Key Points

- Both active and passive management styles have a home in investors' portfolios.

- Passive continues to outperform active, but we may have seen the inflection point.

- Plunging correlations and wider sector dispersion both bode well for active styles.

I'm often asked how I invest my own money and often imbedded in the question is whether I prefer active or passive investing strategies. My answer is always both, and at Schwab we generally believe investors can benefit from traditional active management; e.g. mutual funds; alongside newer passive vehicles; e.g. exchange-traded funds (ETFs). But even before the creation of ETFs there were debates about the merits of passive vs. active. I wrote about this topic in February, but it's time for an update. In addition, my colleague Tony Davidow recently penned an article in which he answers the oft-asked question, "Are ETFs Dangerous?"

The primary advantages of passive investing are low fees, tax efficiency and transparency; but by definition, passive funds will never beat the indexes they track. The primary advantages of active investing are flexibility, the ability to benefit from strong security selection skills, and tax management strategies; but fees are higher and poorly-managed funds can and often do underperform their benchmarks. Blending the two is another way investors can be diversified within their portfolios.

Active underperformance

As of mid-year 2017, more than one-third of all assets in the United States are invested passively—up from one-fifth ten years ago. Last year, S&P Dow Jones Indices conducted a study, and found that about 90% of active equity managers underperformed their benchmarks over the prior one-, five- and 10-year periods; with fees explaining a significant portion of that underperformance. But many active manager counter that the environment since the financial crisis has been unique in that correlations between stocks and the indexes in which they’re housed have been exceptionally high. That is until recently.

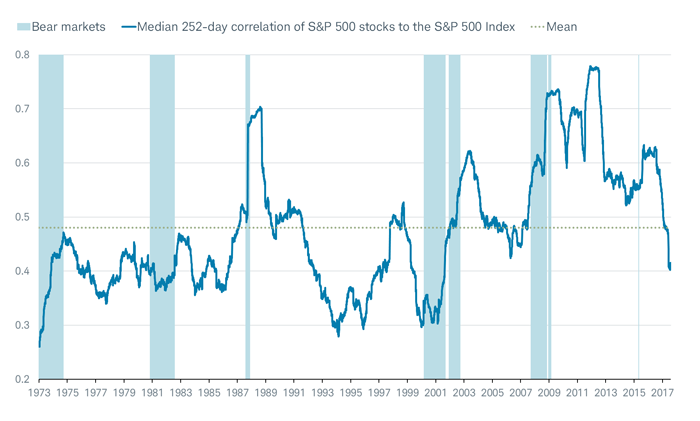

Plunging correlations

For those investors who continue to take an active approach to at least a portion of their portfolios, there is potentially some good news. Let’s start with correlations. As you can see in the chart below—which shows a one-year (trading days) rolling correlation of stocks within the S&P 500 to the S&P 500 Index itself—the correlation has broken down sharply. In other words, stocks are no longer displaying lemming-like behavior.

Source: Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2017© Ned Davis Research, Inc. All rights reserved.) As of August 25, 2017. Bear markets represent declines of 20% or more by the S&P 500.

From a below-mean low in 2006, the correlation shot to the moon by 2012, dropped to still-above the mean two years later, and then moved up again during the corrective phase for stocks in 2015. But since that 2016 peak, the correlation has plunged and now sits comfortably below mean levels. This is good news for active management styles as it ostensibly means managers can exploit the wider differentials among stocks’ individual behaviors. It also suggests that bear market risk is limited given that correlations tend to rise sharply heading into and during bear markets (shadings on the chart above).

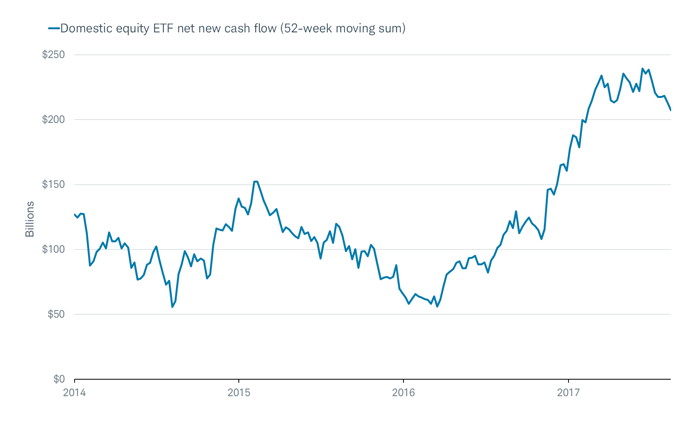

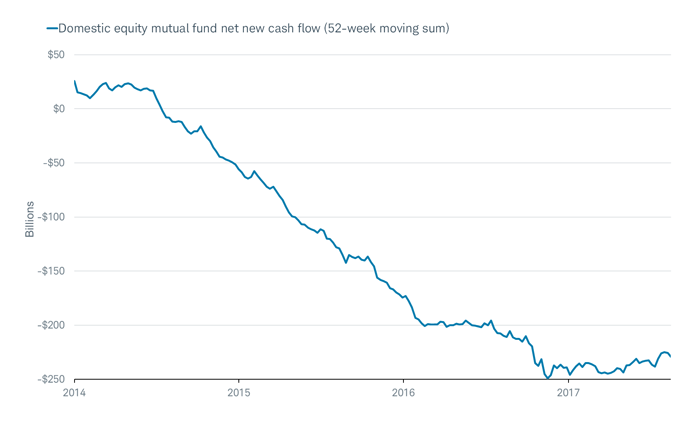

Fund flows' inflection?

Fund flow data appears to be showing a change underfoot as well. The top chart below shows U.S. equity ETF net new cash flows; in contrast with the bottom chart, which shows U.S. equity mutual fund net new cash flows. Not only have ETF flows rolled over, flows out of traditional mutual funds have flattened out over the past year and have oh-so-mildly trended higher. It’s too soon to declare this an important inflection point, but it bears watching.

Source: FactSet, Investment Company Institute, as of August 18, 2017.

Source: FactSet, Investment Company Institute, as of August 18, 2017.

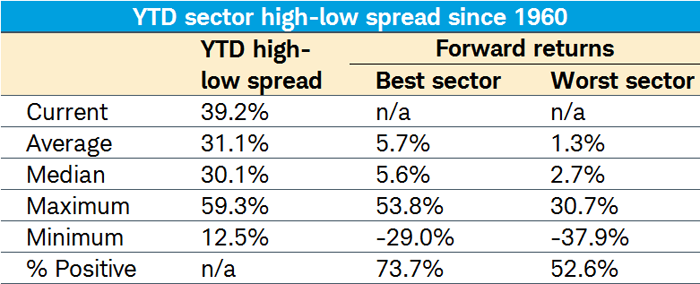

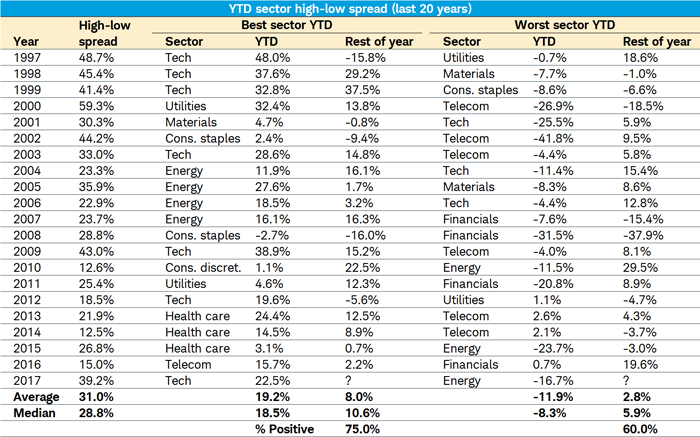

We're seeing the breakdown in correlations in sector behavior as well. Through Friday's close, the year-to-date performance of the best sector in the S&P 500 (technology at 23%) is nearly 40% higher than the worst performer (energy at-17%). According to Bespoke Investment Group (BIG), the current spread for this stage in the calendar is relatively high, but it's by no means a record. The average year saw a performance spread of more than 31%, with a median spread of over 29%. But this is the first year since 2009 with the spread near or above 40%.

What does this mean looking ahead?

The top table below looks at the long-term (since 1960); while the larger (I know, very crowded) table below looks at the past 20 years. In both cases, BIG found a trend: strong continued performance for the leading sector; and weak but improved performance for the lagging sector. Notably, the worst case scenario was much worse for the lagging sector; and the best was much better for the leading sector.

Source: Bespoke Investment Group, as of August 25, 2017.

Source: Bespoke Investment Group, as of August 25, 2017.

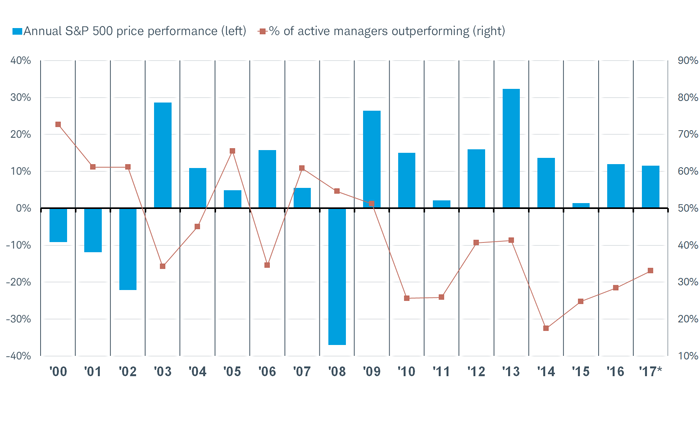

More active managers beating S&P

The waning lemming-like behavior of stocks and sectors is boding well for active managers given the aforementioned exploitation benefit. It has likely aided a continued improvement in the percentage of active managers who are outperforming the S&P 500, as you can see in the chart below.

Source: Strategas Research Partners. *As of July 31, 2017.

Indeed, only one-third of managers are outperforming, but that's double the low of about 17% in 2014. If correlations remain low, and sector dispersions high, the conditions will remain ripe for active to continue to make up some lost relative ground vs. passive.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

© Charles Schwab

Read more commentaries by Charles Schwab