Key Points

- Worst start to a year in history

- Barring recession, pain should be limited to correction, not bear market

- “Smart money” getting more enthusiastic

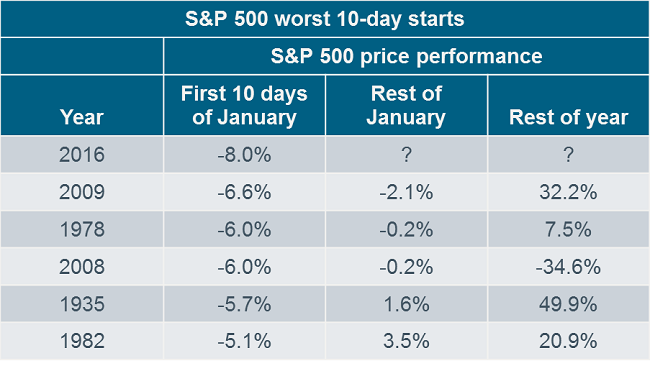

The S&P 500 is down 8% since the year began, the worst two-week start to a year ever. There have only been five other years since 1928 when the index fell by more than 5% in the first 10 trading days of the year. As shown in the B.I.G. table below, looking back at the five worst yearly starts, the returns for the rest of January were mixed, while the rest of year returns were more positive (dramatically so in three cases). The only dud was during the financial crisis in 2008.

Source: Bespoke Investment Group (B.I.G.).

The correction has similarities to last August’s—a swift price decline for a market that had recently been near multi-year highs. SentimenTrader (ST) notes it’s quite rare to see this kind of severity relatively soon after trading near a three-year high—and the fact that we’re seeing another episode so close to last August’s is also rare. Looking at history, there was a binary outcome after such periods: the market tended to worsen looking ahead if a recession had already begun or was imminent. But if there was no recession, the market did decidedly better.

Recession?

Every predictive recession model I have studied still suggests a low risk of recession. In fact, if we are in one or heading toward one, it would be the first time in history the leading indicators did not roll over and provide ample warning.

We are in a manufacturing recession, but at this point, the much larger services segment of the economy is showing sustained growth. Historically, if the annual average of industrial production is down for an entire year, weakness spread to the broader economy. We have yet to see that kind of weakness, but it’s on our watch list.

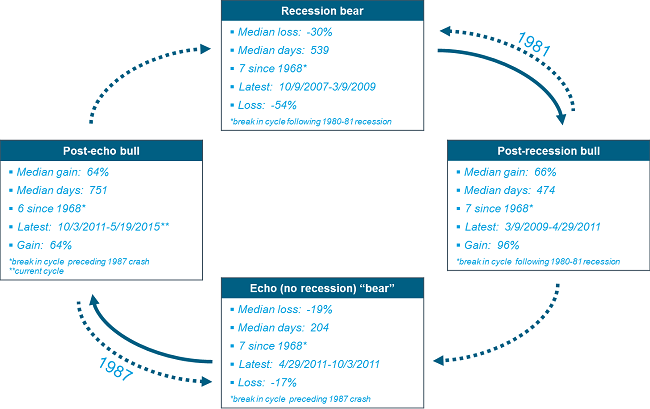

The U.S. stock market has moved in fairly distinct cycles. Looking at the past seven full market cycles, the pattern is typically for the recession bear market to be followed by the post-recession bull market, which typically leads to an “echo bear” market (a severe correction), before finishing with the “echo bull” market. Noted in each box are the dates associated with the most recent market cycle.

Source: Ned Davis Research (NDR), Inc. Further distribution prohibited without prior permission. Copyright 2016© Ned Davis Research, Inc. All rights reserved. Results based on the Dow Jones Industrial Average. Recession bear=cyclical bear market overlapped by a recession. Bear markets classified as recession bears when National Bureau of Economic Research (NBER) declares a recession, which can be several months after the bear market has started. Until then, all bear markets classified as Echo Bears. Post recession bull=cyclical bull immediately following a recession bear. Echo bear=cyclical bear market during a non-recessionary period. Post echo bull=cyclical bull immediately following an echo bear. Cyclical bull market=30% rise in DJIA after 50 calendar days or 13% rise after 155 calendar days. Cyclical bear market=30% drop in DJIA after 50 calendar days or 13% decline after 145 calendar days. **Corresponding end date is date of high/low from trough or peak. Dotted lines indicate occasional occurrences.

We don’t always move in a perfect clockwise direction. For instance, as seen above, in 1981, we quickly moved from the post-recession bull back to a recession bear courtesy of the double-dip recession in the early 1980s. And in 1987, we suffered a quick non-recession bear in the midst of the echo bull courtesy of the crash.

Since all-time highs were reached last May (and haven’t been exceeded since then), inquiring minds want to know where we go from here. Are we moving clockwise and heading into the next recession bear market? Or, if the bull market doesn’t resume, are we moving counter-clockwise toward an echo (non-recession) “bear” market? If we are out of the echo bull market phase, I think we’re more likely in the latter scenario.

Oil effect

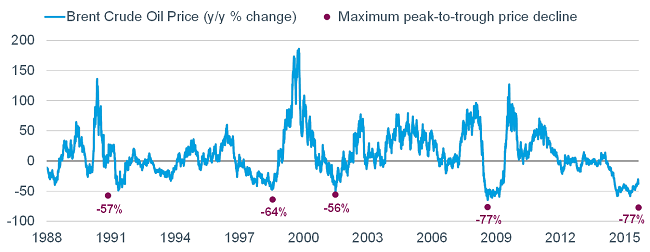

If a recession is coming, it would also be the first time in history it was preceded by a crash in oil prices—more often than not, it’s a surge in oil prices which helps trigger a recession. As a consumption-oriented economy, US growth is ostensibly helped by lower energy prices. The rub of course, is that there are segments of the economy which are severely damaged; i.e., the energy and basic materials sectors. What we’re facing now is an environment where the headwinds associated with weak oil have a higher miles-per-hour than the tailwinds, which have yet to pick up.

Oil prices likely have to stabilize for the market to do the same. I won’t attempt to forecast when/where that may be, but the chart below does show we have reached historical extremes—not only in year-over-year terms for global oil prices, but also maximum peak-to-trough declines.

Source: FactSet, as of January 14, 2015.

Fed’s dots plot conundrum

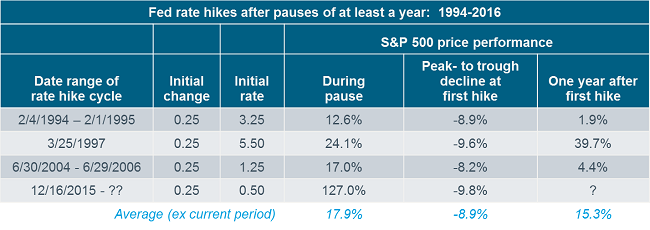

But it’s not just oil, it’s also continued ongoing uncertainty around Federal Reserve policy. We eliminated last year’s uncertainty around the “when” of an initial rate hikes, but not the “how much” in terms of the trajectory of rate hikes from here. The 10.9% drop in the S&P 500 since the November 2015 high is not far off the mark of what we’ve seen historically in the immediate aftermath of initial rate hikes.

Source: Bespoke Investment Group (B.I.G.).

For the market to stabilize, the Fed may have to talk down its forecasts associated with the “dots plot,” which shows that it still assumes four rate hikes this year; while the market assumes only two. We continue to think the market will be closer to the truth.

Sentiment hitting extremes

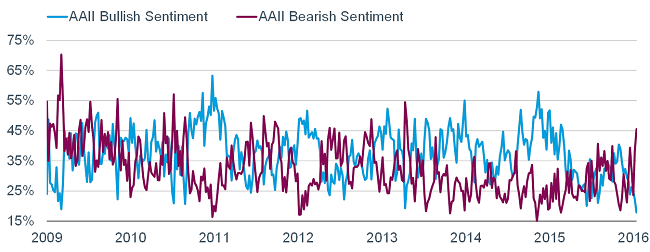

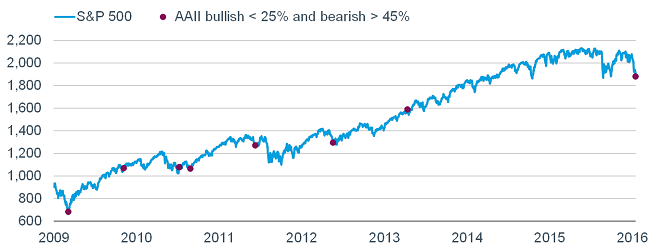

Finally, we can look at sentiment to see if we’ve reached the extremes that have historically marked near-term bottoms (or bottoming phases). The spike in bearishness and commensurate plunge in bullishness as measured by the American Association of Individual Investors (AAII) has hit an extreme historically associated with decent buying opportunities for stocks.

As you can see in the charts below, there have been eight periods so far in the current bull market when bearish sentiment spiked to more than 45% at the same time bullishness plunged to below 25%. They are marked on the same spot on the S&P 500 chart at the bottom and each time, it marked a short-term low for stocks (although in late-2011 there was more pain to come).

Source: FactSet, as of January 15, 2016. The AAII (American Association of Individual Investors) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market short term.

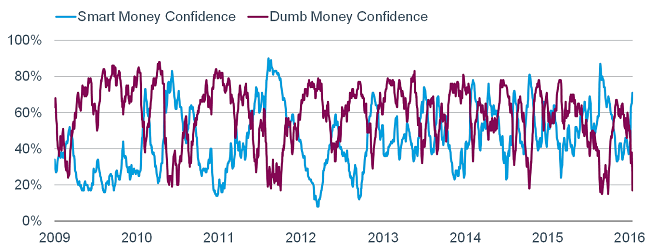

We are seeing a similar—though not as extreme—dispersion in the spread between ST’s “smart money” and “dumb money” confidence (remember, those are ST’s labels, not ours). Although not quite to the extremes seen in 2011 or last summer in 2015, “smart money” confidence has jumped sharply over the past week or so, while “dumb money” confidence has plunged to depths in keeping with extreme lows seen in the current bull market. As a reminder, the “dumb money” is the contrarian indicator, while the “smart money” is the non-contrarian indicator (i.e., you want to follow what they’re doing at extremes).

Source: SentimenTrader as of January 15, 2016. SentimenTrader’s Smart Money Confidence and Dumb Money Confidence Indexes are a unique innovation used to see what the “good” market timers are doing with their money compared to what the “bad” market timers are doing. When the Smart Money Confidence Index is at 100%, it means that those most correct on market direction are 100% confident of a rising market. When it is at 0%, it means good market timers are 0% confident in a rally. The Dumb Money Confidence Index works in the opposite manner.

In sum

The reality is we don’t know where the market goes from here. But although we can’t control the direction of the market, we can control what we do about it. We are long known for espousing that panic is not an investment strategy, and that a disciplined approach to asset allocation- involving diversification and periodic rebalancing—are the keys to long-term success.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

(0116-0362)