Key Points

- The October FOMC meeting’s statement dropped the concern about global developments, raising the likelihood of a December rate hike.

- Slow rate hike cycles have historically been more amply rewarded by stocks than fast cycles.

- But questions remain about whether markets can escape the "Fed policy loop."

The Federal Open Market Committee (FOMC) issued a more hawkish statement last week alongside its decision to keep interest rates unchanged. The forward guidance section of the statement was worded (emphasis mine) to focus on "whether it will be appropriate to raise the target range at the next meeting." And although it waxed more dovish on employment, it dropped the line from the prior meeting’s statement about global developments, which the FOMC had specifically cited as a reason to hold rates steady in September.

The Fed is keenly aware of the equity market implications of statement wording—notably that investors would hone in on the "next meeting" sentence in particular. This appears to have been a purposeful push to raise expectations for a move before year end.

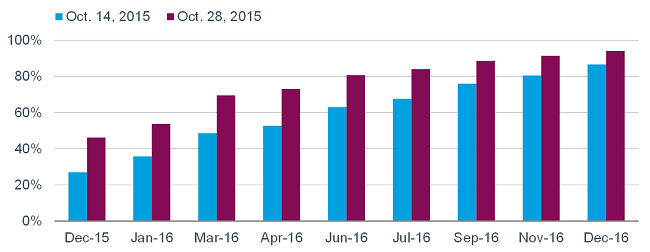

Door for December hike opens wider

Although as you can see in the chart below, expectations for a December hike did jump after the meeting, at 48% they remain less than an even bet. It’s possible the rationale for the more hawkish statement was to reset expectations; which had plunged after the September meeting. Well put by BCA Research (emphasis mine): "…the hawkish language was designed to give the Fed more maneuverability, as well as to restore the view that it was the FOMC, and not the investment community, that was in charge of monetary policy."

Probability of Fed Funds Rate Move

Source: Bloomberg.

As seen above, and as would be expected, not only did expectations for the Fed moving in December rise; they rose for every FOMC meeting in the next year. That said, we continue to believe that once the Fed does initiate liftoff, the trajectory will be anything but straight up. As we have stressed, what matters more than the start date is the speed and duration thereafter. We would take Fed Chair Janet Yellen’s word that this is setting up to be a shallow path of rates hikes.

Why does slope matter?

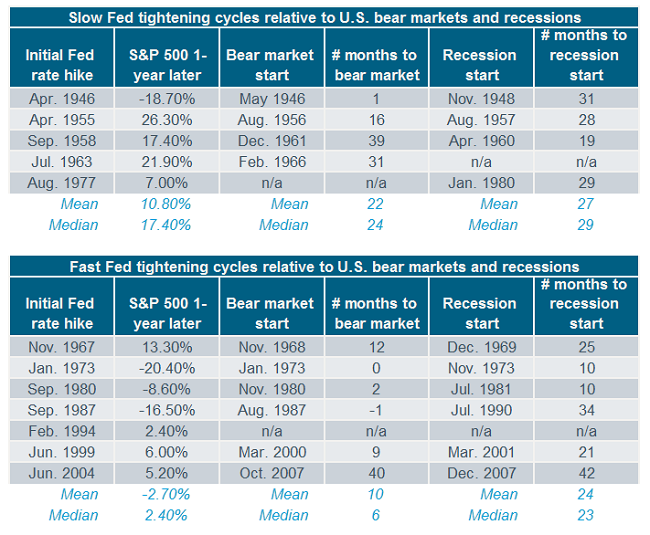

The data in the table below looks at every rate hike cycle since World War II, but breaks them into two categories—those when the Fed was moving slowly (taking breaks from hiking along the way), and those when the Fed was moving more quickly (hiking at most or all consecutive FOMC meetings). Whether you look at mean or median data, you can see that slow cycles—we haven’t had one of those since the 1970s—have led to better stock market returns a year out. You can also see that bear markets and/or recessions were typically further out when the Fed was moving slowly. This makes sense.

Slow Fed tightening cycles relative to U.S. bear markets and recessions

Source: Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2015© Ned Davis Research, Inc. All rights reserved.).

In the meantime though, markets will continue to obsess over the December meeting and the economic data between now and then—particularly this coming Friday’s employment report. That is the first of two employment reports between now and the December FOMC meeting. If they run hotter than expectations—especially if there is a pick-up in wage growth (which could then translate to a pickup in inflation)—we would expect the likelihood of a December hike to rise.

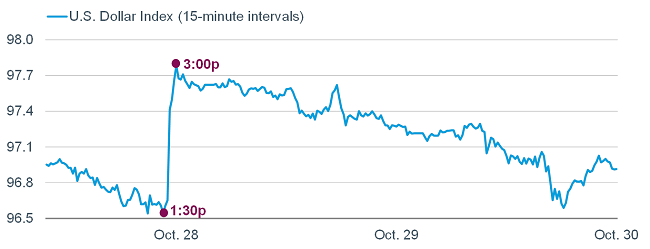

Dollar a factor in "Fed policy loop"

In addition to rate hike expectations rising for December, upon the release of the FOMC statement in October, the US dollar surged as well, as you can see in the chart below. Given the subsequent reversal, it’s possible the initial move was an overreaction.

Dollar’s Quick Surge Fades

Source: FactSet

We do believe the dollar remains in a bull market, but it’s important to note that the dollar has historically had most of its rate hike cycle-related strength leading into the initial hike, not thereafter. After all three of the prior cycles’ initial hikes (1994, 1999 and 2004) the dollar’s ascent hit its apex in short order before trending lower over the subsequent months.

In addition, since 2000 the dollar has been less influenced by Fed policy and other domestic trends, and more influenced by global growth trends. If, as Schwab’s Jeff Kleintop has been noting, global growth is picking up, it would put offsetting downward pressure on the dollar, even if the Fed begins raising rates.

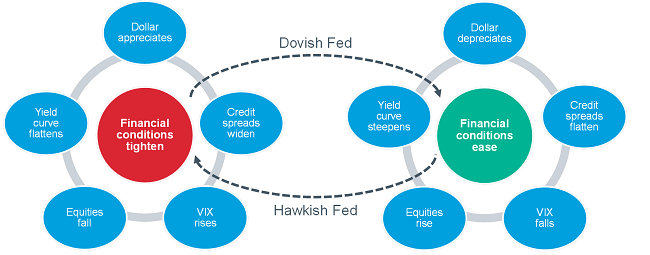

Perhaps that helps alleviate the loop the Fed’s been in for some time, as see in the visual below (my visual representation of an analysis done by BCA Research).

The Fed Policy Loop

Source: BCA Research Inc., Charles Schwab.

The loop we’ve been witnessing starts when Fed rhetoric becomes more hawkish, which tightens financial conditions: the dollar rallies, credit spreads widen, volatility rises, equities pull back and the yield curve flattens. These tighter conditions lead to a more dovish Fed and looser financial conditions: the dollar pulls back, credit spreads narrow, volatility eases, equities rally and the yield curve steepens.

Lately, we have been residing in the right side of this loop, but the October Fed statement may have moved the needle a bit more toward the hawkish side. The hope is that we can exit the “Groundhog Day” scenario (thank you ISI Group) which has resulted from this loop. A Fed that finally rips off the bandaid could do the trick.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

(1115-6779)