Key Points

-

Volatility spike caused the market’s price drop; not the other way around.

-

Have we successfully gone from a FOMO to a LIFO market environment?

-

Sentiment and valuation excesses have corrected along with the market; but complacency should be kept in check.

We went from panic buying to panic selling in less than two weeks. What’s worth pondering is whether we have effectively moved from FOMO to LIFO. For those of you neither text slang nor accounting lingo inclined, that means we may have gone from a “fear of missing out” era to “last in, first out” era … in a very short span of time.

We may have also experienced a classic LTFC market. “Let’s test the new Fed Chair” has been a remarkably consistent tendency by markets, and clearly Jerome Powell is no exception, with last week being his first week on the job.

Were stocks simply overdue for a correction?

The short answer is yes, but it’s never as simple as that. We had traveled the longest span in S&P 500 history without either a 3% or a 5% pullback; and it had been two years since the last full 10% correction. But corrections don’t tend to come out of the blue, and there were a number of factors which had been troubling us over the past couple of quarters.

As we noted late last summer when we moved U.S. equities down from an overweight to a neutral, valuations were stretched and investor sentiment was beginning to show heightened levels of optimism—a contrarian indicator at extremes. That sentiment excess kicked into an even higher gear as the market closed out 2017 and roared into the first month of 2018.

I wrote about the anatomy of a melt-up in a December 2017 report; and that it represented a “risk” for the market in that they tend to end in melt-downs. So some of what we saw over the past couple of weeks may have been the melt-down that corrected much of the sentiment excess. The correction’s onset had its fundamental roots in heightened inflation expectations, the upside breakout in longer-term Treasury yields, and expected tighter monetary policy. But there were important technical underpinnings to last week’s action in particular.

Short vol trade implodes

I had the cartoon below created by our wonderful graphics artist Charlos Gary last November for my use at Schwab’s IMPACT conference. Clearly at least a couple of these “bubbles” have either burst (short vol) or had a heck of a lot of hot air let out of them (Bitcoin and complacency).

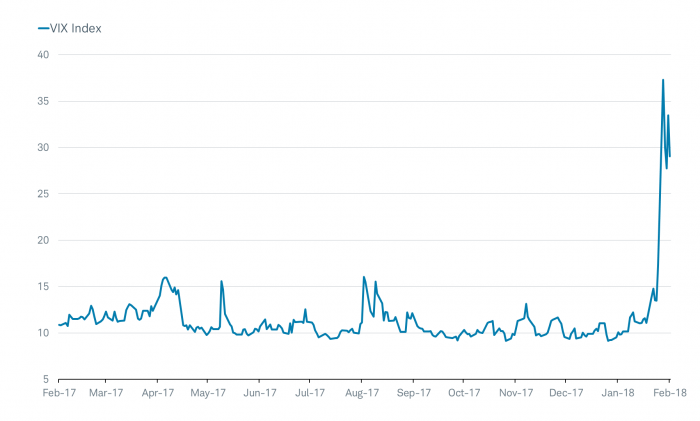

Culprit: VIX

In our minds, this correction was led by the surge in volatility—in other words, the spike in volatility caused equity prices to plunge; not the other way around. In mid-January, I tweeted out the results of a Bank of America Merrill Lynch Global Fund Managers Survey showing that the “short volatility” trade had taken over from the “long Bitcoin” trade as the most overcrowded in the marketplace (having attracted an unusually large number of participants).

VIX spikes

Source: FactSet, as of February 9, 2018.

The culprits of the spike in volatility have been exchange-traded notes (ETNs)—notably the VelocityShares Daily Inverse VIX Short Term ETN (XIV), which collapsed to effectively zero during last week’s turmoil. This was courtesy of the parabolic surge in the CBOE Volatility Index (VIX); with the XIV (among other inverse products) moving in the opposite direction.

Is it over?

According to Bloomberg and Evercore ISI, net-long VIX futures positioning increased to its highest level on record last week; largely due to the closing out of all the short volatility positions held by the primary inverse VIX funds as they unwind and/or close down. This was in stark contrast to the record net short positioning just a few weeks ago. As my colleague Randy Frederick, VP of Trading & Derivatives, put in his blog on Friday: “While past performance is no guarantee of future results, traders with cash on the sidelines who are considering adding equity exposure may want to consider waiting for two consecutive up market days, combined with strength into the close and a VIX at about 20 or below. If these things occur, it might be conveying reasonable assurance that the worst of this rout is probably over. We are not there yet.”

But even if the technical correction may have largely run its course, as we chronicled in our 2018 Outlook—the theme of which was “It’s Getting Late”—the low inflation and low volatility era is likely in the rear view mirror. The bull market, although likely still intact, will be met with sharper bouts of volatility and greater frequency of pullbacks/corrections.

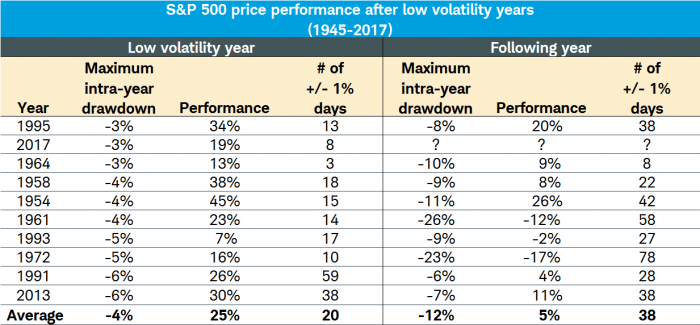

According to SentimenTrader, Last Monday’s >100% jump in the VIX was the second-largest in history since 1986 (combining the VIX with the former VXO version). After the other times when the VIX/VXO jumped by more than 50% in a single day, stocks never declined between one and six months later.

One of the reasons to expect continued higher volatility is simply because of the lack thereof last year. As I’ve shown in past communications, last year was the second-lowest year for maximum drawdown in history. Looking at the top-10 years based on lowest drawdowns, you’ll see a consistent pattern of subsequent years bringing higher drawdowns and a greater frequency of larger daily moves.

Source: Bloomberg, Strategas Research Partners LLC.

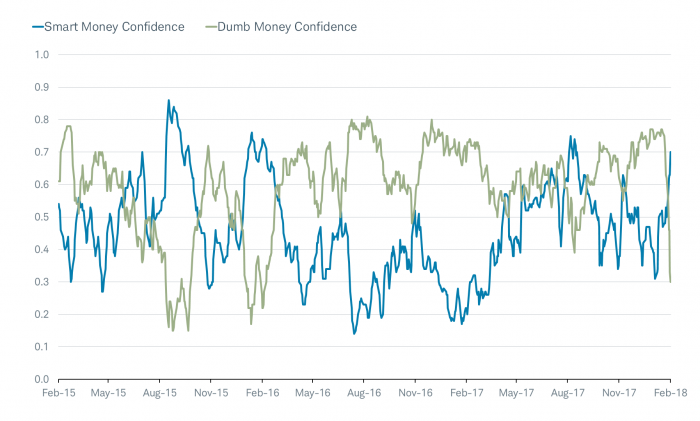

Sentiment excess corrected?

Given that investor sentiment had reached “froth” territory at the recent market highs, it’s instructive to look at what’s happened now that a correction has been registered. There are myriad sentiment indicators on which I keep a close eye, but one set I often highlight at extremes are the SentimenTrader “Smart Money and Dumb Money confidence indexes.

What I like about these is that they are behavioral measures of sentiment and go beyond just expressed attitudes. In other words, it’s at least as important to watch what investors are doing vs. just listening to what they’re saying—and especially important to see what the “good” market timers are doing with their money compared to the “bad” market timers.

Examples of Smart Money indicators include the OEX put/call and open interest ratios, commercial hedger positions in the equity index futures, and the current relationship between stocks and bonds. In contrast, examples of Dumb Money indicators include the equity-only put/call ratio, the flow into and out of the Rydex (bull and bear) series of index mutual funds, and small speculators in equity index futures contracts.

Smart Money confidence tends to be non-contrarian in nature; while Dumb Money confidence tends to be contrarian—especially when both are at extremes. As you can see in the chart below, the spread between the two is now at an extreme; having reversed from an opposing extreme recently.

Massive reversal in sentiment

Source: SentimenTrader, as of February 9, 2018.

The 40% spread between the two—with Smart Money confidence having surged and Dumb Money confidence having plunged—is a rare extreme with the S&P 500 still above its 200-day moving average. According to SentimenTrader, there were 58 days historically when this occurred since 1999. Over the next month, the S&P showed a positive return 88% of the time; with only one showing a loss of more than -1.8% (it was -2.9%).

Valuation excesses corrected?

Our more cautious stance on the stock market was also based on extended valuations; so the correction begs the question about whether valuation is now more reasonable. The short answer is yes.

As you can see in the chart below, courtesy of not only the correction in stocks—but also the unrelenting surge in earnings expectations for 2018—the market’s forward P/E has contracted a full two multiple points; well beyond the decline in the stock market’s value.

P/E plunges more than market

Source: FactSet, as of February 9, 2018.

The ascent of the “E” has been remarkable—and directly tied to the passage of tax reform. From a low of 11.1% last October, earnings expectations for 2018 year-over-year S&P 500 earnings growth has surged to 18.8% today according to Thomson Reuters (TR) data. And although there are yet to be published TR estimates for 2019, Evercore ISI has $170, which puts the multiple on 2019 earnings at under 15.5x.

More on technicals

- Beyond the short vol trade unwind, there are other technicals worth noting which could suggest the worst of the carnage is ending:

- S&P 500 e-mini futures have twice bounded off the 200-day morning average in intraday trading last week.

- Spikes in the percentage of stocks at at least 20-day lows are often climactic (>80% last week).

- The percentage of stocks above their 50-day moving averages is also washed out (<20% last week).

- Highest TRIN reading since mid-2015 (measures selling intensity); although we’re not yet seeing enough buying intensity.

- CBOE put/call ratio finally surged to >95th percentile last week.

- Unlike at the 2000 and 2007 peaks, market breadth was strong heading into this correction.

The net is that we have moved into a more mature phase of the cycle—both in terms of the economy and markets. The Fed is engineering the lift from unprecedented monetary policy with both rate hikes and the shrinking of its balance sheet. And although fiscal policy has been a growth kicker; it’s also likely an inflation kicker. So although the technical salt in the market’s wounds maybe getting washed out, enthusiasm for the “all clear” sign should be curbed.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

©2018 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

Read more commentaries by Charles Schwab