Key Points

- Adding some perspective on markets courtesy of my dual role at Schwab/Windhaven.

- Analyzing the pros and cons of today's market/economic landscape.

- Looking at the history of Septembers in general, and during midterm election years.

Additional perspective

Welcome back from the summer! As many readers probably know, a new role was added to my Schwab responsibilities about two months ago when I was named Chair of the Investment Committee at Windhaven Investments. Windhaven came under the Schwab umbrella nearly four years ago via Schwab's acquisition of the company. Soon after the acquisition, I joined Windhaven's Advisory Board and therefore was intimately aware of its investment process before more formally joining the investment team. And in the interest of full disclosure, I also have my retirement assets in Windhaven.

Windhaven manages global investment strategies which may include exposure to US and non-US stocks, bonds, and real estate; as well as hard assets (e.g. commodities including gold) and currencies. We seek investments with low correlation to each other such that when one asset class is down others are up, thus attempting to provide a "natural hedge."

We do not invest in individual stocks or bonds (micro-level investing). Instead we believe that macro-level investing (in asset classes) provides the greatest chance to discover and capitalize on trends in the global economy. We have found that Exchange Traded Funds (ETFs) are generally the best investment vehicle available to achieve our desired exposures to our universe of asset classes.

This has been an exciting two months for me. Some readers and clients may not be aware that the first half of my 28-year career was spent managing money. In fact, in the first 13 years, I worked for the late, great Marty Zweig—one of the pioneers of tactical asset allocation (the general strategy employed by Windhaven). It's invigorating to get back in the money management saddle again and I hope the additional perspectives on global markets and asset classes I can share with all of you (regardless of whether you are Windhaven investors) will be additive to the caliber of research you appropriately demand from all of us at Schwab.

Now on to the topic of today: Is the market ready for a breather?

I remain a secular bull on the US stock market, which is also reflected in Windhaven's positioning (the highest rankings among asset classes in the Windhaven model include US equities and US/global real estate). But bull markets can and should take breathers. We are not suggesting running for the hills; just suggesting that getting overly greedy doesn't make sense in today's environment. We believe one of the investment themes developing is of global divergences; in terms of economic traction, inflation/deflation risks, and central bank policies. It points to the rising benefits of global diversification and a greater focus on more tactically-oriented asset allocation. It also shows the dominance of the US economic position globally (and why the Fed is ahead of most other global central banks in moving toward tighter monetary policy).

Pros and cons

The cleanest way to set up the discussion is to put together a simple pros/cons list. It's a common way for me to think through theses. These apply to a combination of the US stock market and economy.

Pros:

- P/Es and earnings rising simultaneously

- P/Es remain reasonable

- Consumer confidence rising

- Generally rising/strong leading indicators

- Booming ISM manufacturing index (particularly orders)

- Better housing data

- Better employment conditions (surging JOLTS, plunging unemployment claims)

- Capital spending story kicking into gear

- "Wall of worry" still intact

- Lower energy/commodity prices good for US consumer

- Stronger dollar

Cons:

- Flattening yield curve

- Rollover in inflation expectations (deflation concerns rising)

- Potential for earlier Fed tightening

- Elevated optimistic sentiment (contrarian indicator)

- Seasonals (September)/election cycle

- Wage growth still weak

- Consumer is more price/rate-sensitive (not levering up/spending like in past)

- Volatile real GDP from quarter-to-quarter

- Low market volatility (contrarian indicator?)

- Geopolitics

Rate hikes coming sooner?

I won't tackle all of the above, but want to point out some highlights. One key risk for the market could be a move forward of rate hike expectations. The next spew of economic data releases will be key. The most recent roster have been largely to the better side; including the upward revision to second quarter US gross domestic product (GDP). I don't tend to focus much on GDP as a stand-alone economic indicator given its highly-lagging and highly-subject-to-revision nature. But it does help put the more leading economic readings of late into context.

|

% of real GDP |

1Q14 annualized Q/Q % change |

2Q14 annualized Q/Q % change |

|

|

Consumer spending |

68.2% |

1.2% |

2.5% |

|

Government spending |

18% |

-0.8% |

1.4% |

|

Net exports of goods & services |

-2.9% |

(1.7)* |

-0.4 |

|

Fixed investment |

16.2% |

0.2% |

8.1% |

|

Change in private inventories |

— |

(1.2)* |

1.4 |

|

Real GDP |

-2.1% |

4.2% |

Source: Bureau of Economic Analysis, as of June 30, 2014. *Represents contribution to percent change in real GDP. Numbers may not add up to 100% due to rounding.

Capex cycle kicking in?

Although sub-3% growth in consumer spending—matters, given that it accounts for two-thirds of US economic growth – another important section is investment. Both residential and non-residential investment are now humming, suggesting a more robust capital spending (capex) cycle may be finally kicking in.

The fact that economic readings have been more mixed lately could be a disguised blessing in that July's Federal Open Market Committee (FOMC) meeting minutes reflected some concerns about overheating economic conditions.

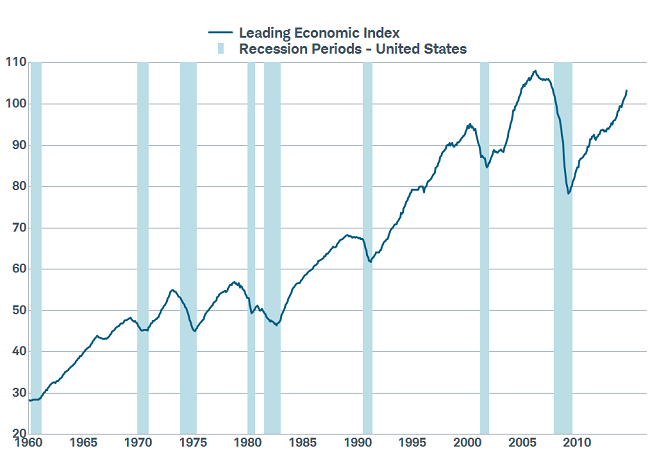

Recession risk extremely low

The good news from a market perspective is that the risk of a recession appears to be quite remote. As healthy as a short-term correction would be for the market; a bear market would not be welcome. But it's highly unlikely given the low risk of a recession. The most reliable of the leading indicators are far from recession-warning levels, there's no overheating in the cyclical areas of the economy, and the Fed is highly unlikely to "induce" a recession via sharply higher interest rates.

See a chart of the Conference Board's Leading Economic Index (LEI) below—there is none of the deterioration seen in the past heading into recessions (shaded bars).

LEI Not Warning of Weakness

Source: FactSet, The Conference Board, as of July 31, 2014.

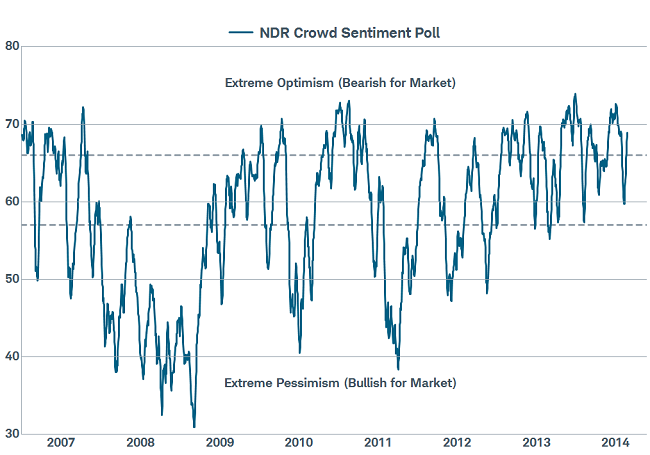

Stretched sentiment

The primary vulnerability I see is tied to the recent high level of bullishness, a contrarian indicator; and some seasonal/election cycle tendencies. A common blended sentiment index I track is Ned Davis Research's Crowd Sentiment Poll, which not surprisingly is showing a pick-up in optimistic sentiment alongside all-time highs in stocks.

Sentiment Heading Back Toward Extreme Optimism

Source: FactSet, Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2014© Ned Davis Research, Inc. All rights reserved.), as of August 26, 2014. The Crowd Sentiment Poll® is a sentiment indicator designed to highlight short-term swings in investor psychology. It combines a number of individual indicators in order to represent the psychology of a broad array of investors to identify trading extremes.

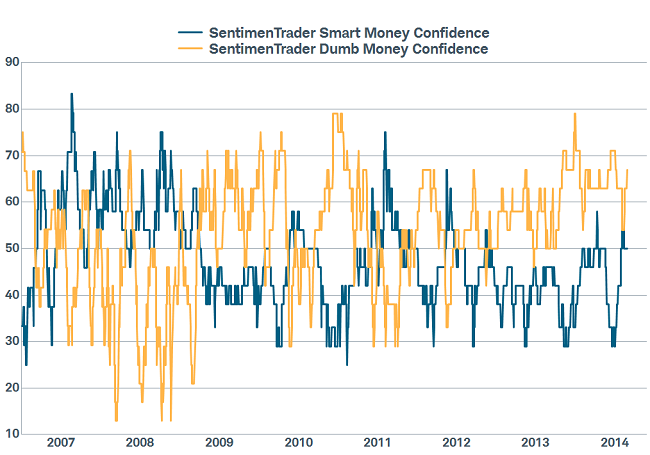

A more unique analysis of investor sentiment comes from SentimenTrader.com via their "Smart Money/Dumb Money Confidence" indicator (see the footnotes below the chart for their definitions of each cohort). As you can see, "dumb money" confidence (the contrarian indicator) has spiked recently; while "smart money" optimism has rolled over. Neither are at the kind of extreme they were in advance of the most recent 4% pullback, but it bears watching.

"Dumb Money" Confidence Up

Source: SentimenTrader.com, as of August 29, 2014. According to SentimenTrader, you want to follow the Smart Money traders when they reach an extreme. Examples of Smart Money indicators include the OEX put/call and open interest ratios, commercial hedger positions in the equity index futures, and the current relationship between stocks and bonds. You want to do the opposite of what the Dumb Money is doing when they are at an extreme. Examples of Dumb Money indicators include the equity-only put/call ratio, the flow into and out of the Rydex series of index mutual funds, and small speculators in equity index futures contracts.

September … ugh

It's also September, which is personally depressing since I turn 50 this month. But it's also a weak month historically for the stock market (the weakest in fact). For the Dow, which has a longer history than the S&P 500, September is the only month that has a negative average monthly percentage change going back to 1900 (-0.83%). It also has the lowest percentage of positive readings of all twelve months (43%). For what it's worth, though, over the past 20 years, both August and June have worse readings for average monthly declines.

You can see the details for the S&P 500 (since its inception in 1928) in the table below.

S&P 500 Septembers since 1928

|

Average |

Median |

% positive |

|

|

All Septembers |

-1.07% |

-0.42% |

45.3% |

| Up YTD into September | 0.21% | 0.06% | 50.0% |

|

Down YTD into September |

-3.45% |

-1.64% |

36.7% |

Source: Bespoke Investment Group, LLC (B.I.G.).

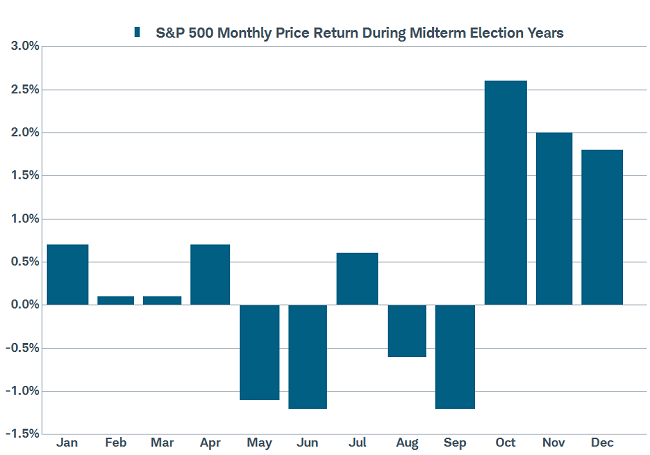

And of course, it's a midterm election year. I've shown charts around this countless times this year; but here's a breakdown of monthly performance historically in midterm election years. As you can see, September is tied for the weakest month historically. But importantly, it is followed by the three strongest months of midterm election years … by far!

Weak Septembers in Midterm Election Years

Source: Strategas Research Partners LLC. Average returns for 1930-2010.

The net

Interest rates and seasonal tendencies are taking some attention away from the stronger economy and pose short-term risks for the stock market. Another pullback would be welcome from a sentiment perspective and would not dent our longer-term optimism that we are in a secular bull market that still has room to run. But just as fear has been the strongest emotion keeping many investors out of this bull market, greed is an emotion to rein in as well.

© Charles Schwab