Key Points

- Stock buybacks are on track to bust all prior records in 2015.

- We take sides on the debate about whether they're for-good or for-bad.

- Are buybacks to "blame" for weak productivity?

A common question I’ve been getting at client events lately is about stock buybacks and the effect they’re having on earnings-per-share (EPS); as well as what they say about the economy overall and investor/business psychology.

First, the numbers

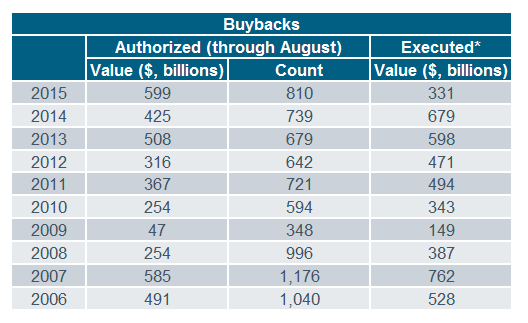

Birinyi Associates does a monthly tracking of authorized and executed stock buybacks. There were $47 billion of buyback authorizations in August, a 15% increase year-over-year. Year-to-date buyback authorizations, at 146, have eclipsed full year totals from 2008 through 2012, and are up 40% year-over-year. Based on the data year-to-date, buybacks are at a run-rate to a record $897 billion of announced buybacks in 2015—this would be the largest of all-time, as you can see in the table below.

Source: Birinyi Associates, Inc., as of August 31, 2015.

*Executed figures are full-year. Authorized is year-to-date for all periods.

Critics of stock buybacks argue they are manipulating EPS, and therefore stock prices; are depressing job growth; and/or are hurting the US economy overall. As per the first argument, it’s also the critics’ contention that companies buying back their own stock are sacrificing longer-term capital investments for the benefit of returning cash to shorter-term oriented hedge funds and other investors. I don’t happen to be one of those critics.

Let’s distinguish what a stock buyback is—it’s the other side of the stock sales coin. Companies sell shares of equity to raise capital. They buy back shares of equity to retire capital. Those decisions are part of the process known as “capital allocation,” which is essential in a capitalistic economy in that it directs money to areas where it’s most productive.

There are generally two primary reasons why companies buy back their own stock: 1) they believe their stock is undervalued and a cheaper place to deploy capital than other alternatives, like capital spending or mergers/acquisitions; 2) they have amassed more capital than their company can spend/invest profitably. Remember, over-capitalization can be just as problematic as under-capitalization. The effect of a buyback is to increase EPS, since the company’s future profits will be divided among fewer shares.

Tie in to Fed policy

Many argue that excess Fed liquidity, zero interest rate policy (ZIRP), and the ability of companies to leverage both, have led to a manipulation of earnings. But Strategas Research Partners looked at the growth rate of revenues and earnings on both a notional dollar and a per-share basis and found that share buybacks have had little to do with the rapid rebound in earnings. Operating EPS are up 119% since the market’s low in March 2009; while operating earnings in notional dollars are up an even greater 122%. It appears that lower interest expense and the ability of companies to restrain labor costs have had a much bigger impact on profits.

Indeed, ZIRP has made it extremely cheap for companies to borrow money to buy back their shares; with several of the world’s most well-known investors recently warning about this—including BlackRock’s Larry Fink and GMO’s Jeremy Grantham. It’s arguably one of the distortions that has arisen from the still-emergency level of interest rates and accommodation—a can that was kicked down the road yet again last week when the Fed maintained ZIRP.

Buybacks suggest weak investment?

Stock buybacks don’t necessarily indicate weak investment, especially when capital is abundant, like today. According to Thomson Reuters, global companies have about $7 trillion in cash; and additional data from the National Science Foundation shows an uptick in US business investment in research and development (R&D)—which has not only been outpacing overall economic growth in recent years, it’s actually outpacing historical trends. The data does not indicate a crisis of business investment in innovation. Data from the Federal Reserve shows that private capital investment—an even larger ticket item than R&D—has also been increasing and is at historically high levels of gross domestic product (GDP).

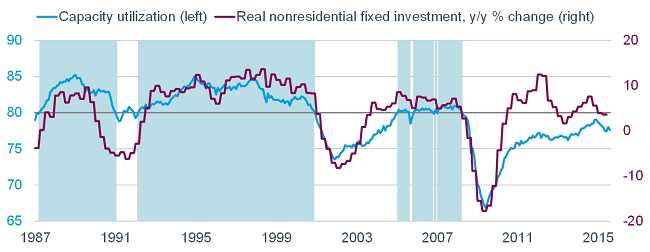

A recent report from Bain showed that the world is currently awash in capital and many companies have more money than they can invest productively. At the same time, as you can see in the chart below, capacity utilization remains below the critical 80% level—at and above which capital spending (aka fixed investment) tends to kick into higher gear. Companies with excess cash should arguably not invest in new equipment/machinery/structures until they are ready to fully utilize their existing stock. We are not quite there yet in this expansion.

Capacity Utilization Sub-80%

Source: FactSet, Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2015© Ned Davis Research, Inc. All rights reserved.), Strategas Research Partners LLC. Capacity utilization as of August 31, 2015. Nonresidential Fixed Investment as of 2Q15. Blue-shaded areas indicate periods when capacity utilization was greater than 80%.

So, how do we square this data with the near-record high average age of a variety of fixed investments in the United States? Some of it lies with the public sector, given that public sector investment in infrastructure is massively underfunded. The American Society of Civil Engineers gives US infrastructure a grade of D+. Spending a lot of time in New York City’s airports and train stations, I frankly question the “+”.

Tax considerations

Often when companies have excess capital, the best thing they can do is return it to shareholders; and stock buybacks—unlike dividends—allow investors to defer taxes. To some, that may be viewed as a flaw in our tax system—and there are an uncountable numbers of flaws in our tax system—but that’s not the fault of corporate executives. Companies are making logical choices based on incentives; an appropriate bi-product of capitalism.

There is no benefit to a company sitting on cash—it should always try to put it to work; if not in its own operations/investments, then back to its investors so they can deploy it. Money returned to investors—whether through buybacks or dividends—does not disappear, it gets deployed elsewhere. In fact, much of the money that old-guard companies have been returning to shareholders is going to fund new, and generally more cash-starved companies. Case in point, the venture capital market has reached dot com era levels, and has brought to the market an unprecedented number of billion dollar startups. In sum, companies are bothincreasing investments and returning the excess to shareholders to be invested elsewhere.

Bad signs

There are cases of potential problematic conduct regarding buybacks, however. One example would be if a company is significantly levering up its balance sheet to buy back its stock. This will sometimes occur if much of the company’s excess cash is tied up offshore. Another example is when a company buys back its stock to offset the dilutive effect of stock-based compensation for its employees, vs. using it to retire outstanding shares. For investors who take an active approach in picking individual stocks to buy, it’s important to dig a bit into each company’s buyback program to make sure the money is being put to work properly.

Productivity connection?

Many also tie record-breaking buybacks to the current low level of US economic productivity; in that companies have not been investing in longer-run productivity-enhancing projects/equipment. There’s another theory behind weak productivity growth though—often called the “new economy” theory. I am intrigued by this theory; recently laid out in an interesting GavekalDragonomicsreport. The theory posits that the apparent productivity slowdown is a statistical illusion caused by rapid technological change.

Traditional data methods become unreliable in periods of rapid technological and structural change when a growing proportion of consumption and employment growth is generated by services that did not exist in earlier periods or were run on different business models. As many “old economy” activities have been replaced by online services operating on totally different business models and often delivered free at the point of sale. Such businesses are underestimated or even missed completely in GDP and productivity statistics, even though they provide services of huge economic value. And, back to the tax component of the argument; many newer business are organized to minimize the value-add they reveal to tax authorities, and therefore also to official data-gatherers.

In sum

Stock buybacks are not the market’s bogeyman—when done right, they can reward shareholders and share prices, and reallocate capital to where it’s most productive.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

(0915-5984)