Devil Inside, Redux: Another Look at the Variety of U.S. Market Valuation Metrics

Key Points

- Inflation and interest rate-based valuation measurements suggest the market remains inexpensive.

- But more traditional P/E ratios and other unique models suggest the market is expensive.

- Ultimately, what matters more for the market is the direction, not the level, of valuations.

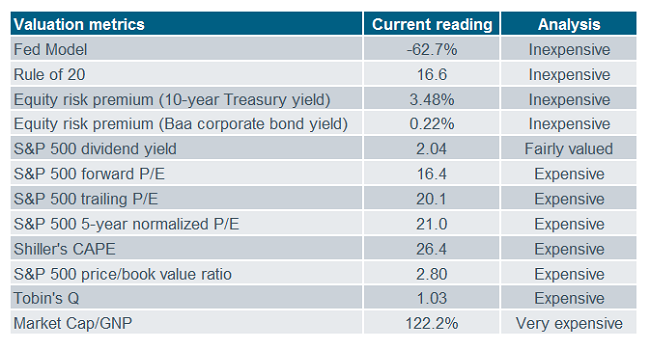

I’ve written many times about equity market valuation being both in the eye of the beholder and a function of the chosen indicator. Even the most common valuation metric—the price/earnings (P/E) ratio—has many derivations. The table in this report is a summary of most of the common (and somewhat less common) valuation metrics, and a subjective assessment of whether they are sending an inexpensive or expensive message about the stock market presently.

The punchline is that valuation is presently a very mixed bag—with a few indicators saying the market is quite cheap, while others saying it’s quite expensive. This muddied picture continues to be one reason for our continued “neutral” rating on U.S. stocks (meaning investors should remain at their long-term equity allocations).

The five valuation measurements falling into the inexpensive or fairly valued category are:

Rule of 20: Stocks are considered fairly valued when the sum of the S&P 500 forward P/E ratio and the year-over-year change in the consumer price index (CPI) is equal to 20 (or inexpensive when it’s below 20).

Fed Model: This model compares the S&P 500’s earnings yield (which is the inverse of the P/E—or E/P) to the yield on long-term U.S. government bonds. Negative readings suggest favoring stocks over bonds.

Equity Risk Premiums: These subtract either the forward 10-year U.S. Treasury bond yield or the forward Baa corporate bond yield from the forward S&P 500’s earnings yield (E/P). Positive readings suggest stocks are undervalued relative to bonds.

Dividend Yield: Compares the current dividend yield on the S&P 500 with both historic averages and the 10-year U.S. Treasury yield. At near-equivalent yields, the market is seen as fairly valued.

The seven valuation measurements falling into the expensive category are:

Forward P/E: Probably the most common measurement, it divides the current S&P 500 price by 12-month forward expected operating earnings. It’s presently slightly above its ~20-year median of 15.9.

Trailing P/E: Also a common measurement, it divides the current S&P 500 price by 12-month trailing operating earnings. It’s presently comfortably above its ~25-year median of 17.8.

5-Year Normalized P/E: This model uses four years of historic earnings, two quarters of forward earnings, and takes the midpoint between reported and operating earnings (it’s a take on Shiller’s CAPE, but with a shorter time span, and with an adjusted earnings calculation). It’s presently comfortably above its ~70-year median of 18.1.

Shiller’s Cyclically-Adjusted P/E (CAPE): This model uses an inflation-adjusted price for the S&P 500 and divides by reported earnings over the prior 10 years. It’s presently comfortably above its ~135-year median of 16.

Price/book: Divides the current S&P 500 price by the book value of its components. It’s presently slightly above its ~38-year norm of 2.4.

Tobin’s Q: Developed by Nobel Laureate James Tobin, it’s a fairly simple concept, but laborious to calculate (calculations are done by the U.S. government and the ratio’s readings are provided by the Fed). It’s often called the Q Ratio and is the total price of the U.S. stock market divided by the replacement cost of all its companies. A high Q (greater than .85) implies overvaluation.

Market Cap/GNP: Considered Warren Buffett’s “favorite valuation indicator,” the model is the ratio of total U.S. market capitalization to gross national product (GNP). It’s presently well above its ~65-year mean of 69%.

Source: Cornerstone Macro, FactSet, The Leuthold Group, Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2015© Ned Davis Research, Inc. All rights reserved.), Standard and Poor’s, as of November 27, 2015. CAPE data and methodology courtesy of Professor Robert J. Shiller (http://www.econ.yale.edu/~shiller/data.htm).

Caveats

Three of the valuation metrics above—one of which falls into the inexpensive category and two of which fall into the expensive category—deserve mention for important caveats to consider: Fed Model, Shiller’s CAPE and Market Cap/GNP.

Fed Model: Cornerstone Macro highlighted the problem with the Fed Model in a recent report on valuation. “For much of history, before the early 2000s, bond yields and earnings yields were within close range; making such a comparison an important branch in the asset-allocation decision tree. Since 2002, the gap has widened to historic highs, and has exposed the shortfalls of the model.”

“In mid-2002, the yield on the 10-year government bond fell below the yield on the S&P 500. It has never crossed back since then. Thus, the Fed Model has told asset allocators for 12 straight years now to prefer stocks over bonds. That’s quite a long time to buy and hold stocks … especially while bonds have rallied so much over that time. This is one where you sometimes should fight the Fed [model].”

Shiller’s CAPE: In a version of this valuation analysis I published last May, I dissected the CAPE and the caveats which are crucial to consider. I’ve linked to that report here: Devil Inside: Dissecting the Most Popular Valuation Metrics

Market Cap/GNP: As for Warren Buffett’s favorite valuation indicator, some caveats are also worth mentioning. As noted by Cornerstone, “this metric has huge weaknesses, such as not recognizing structural changes in a country’s financial system, productivity, tax policy, demographics, etc. … the list is long on why this metric isn’t useful for comparison over time.”

In sum

You could probably find two market analysts on opposite ends of the spectrum from bullish to bearish; and they’d probably cite valuation as one of their reasons. It’s confusing for investors, who would probably love a simple and foolproof approach to valuing the stock market. There are myriad factors which affect valuation levels and their direction; including economic growth, inflation, Fed policy and even geopolitics.

Finally, and importantly, what’s perhaps more important than the level of valuations, is the direction they’re heading, regardless of the metric being used. In general, valuations have been expanding across most metrics and in the near-term, the conditions remain ripe for that trend to continue; at least until earnings can “catch back up” to valuations.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

(1115-7199)