Key Points

- Leading indicators weakened in August, but are not yet flashing a recession warning.

- Recession models show rising, but still low risk of a coming contraction in economic activity.

- Economic recoveries don’t tend to die of old age; they die of excess…of which there’s little in this recovery.

I keep a close eye on every variety of leading economic indicators—of which the stock market is one. Last week’s release of the most-widely followed set of leading indicators—the Conference Board’s Index of Leading Economic Indicators (CB’s LEI)—showed an unexpected decline of 0.2%. Each month I put together a “dashboard” of these leading indicators in order to see any flashpoints. The LEI has ten sub-indexes and it’s important to judge each not just on their level, but their trend and rate of change. This is because when it comes to the relationship between the economy and the stock market, it’s typically the case that better or worse matters more than good or bad. In other words, inflection points in the data are often more telling than the level of the data point.

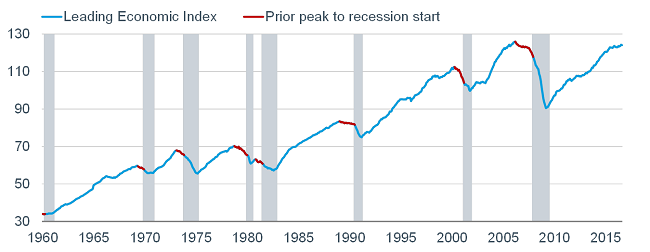

Below is a long-term chart of the LEI. As you can see, the peaks occurred well in advance of the onsets of recessions—on average by more than 12 months. And in the case of the three most recent recessions, the LEI had “round-tripped” (taken out its prior high) at least four years prior to the subsequent recessions. So, if a recession is imminent today, it would be unprecedented for the LEI not to give sufficient warning.

Source: FactSet, The Conference Board, as of August 31, 2016.

As you can see above, the LEI presently remains below its prior (2006) high and has yet to signal a definitive turn for the worse. Yes, August’s reading was negative and worse than expected, but as noted, there are usually months and months of deterioration before recessions ensue. August is also a month notoriously prone to economic data revisions—especially jobs-related data. So, the net is it’s too soon to declare victory for the economic bears.

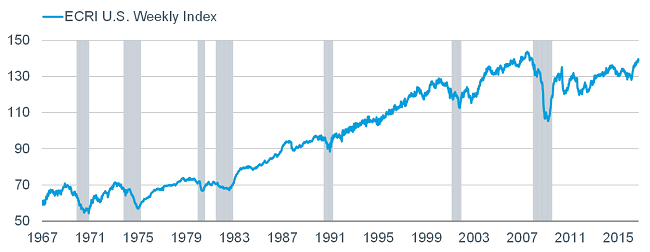

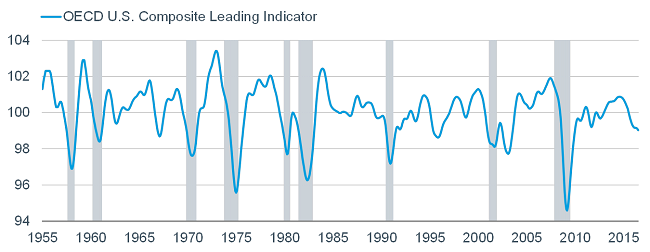

Before I get to the level and trend analysis of the LEI’s components, I also want to highlight two additional leading indexes. The first chart below shows the Economic Cycle Research Institute’s Weekly Leading Index (ECRI’s WLI), which is also not flashing a warning about a coming recession. The second chart shows the OECD U.S. Composite Leading Indicator, which does show an alarming decline recently. However, do note there are three precedents—in the mid-1960s, mid-1980s and mid-1990s—when the index dropped significantly, but they turned out to be mid-cycle slowdowns, not recessions.

Source: ECRI (Economic Cycle Research Institute), as of September 16, 2016.

Source: FactSet, OECD (Organization for Economic Coordination and Development), as of July 31, 2016.

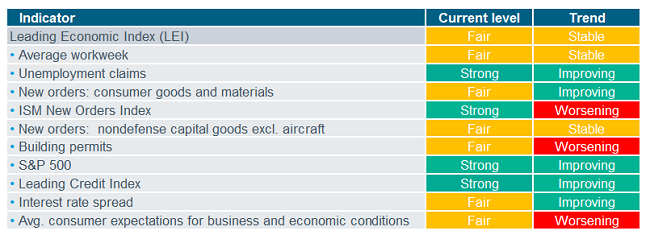

One of the reasons for the popularity of the CB’s LEI is that the CB is transparent with its underlying data, and the sub-indexes are easy to track. There are ten sub-indexes within the LEI and below is the aforementioned dashboard showing a color-coded review of the individual indicators.

Source: Charles Schwab, The Conference Board, as of August 31, 2016.

There is unquestionably a bit more red on the page than there was last month, with ISM new orders and consumer confidence particularly bearing watching. But I don’t yet view this as particularly alarming.

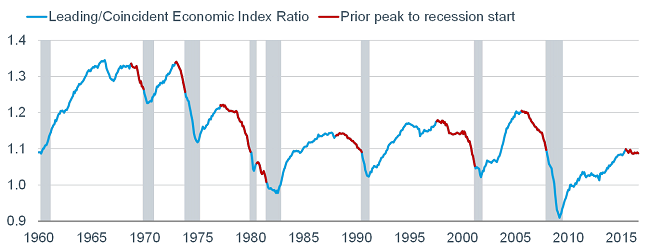

The CB also releases its Coincident Economic Index (CEI) every month, which includes data that tends to move coincident with economic activity. In fact, its four components—payrolls, personal income, industrial production, and real manufacturing and trade sales—are the indicators used to date recessions by the National Bureau of Economic Research (NBER). The ratio between the CEI and the LEI (LEI/CEI) has also historically been a good leading indicator of recessions. Before prior recessions, the ratio has peaked well ahead of time; and has tended to roll over significantly ahead of recessions, as you can see in the chart below.

Source: Bespoke Investment Group (BIG), FactSet, The Conference Board, as of August 31, 2016.

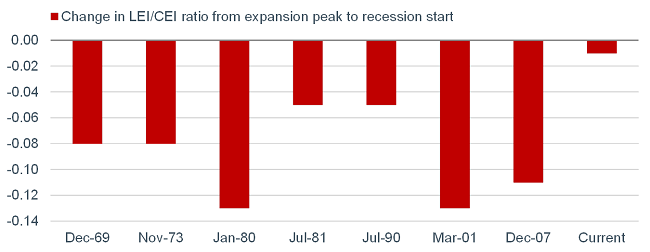

The chart below is courtesy of Bespoke Investment Group (BIG) and shows the decline in the ratio from the peak of each expansion to the start of the following recession. In the seven prior recessions since 1960, the average decline of the ratio was 0.091 (median 0.083), and the minimum decline was 0.054. As you can see, the current decline is still a fraction of those prior declines.

Source: Bespoke Investment Group (BIG), FactSet, The Conference Board, as of August 31, 2016.

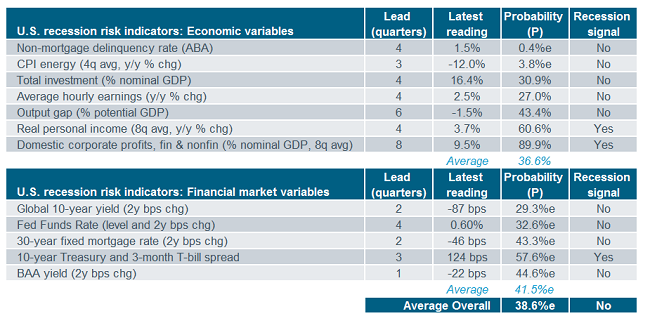

Finally, there are two recession models on which I keep a close eye. The first is courtesy of Cornerstone Macro and the table below is a detailed look at the model’s sub-indicators and whether they’re individually (or collectively) signaling recessions. Presently there are three indicators flashing warnings—personal income, corporate profits and the Treasury yield spread. The overall probability of a recession based on this model has risen to just over 38%.

Source: Cornerstone Macro. Subjective recession signal per Cornerstone Macro thru 2Q17. ABA=American Bankers Association. Bps=basis points.

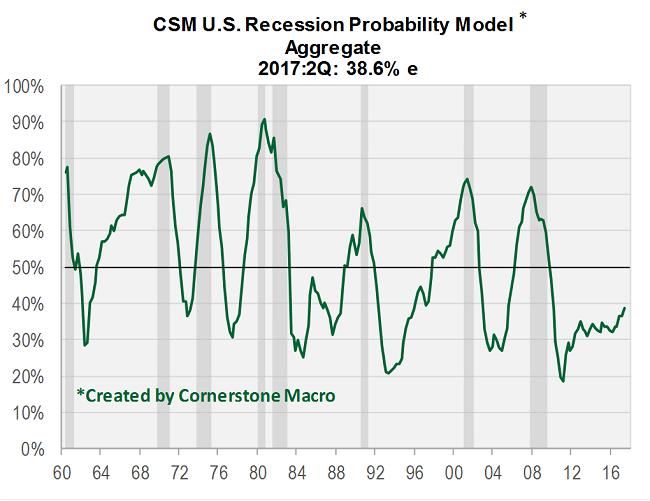

I do think these indicators bear watching, but do note that it’s typically readings comfortably north of 50% that have signaled coming recessions historically, as you can see from this long look back at the history of Cornerstone’s modeling framework.

Source: CornerstoneMacro.

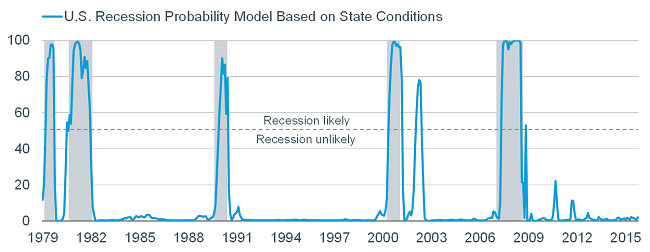

The second recession model is courtesy of Ned Davis Research and is based on state-level coincident indicators. These indicators can be useful in determining where the economy is in the national business cycle. So far, this model says no recession, but underlying conditions are deteriorating and bear watching.

Source: Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2016 © Ned Davis Research, Inc. All rights reserved.), as of August 31, 2016.

Old age curse?

Yes, this has been a historically-long recovery of over seven years, or 86 months—which compares to the post-war average of 58 months. But expansions don’t typically die of old age, they die of excess. The excess is often in the form of inflation, monetary policy, capital spending, capacity utilization, debt, etc. If there is one benefit to this recovery having been of the anemic variety is that it’s kept this excess in check.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

(0916-MDTP)

© Charles Schwab