Key Points

- In typical fashion, the financial media may have gone a little overboard with its breathless reporting on the recent "tech wreck."

- For all the hype around "FAANG" stocks, none of them were even in S&P 500’s top-30 at the recent peak.

- Tech companies' fundamentals and valuations look vastly dissimilar to the 2000 era.

Tech "wreck?" That's a bit of a stretch in my opinion; but the financial media loves a good headline. The major ascent—and recent pullback—of the so-called FAANG stocks (Facebook, Apple, Amazon, Netflix and Google) has generated much attention; and lately, the subject of technology stocks more broadly has dominated Q&A sessions at events at which I've spoken. Let's start with the FAANG stocks (which sometimes have Microsoft lumped in with them as well). For all the sound and fury around that group of stocks, it may surprise many that none of them were even in the top 30 best performers within the S&P 500 at the recent market peak. Also, do note that neither Amazon nor Netflix are even in the tech sector—they're in the consumer discretionary sector.

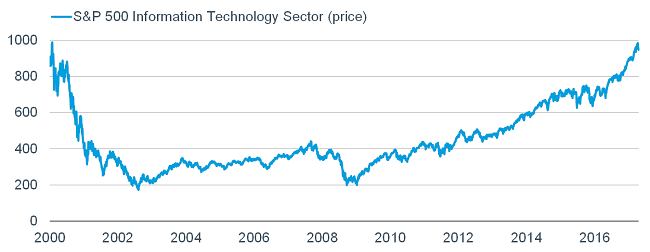

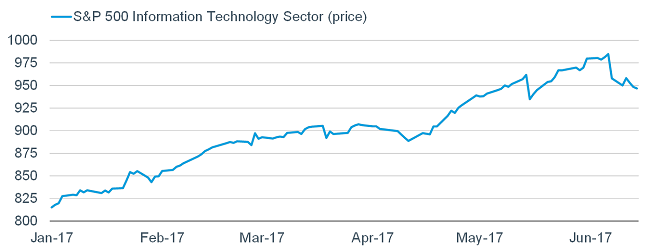

Nonetheless, parallels are being drawn between tech today and tech circa 2000. I think the comparison is a stretch, across many measures of valuation—not to mention magnitude of decline. From its peak on June 8 the S&P 500 tech sector is down about 4% as of Friday's close. The charts below cover the period since tech's peak in March 2000 and year-to-date, respectively.

Source: FactSet, as of June 16, 2017.

The Leuthold Group recently did a micro-level study of tech sector valuations across the cap spectrum, and as music to my ears, they titled it What a Long Strange Trip It’s Been. They noted that the S&P tech sector is "just a few percentage points short of a five-bagger off the 2009 bear market low. That's spectacular performance, but also one of several recent developments that highlight not so much the persistence of the current bull market, but rather, the insanity of the one that ended more than 17 years ago. Specifically, the nearly 400% cyclical gain in the [tech sector] has merely restored it to its March 27, 2000 peak!"

The S&P 500's tech sector’s cumulative return since March 2000 is now flat; but the S&P 400's midcap tech sector's cumulative return is 65% and the S&P 600's small cap tech sector’s cumulative return is 75%. If investors had purchased and held the midcap and small cap tech stocks at the top in 2000 they would have outperformed the S&P 500, reinforcing the power of time.

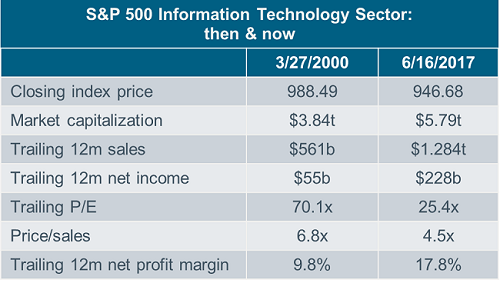

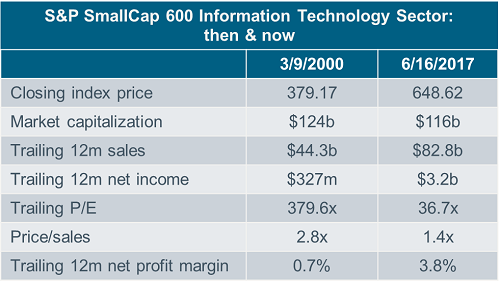

Take a look at the table below, which shows that the 69 companies in the S&P 500 tech sector have generated nearly 130% more revenue in the past 12 months than in 2000; while net income has more than quadrupled courtesy of a huge increase in net profit margins. More importantly, valuations are nowhere near the stratospheric level of 2000.

Source: The Leuthold Group, as of June 16, 2017.

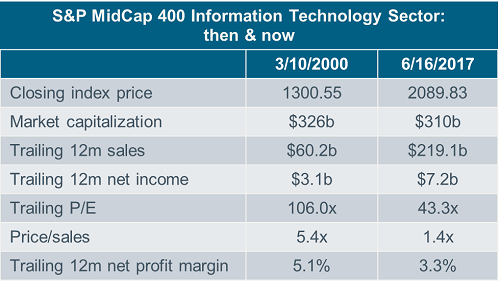

You can see the same analysis in the tables below, which look at the comparisons for the midcap and small cap S&P tech sectors, respectively.

Source: The Leuthold Group, as of June 16, 2017.

We think the latest pullback in tech is more likely to represent a pause that refreshes some excess optimistic sentiment than it is the start of something nastier. My colleague Brad Sorensen, Schwab's Director of Market and Sector Analysis, has highlighted that the sector has had an incredible run and remains the leading sector in the year-to-date performance derby. Forward-looking earnings expectations are for 12% growth in 2017 and an additional 11% in 2018; while debt is low, dividend payouts are rising and buybacks persist. And with a tight labor market, companies are looking toward technology to boost productivity. Evercore ISI survey data shows 53% of companies planning to increase tech spending; up from 38% last November.

Today's tech companies look nothing like many of their 2000 counterparts, some of which were valued on silly things like "eyeballs" given they had no earnings, and little prospect of every having an earnings stream. I sympathize with the muscle memory of both the bursting of the tech bubble in 2000, and the real estate bubble in 2007; and many investors have vowed not to get caught up in the "hype" again. We are maintaining our outperform rating on the tech sector, but as with any fast-growing segment of a portfolio’s holdings, also remind investors of the power of diversification and periodic rebalancing.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

© Charles Schwab

Read more commentaries by Charles Schwab