Key Points

- It's time for another reminder about the perils of panic.

- Asset allocation, diversification and rebalancing are as close to a "free lunch" as you can get as an investor.

- In a world where time horizons have shrunk precipitously, think longer term.

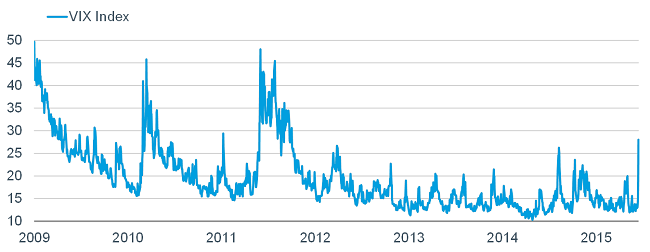

If markets are good at one thing, it's reminding investors that they don't go up uninterrupted forever. The US stock market went over 1,000 trading days between its 2011 correction and the one we’re in the midst of presently. Normally, corrections—defined as declines of at least 10%—occur about once a year. As the chart below illustrates, the CBOE Volatility Index® (VIX) has spiked. Last week’s move was the largest for a single week in the history of the VIX, albeit nowhere near the peaks between 2009 and 2011.

Fear up, but well down from highs

Source: FactSet, as of August 21, 2015.

We’ll have plenty of shorter-term commentary on the latest market moves, but this piece is longer-term and more evergreen in nature. It serves to remind investors that neither panic nor greed is an investment strategy, and that the best foundation to help protect a portfolio against the unpredictable is having—and sticking with—a long-term strategic asset allocation plan.

Mindset matters: Strategic trumps tactical

Individual investors should rarely, if ever, react in a purely emotional fashion to a dramatic short-term move in the market. As intriguing as it may seem to try to catch bottoms and get out at tops in order to reap big profits (or so you think), the "tactical" (or shorter-term) approach to investing has its limitations ... and its risks. That said, if you're a regular reader of our shorter-term commentary, we've been in the neutral camp (neither over- nor underweight) on US stocks all year—our most cautious stance in the past several years.

We believe it's the "strategic" (longer-term) asset allocation decision—and the ability to stick with it through the discipline of rebalancing—that will ultimately reap the greatest rewards. These decisions are not a function of short-term market gyrations or forecasts (mine, yours or anyone else's), but are tied to your risk tolerance and long-term goals. Developing and maintaining the right long-term asset mix is by far the most important set of decisions an investor will ever make.

Never before has information about the global economy and markets been more readily available and disseminated. As a result, global markets have become highly interconnected. In turn, our reaction mechanisms are heightened, and investor time horizons have shortened dramatically—but not necessarily to our advantage. Yes, the long term is really just a series of short-term events, but it's how we react to them that decides our ultimate fate as investors.

Asset allocation and diversification: Investors' "free lunch"

One of the most important areas where Schwab offers advice is the development of a long-term strategic asset allocation plan. Many investors assume that their position along the risk spectrum from conservative to aggressive is largely based on their age and time horizon. But a more important factor is risk tolerance. Also important is judging the difference between an investor's financial risk tolerance (the ability to financially withstand volatile markets) and emotional risk tolerance—a spread that's often quite wide and acknowledged only during tumultuous market environments.

I've known plenty of older, close-to-retirement investors who thrive on the risk associated with an aggressive investment stance. I've also known plenty of young investors, with multi-decade time horizons, who can't stomach any losses. Too often, investors use a rearview mirror to make investing decisions, by looking at past performance as a guide to future results. A mirror is a valuable tool but only when turned on yourself to judge your own circumstances—tolerance for risk, time horizon, income needs, etc. As I've often said, there are very few free lunches in investing. Asset allocation, diversification and periodic rebalancing are as close as you get.

Risk tolerance: Know what you can stomach

Clearly, over the long term, given the better performance by riskier asset classes, a more aggressive allocation has historically reaped higher rewards in terms of returns. But there is a dark side to an aggressive posture's higher returns—the risk taken in getting there. Aggressive portfolios’ higher historical returns have had a much wider range of returns (i.e., a higher standard deviation, with greater “drawdowns” and volatility) and, most importantly, are generated only through "stick-to-it-iveness."

Many investors have learned the hard way that their tolerance for a big loss in the short term was less than they thought. And to maintain an aggressive allocation, they generally had to rebalance in favor of the asset class(es) that generated those steep losses and away from the asset class(es) that had weathered the storm.

Conservative investors should heed the lesson as well. A conservative portfolio’s lower historical returns have come with significantly less drawdown and volatility. For some, it's worth the lower return for the sleep-at-night benefits. But the reality is that many investors want all of the upside when markets are performing well—but none of the downside when they are not. That is highly unrealistic.

We believe that rebalancing to maintain risk-tolerance-appropriate allocations is the best way to generate healthy long-term returns. Rebalancing is often the real test—a test that is administered more often during times of increased volatility. But the practical way to think about rebalancing is that your portfolio will tell you when it's time to trim from or add to an asset class because of the appreciation or depreciation that’s occurred in various asset classes. You don't need to rely on anyone's forecast of what may or may not happen. Rebalancing forces us to do what we know we’re supposed to do, which is “buy low, sell high.”

Market timing: A dangerous game

It's enticing to try to catch the next big investment wave (up or down) and allocate assets accordingly. But there are very few time-tested tools for consistently making those decisions well. Unfortunately, rearview-mirror investing—or performance chasing, either up or down—never seems to go out of style.

Time horizons: The longer, the better

Based on several well-known studies, the length of time that individual investors hold stocks, mutual funds and exchange-traded funds (ETFs) has shrunk precipitously over the past 50 years. Back then it was common for investors to have five-to-10-year time horizons, but today they are typically well less than a year, exacerbated by the proliferation of high-frequency/algorithmic trading firms. These firms are considered price-insensitive buyers and sellers—typically trading based on momentum and purely technical factors, with time horizons measured in nanoseconds. This is decidedly not a game individual investors should try to play. Individual investors should be price-sensitive buyers and sellers. We still strongly believe that over the longer term, fundamentals will define how markets behave.

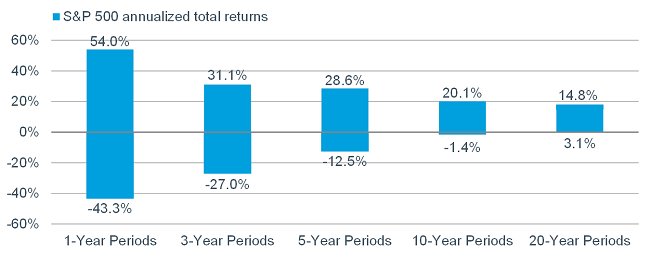

In the chart below, you can see the power of long holding periods when it comes to minimizing downside risk. The longer you extend your time horizon, the less likely you'll experience a loss over that holding period.

Longer time horizon = lower downside risk

Source: Schwab Center for Financial Research with data provided by Standard and Poor's. Every 1-, 3-, 5-, 10-, and 20-year rolling calendar period for the S&P 500 Index was analyzed from 1926 through 2014. The highest and lowest annual total returns for the specified rolling time periods were chosen to depict the volatility of the market. Returns include reinvestment of dividends. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is no indication of future results.

Patience and stick-to-it-iveness

Admittedly, the development of a long-term strategic asset allocation plan isn't the hard part—it's sticking to it that often becomes the real challenge. Adding to underperforming asset classes and trimming outperforming asset classes goes against the emotions of fear and greed that often drive investment decision making. But if we learn from our mistakes, use our brains over our hearts and look to our portfolios as rebalancing guides, we can expect a more successful investing future and maybe even get a free lunch along the way.

© Charles Schwab