Key Points

-

A very strong jobs growth with benign wage pressures unleashed a strong day for the stock market.

-

Other than wage growth deceleration, the details of the report were quite healthy.

-

Tax reform can take some of the credit for stronger goods employment relative to services employment.

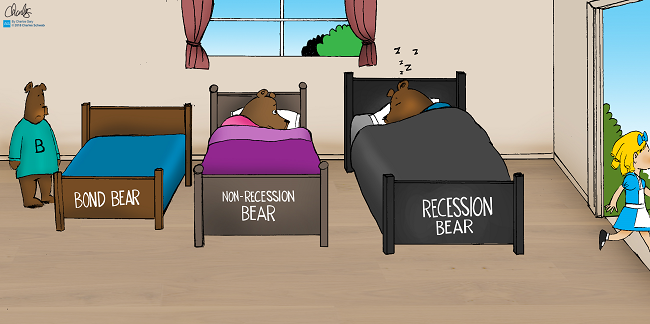

In the wake of the release of January’s jobs report—which saw a jump in average hourly earnings—I had our fearless cartoonist Charlos Gary create the visual below, with the headline “Goldilocks may be leaving the building.” Notice that the little bond bear has been awakened (as Schwab’s Kathy Jones has been detailing); but the equity bears are still tucked in their beds—albeit with the non-recession bear keeping a cautious eye on the situation.

Courtesy of last week’s February jobs report though, it looks like Goldilocks may have taken a step back into the building. For those not familiar with the analogy, an economy that’s operating “not too hot, but not too cold” is often referred to as a Goldilocks environment. We have been in such an environment as it relates to economic growth and wages/inflation for much of the current economic expansion. Yet the first market correction in two years was ushered in during the early part of February on the back of the aforementioned hotter wage data in the January jobs report—and the concomitant jump in the 10-year yield to about 2.9%.

Ninth birthday parties are fun

The stock market took it as another reason to celebrate on Friday, which was the bull market’s ninth birthday (using the simple 20% +/- definition for bull/bear markets), during which time the S&P 500 has quadrupled. The muted wage gains for Main Street tend to get cheers from Wall Street because tame wage growth can keep inflation from accelerating and keep a lid on the number of rate hikes by the Federal Reserve.

A devil (and some angels) in the details

Non-farm payroll growth surprised on the upside with a jump of 313,000 jobs—well above the consensus of 205,000; but partly boosted by weather effects. In addition, revisions added an additional 54,000 to the prior two months’ reports. The private-sector/public-sector split was 287,000 and 26,000, respectively; and the largest gains came in the construction, retail (surprise!), and manufacturing sectors. Only the information sector was a jobs loser last month. U.S. companies have added an average of 242,000 jobs per month over the past three months—above 2017’s pace of 182,000. The string of 89 consecutive months of job gains is the longest streak in history.

The recently-passed tax reform has helped to boost both capital spending and job growth; and as a result, goods employment growth (led by manufacturing) has surged to its highest level since 1984. This is in contrast to service employment, which has been decelerating in typical late-cycle fashion.

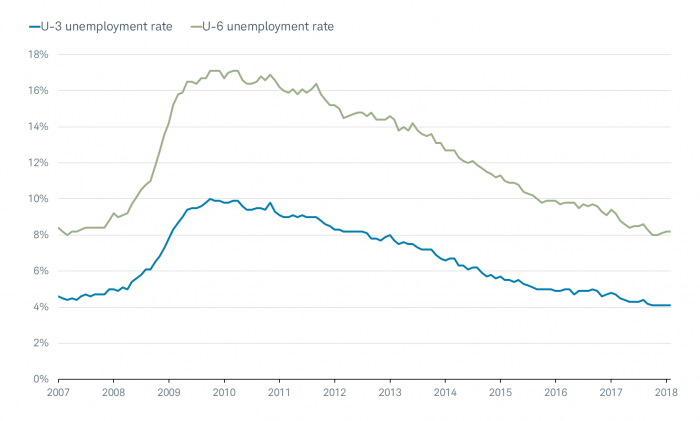

The headline U3 unemployment rate remained steady at 4.1%, although the broader U6 rate (incorporating marginally-attached workers and those working part-time for economic reasons) ticked up to 8.2%. As you can see in the chart below, both have descended consistently since the 2010 peak.

U3 vs. U6

Source: Department of Labor, FactSet, as of February 28, 2018.

Time to participate

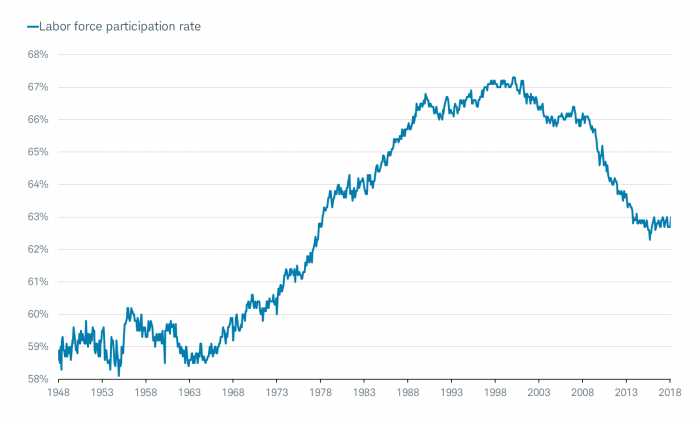

The unemployment rate’s underlying details were quite strong. Household survey employment—the data from which the unemployment rate is calculated, and distinct from non-farm payrolls—surged by 785,000. In addition, the labor force participation rate rose 0.3 percentage points to 63% (as you can see in the chart below); which explains why the unemployment rate did not drop alongside the payrolls gain.

Participation rate ticks higher

Source: Department of Labor, FactSet, as of February 28, 2018.

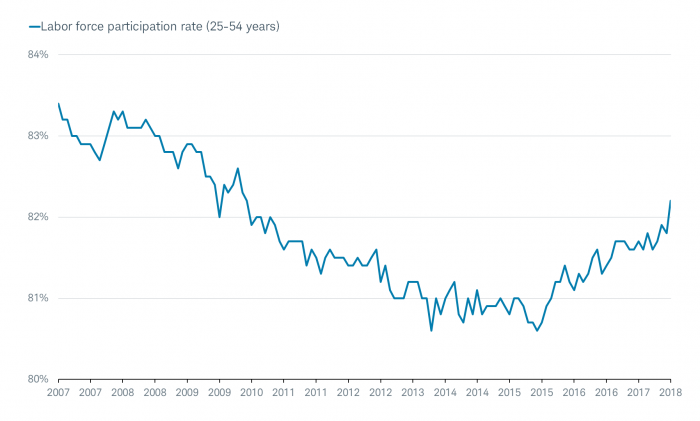

Importantly, within the labor force data is the participation rate of “prime age workers,” which are those between 25 and 54 years old (seen in the chart below). That rate continues to accelerate and currently sits at 82.2%. Attention is often focused on this range given that education and/or retirement are lower influencers and therefore don’t skew the data.

Prime working age participation ticks higher

Source: Department of Labor, FactSet, as of February 28, 2018.

Wall Street happier than Main Street?

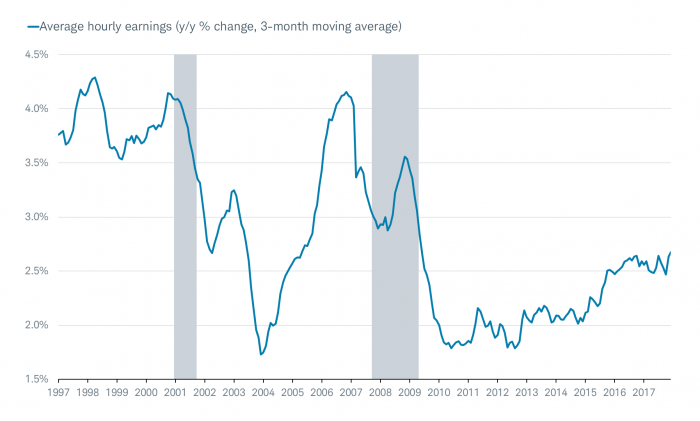

Less positive for workers was wage growth. Average hourly earnings (AHE)—the most common measure of wages—were up 0.1% month-over-month, which was below the 0.2% consensus. Garnering more attention was the year-over-year change, which fell to 2.6% from 2.8% the prior month (which in turn was revised from 2.9%). It is still up from the 2.5% average last year, but was a disappointment for workers (although not the stock market) nonetheless.

One of the problems though with an “average” measure of wages is that it can be skewed by “mix shift.” A visual way to explain this can be seen in the chart below, which is a smoothed (three-month moving average) look at AHE.

Benign average wages growth

Source: Department of Labor, FactSet, as of February 28, 2018.

See something odd in the second gray-shaded bar, which represents the Great Recession? Does anyone think wage growth was accelerating during the worst recession since the Great Depression? Of course not. What was happening is that a majority of workers losing their jobs during that recession were on the lower end of the wage spectrum, which biased up the average. The opposite has been a factor in the expansion’s subdued wage growth. Baby Boomers are retiring in greater numbers—and they tend to be on the higher end of the wage spectrum. On the other hand, Millennials are experiencing stronger job growth—and they tend to be on the lower end of the wage spectrum due to their younger age. Those forces have conspired to bias down the average.

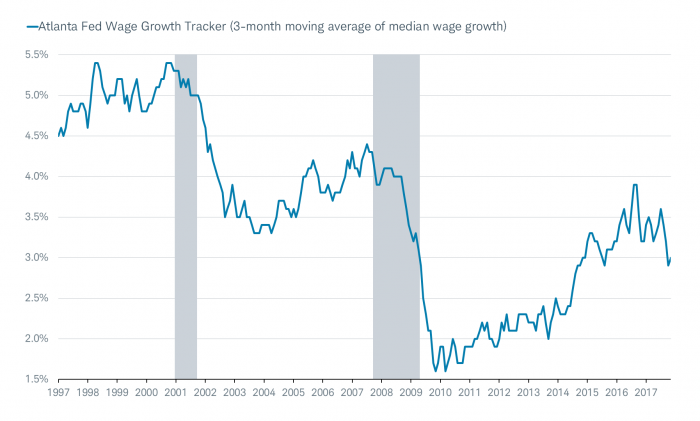

This is why “median” measures of wage growth are also tracked by market watchers and economists. One such measure—which tracks the median percent change in the wages of workers observed 12 months apart—is the Wage Growth Tracker from the Federal Reserve Bank of Atlanta. Although it’s recently rolled over, you can see in the chart below that wage gains via this measurement criteria have been running at least 0.5 percentage point above AHE.

Benign median wages growth

Source: Federal Reserve Bank of Atlanta calculations, as of January 31, 2018.

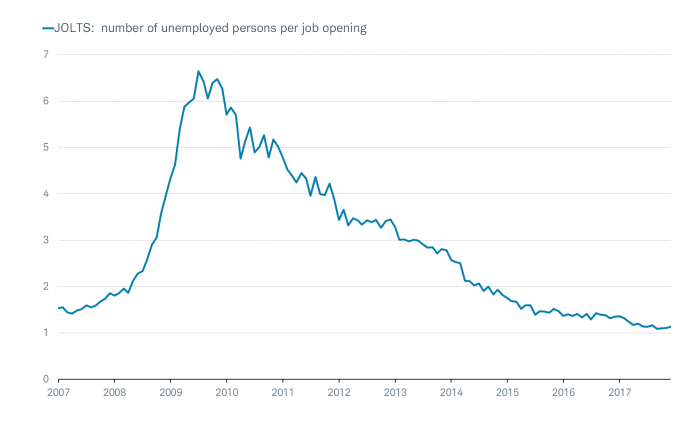

A JOLT of good news

Although it’s not reported in conjunction with the monthly payroll jobs report, there is another series of jobs data that garners attention and comes from the Job Openings and Labor Turnover Survey (JOLTS), which is conducted by the Bureau of Labor Statistics. The data includes employment, job openings, hires, quits, layoffs and discharges, and other separations.

Job openings are just off a recent all-time high, but importantly, the number of unemployed for each job opening has fallen from a peak of 6.6 in 2009 to just above 1.0 today. That means there is nearly one job available for every unemployed worker—helping explain the jump in labor force participation.

Nearly one job for everyone unemployed

Source: Department of Labor, FactSet, as of December 31, 2017.

In sum

The net is that the U.S. economy continues to be able to create enough jobs to both accommodate the re-emergence of job hunters and keep the unemployment rate in a declining trend. At the same time, relatively tepid wage growth should keep near-term pressure on inflation from heating up. For now, it’s being cheered by the stock market, but a revival of frothy investor sentiment represents a risk worth watching given its contrarian tendencies.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

©2018 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

Read more commentaries by Charles Schwab