernstein has pointed out, investors should pattern common stock selection after the investment style of the Mafia. What causes the Mafia to get such good returns? How do they spot opportunities? Why should we as investors in publicly-traded common stocks emulate their behavior near the end of 2017?

Today’s Financial Euphoria

All major financial euphoria episodes hold aspects in common. Among our favorite books on investing is John Kenneth Galbraith’s A Short History of Financial Euphoria. More than any other economist, we admire his understanding of the connection between the securities markets and the economy.

Rise of the Rest

The first time I read Forbes magazine was in 1980 as a brokerage trainee in New York City. I was fascinated by the company stories and the way the top investment disciplines were analyzed. In the 100th Anniversary Issue—published in September 2017—over 100 successful business and investment people wrote a short essay.

Buying Value in a Good Ol’ Bull Market

Many well-regarded experts have weighed in on the length and the pricing of common stocks eight and one half years into this bull market. They range from the dire warnings of perma-bears like Marc Faber to more reserved warnings from Howard Marks and Robert Shiller.

Value’s Lazarus Moment

In the Bible, Jesus arrives to help his friend Lazarus a few days after he had already died. His friends Mary and Martha were very disappointed because they thought all hope was lost. As the story goes, Jesus raised Lazarus from the dead.

Large-Cap Value Farming

Value investing is very similar to farming. A farmer needs fertile ground, well-planted seeds, unshakable patience, loads of sunshine, watering and weeding, as well as a great deal of courage and faith to succeed in the long run. Today, we believe that investors need to reexamine the benefits of a value investing approach toward the end of an era which has rewarded growth stock investing.

We Didn’t Start the Fire

What should long-duration common stock owners like us do with the news of the horrific flood in Texas, the Category 5 hurricane in the Caribbean, the heightened tensions created by North Korea’s Dictator, Kim Jong-un, and the 8.1 magnitude earthquake in Southern Mexico? What is wise behavior in a more volatile stock market environment created by outside events?

Intense Bargain or Value Trap?

As value managers, we are often asked if a company whose stock price is down substantially is a value trap. This is especially true when we are auditioning new holdings. We like to buy a company with a long history of success when it falls deeply out of favor for one reason or another.

Foregone Conclusions Become Well Known Facts

We’ve heard Warren Buffett continue to repeat an important phrase, “what the wise man does in the beginning, the fool does in the end.” This begs the question, when does a foregone conclusion become what we call “a well-known fact”?

Death of the Internal Combustion Engine

The stock market is discounting an accelerating rate of technological change in our society. A mad dash by investors is anticipating a world organized like “The Jetsons” cartoon from my childhood. We thought it would be useful to look back at other points in time where great technological change was anticipated and see how that worked out for S&P 500 Index investors.

Get Rich Slowly

A Forbes article of July 1974 profiled John Templeton and highlighted some of the wisdom he implemented in his investment process. The article touched on his discipline of consistently praying to God “for wisdom and clear thinking” at the start of each directors meeting for the Templeton Growth Fund.

What Doesn’t Kill You Makes You Stronger!

As we look out into the second half of 2017, it is important to understand that we believe the U.S. stock market has tried to “kill” investor enthusiasm. We would argue this enhances the position of the value-oriented and long-duration equity manager in a way that that doesn’t kill us and makes us “stronger.”

Hey, You, Get Off My Cloud

Walmart (WMT) recently made it clear to vendors that they should “get off” Amazon’s Cloud. This was one of two announcements which speak to the competitive landscape of business in the U.S. The other announcement came earlier when Amazon (AMZN) disclosed an agreement to buy Whole Foods (WFM) for $42 per share in cash.

The General Theory of Reverse Float

During the most-recent Berkshire Hathaway Shareholder Meeting, Warren Buffett and Charlie Munger reiterated a point during the question and answer portion that has stuck with us. We feel compelled to share what we learned.

The Only Game in Town

At the end of my freshman year in college (1977), my brother-in-law’s twin brother called me to ask if I wanted to go to the sixth game of the NBA Finals in Portland. I was a huge Trailblazer fan and was thrilled to sit in the top row of Memorial Coliseum, which held 12,665 fans. Not only was it an unbelievable experience for a lifelong fan (the Blazer’s won), but it was even more powerful because professional basketball was “the only game in town.” No other major professional sport (football, basketball, baseball) existed in Portland in 1977 and there is only one in town today.

Revisiting Buffett’s 1999 Warning: Interest Rates, Orgies, and Value

We thought it would be very helpful to review Warren Buffett’s argument in 19991, the last time there was very high expectations attached to technology stocks and to the overall level of common stock prices. We will reference Buffett’s quotes by the year he said them. The sections labeled 2017 offer our current observations on the markets and thoughts from respected experts.