Key Points

- Soft economic data has been on a tear; will the hard data catch up?

- After a "typical" weak first quarter, economic growth should accelerate.

- Based on history, soft data is likely to retreat, while hard data is likely to accelerate.

Much ink has been spilled by Wall Street analysts, the media, and yours truly, about the historically-wide spread between the so-called "soft" and "hard" economic data. Before getting to my latest thoughts on the subject, some definitions are in order. Soft data is generally survey-based readings, including many of the most widely-followed confidence indicators—incorporating both consumer and business measures of confidence, as well as purchasing managers' surveys (PMIs). Think of it as the qualitative data. On the other hand, hard data is the quantitative data—actual measures of economic activity.

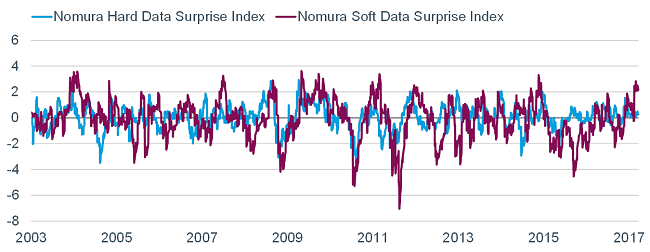

Soft data surging

The spread between the soft and hard data (using any number of indexes created to track this) hit a recent high; with the soft data reflecting a post-election surge in optimism. You can see the relative strength of the soft data vs. the hard data in the chart below.

Source: Bloomberg, as of March 22, 2017. Indices track data surprises (actual – economist expectations) through time. Surprises are standardized, and each indicator has an equal weight.

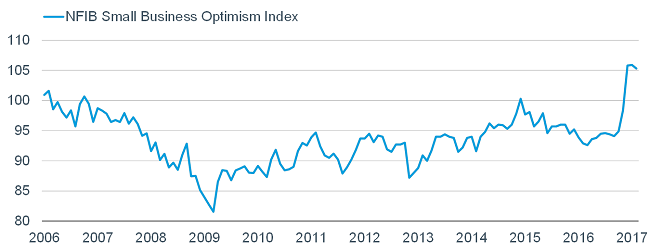

In particular, the spike in soft data was aided by a parabolic move up in the small business optimism index published by the National Federation of Independent Business (NFIB), as you can see in the chart below. All common measures of consumer confidence and sentiment have surged as well.

Source: FactSet, as of February 28, 2017.

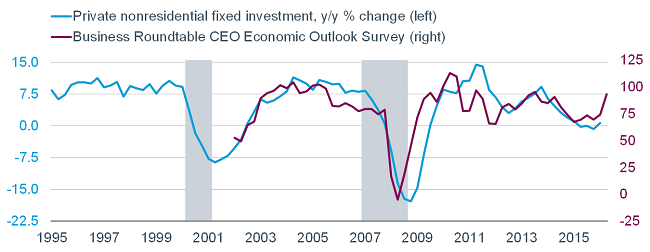

Another measure of soft data which has accelerated sharply is the Business Roundtable CEO Survey, seen in the blue line below. As you can see, fixed investment tends to be highly correlated to CEO optimism, so this is one suggestion of improving hard data to come. According to Strategas Research Partners, CEO confidence has led capital spending by one quarter; so if animal spirits are going to show up in the U.S. economy, this is a key metric to watch.

Source: FactSet, Strategas Research Partners. Fixed investment as of December 31, 2016. CEO Outlook Survey as of March 27, 2017. Gray-shaded areas indicate periods of recession.

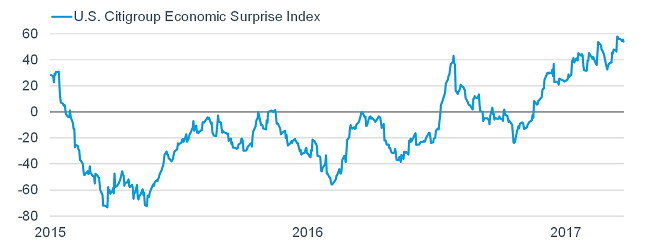

The strength in the soft data, as well as some in the hard data, has helped push up the Citi U.S. Economic Surprise Index, which measures how data is coming in relative to expectations (see chart below).

Source: FactSet, as of March 24, 2017.

It's been our contention that the inevitable narrowing of the spread between the soft and hard data would likely be in both directions; i.e., confidence measures would likely ease, while the hard data would play at least a little catch up. According to Bespoke Investment Group (BIG), when soft data outperforms, hard data usually plays catch up in the following three and six months; while soft data almost always declines. With regards to the stock market, average and median returns have been skewed to the positive over these time frames as well.

Hard data less robust

Higher-frequency financial and economic data has been fairly strong to start the year; keeping in mind the likelihood of yet another weak first quarter growth reading. This has been a consistent pattern over the past two decades, with first quarter real gross domestic product (GDP) lagging the other three quarters by about 100 basis points.

Durable goods orders were strong in February, as were core capital goods shipments. Within the industrial production report, manufacturing, mining and ex-auto manufacturing were all strong. Housing data has been mixed-to-strong and the housing market index (HMI) surged in early March. And strength abroad has been notable—important for U.S. multinationals and the export side of the U.S. economy.

There are longer-term pressures weighing on the hard data; most notably, debt In addition, inflation is on the rise, which puts downward pressure on real incomes. Finally, with anti-immigration policies coming, it becomes more difficult to generate the kind of labor force growth needed to boost economic growth. Add to that weak productivity, and it’s hard to get too enthusiastic for a major lift in economic growth any time soon. So, hard data is likely to play a little catch up, but curb your enthusiasm for a more meaningful acceleration.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

© Charles Schwab

Read more commentaries by Charles Schwab