Key Points

- Economic surprises have faltered to the neutral level

- Hard data has been stubbornly weak relative to soft data

- But leading indicators are not flashing any meaningful warning about growth

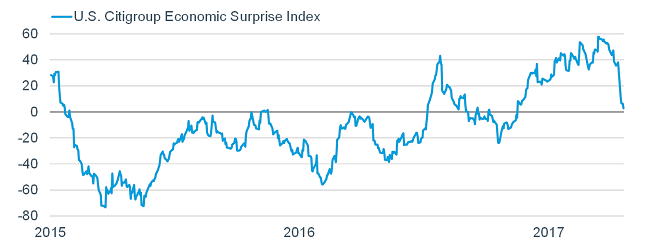

As I've often noted when it comes to the relationship between economic data and the stock market, "better or worse tends to matter more than good or bad." In other words, stocks tend to key off rate of change more than level when it comes to economic indicators. That is why the Citi Economic Surprise Index (CESI) is not only so widely followed, it's highly correlated to the stock market's performance.

Surprise!

As seen below, the CESI—in this case for the United States—measures how economic data is coming in relative to expectations. After a notable surge from mid-October 2016 to the recent high, the index has fallen back toward the zero marker. This perhaps explains more than anything the choppier action by U.S. stocks in March and April. As grim as this may appear, it is more likely a normal reversion to the mean, as readings as high as seen recently don't tend to be sustainable—especially when the expectations bar gets high, as had been the case.

Source: FactSet, as of April 21, 2017.

Soft hard data

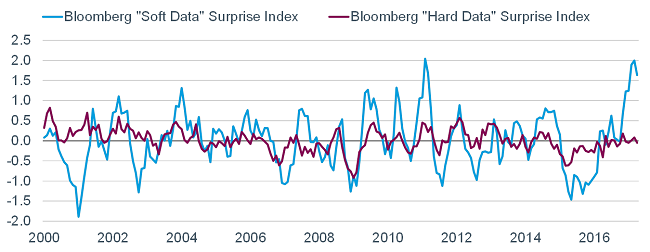

Part of the reason the expectations bar got elevated was due to the parabolic surge in so-called "soft" data (survey/confidence-based); about which I've written in detail recently. The chart below looks as the relationship between soft and hard economic surprises. Clearly, the hard data continues to be disappointing relative to the soft data, although even the soft data retreated a touch recently.

Source: Bloomberg, as of April 21, 2017. Soft data: business and consumer surveys. Hard data: housing, industrial, labor, household and retail data.

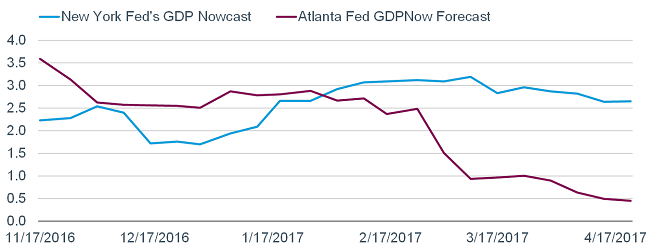

This soft vs. hard divide has also manifested itself in two popular—and divergent—forecasts for first quarter U.S. real gross domestic product (GDP). As seen below, the Atlanta Fed’s GDPNow model has sunk to 0.5%; while the NY Fed's Nowcast remains significantly higher at 2.6%. One simple explanation is that the former has a greater emphasis on hard data, while the latter incorporates more soft data.

Source: Bloomberg, as of April 21, 2017. Forecasts for 2017:Q1 GDP growth.

Recent culprits of the drop in the CESI as well as the sluggish movement in the hard data include:

- March's Philadelphia Fed manufacturing survey was weaker-than-expected, although still strong.

- Last week's initial unemployment claims ticked up, although they remain strong.

- Details within the consensus-matching March industrial production report were weaker-than-expected.

- March's housing starts were below expectations, but were preceded by weather-related exaggerated strength.

- Early April's housing market index (HMI) came in below consensus, but was preceded by an unsustainable surge.

- March's retail sales disappointed, but the details not as weak as the headline reading.

Weak Q1- what else is new?

Notice the more positive caveats in each of the bullets above. Yes, data has come in a bit weaker than expectations; and as noted above, the Atlanta Fed's GDPNow model is forecasting an anemic first quarter. However, weak first quarters have become a consistent pattern. Over the past 10 years, the average for all first quarters has been exactly zero real growth; while the average for the other three quarters has been 1.8%. At the same time, forward-looking data remains quite healthy.

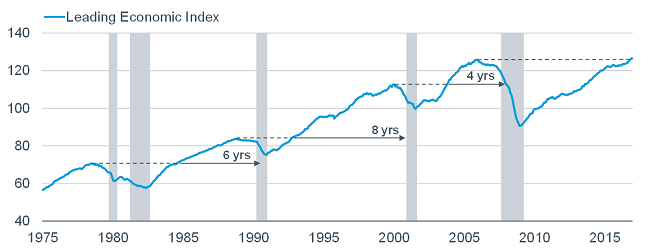

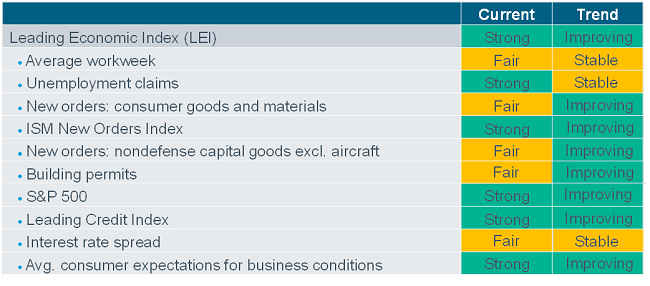

But leading indicators look good

I keep a close eye on leading economic indicators as they say a lot more about the economy prospectively than backward-looking measures like GDP. The chart and table below are part of a package I put together every month for Schwab's operating committee as it serves as a quick snapshot of how the economy is faring looking ahead. There are several popular indexes of leading indicators; with the most popular being the one compiled by The Conference Board:

"The composite economic indexes are the key elements in an analytic system designed to signal peaks and troughs in the business cycle. The leading economic index is essentially a composite average of 10 individual leading indicators. They are constructed to summarize and reveal common turning point patterns in economic data in a clearer and more convincing manner than any individual component—primarily because they smooth out some of the volatility of individual components."

First, an explanation of the markers on the chart is in order. The line is simply the level of the LEI. The gray bars are official recessions (notice how the LEI has never failed to roll over in advance of recessions; nor failed to bottom and turn high in advance of recessions' ends). The dotted lines represent what I think of as "round trips" in that they measure the span from the prior cycle's LEI high to the point in the post-recession expansion when the LEI took out that prior high. The solid lines represent the span from the new LEI high to the subsequent recession. After the three most recent round trips were complete, the next recession was between four and eight years away. Although I think it's a stretch to think the next recession is still years away; do notice the LEI just last month finally took out its prior 2006 high.

Source: FactSet, The Conference Board, as of March 31, 2017. ISM=Institute for Supply Management.

In the table above, you can see the 10 component sub-indexes of the LEI and courtesy of the green/yellow/red color-coding, you can see that there are presently no red-colored boxes (meaning no warning flashes). We are likely just experiencing yet another "soft patch" in an ongoing expansion; so for now, I am seeing the glass as half full.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

© Charles Schwab

Read more commentaries by Charles Schwab