Key Points

-

April’s leading indicators posted another strong showing and continue to suggest little near-term recession risk.

-

Leading indicators have done a stellar job “forecasting” subsequent economic growth.

-

But leading indicators—which include the stock market—have done a less-than-stellar job forecasting subsequent stock market performance.

“Leaders aren’t born, they are made.” - Vince Lombardi

LEI history

In the 1960s, the U.S. Department of Commerce began researching and releasing business cycle indicators, which use composite data points—including manufacturing, construction and stock market indicators—to time economic cycle turning points. More than 20 years ago, The Conference Board took over the business indicator program from the government and created the Leading Economic Index (LEI), which was expressly designed to forecast recessions and subsequent recoveries.

Caveat: the LEI is not the be-all end-all. Upon its release each month, much of the data is a month or two old and nearly all of the 10 sub-components have already been released (or are available) prior to the release of the LEI itself. That said, the indicator has successfully rolled over in advance of each of the past five recessions; and also rolled up within recessions in advance of each of the past five recoveries.

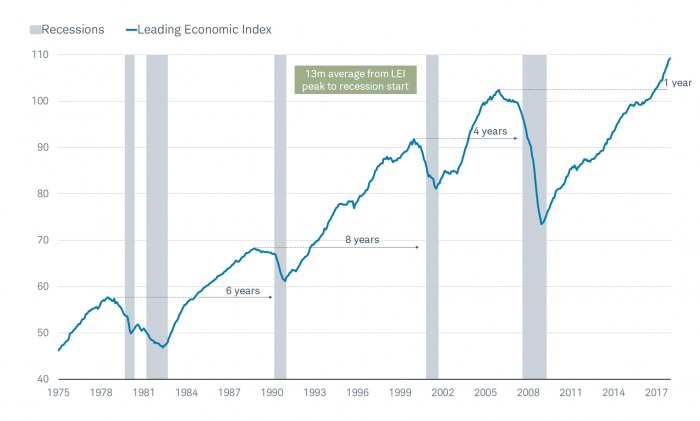

As you can see in the chart below, not only is the LEI still improving, it’s improving at an accelerated pace. April’s reading was +0.4% with the prior month revised up to +0.4% from +0.3%. Eight of the 10 LEI subcomponents made positive contributions, led by the interest rate spread.

Recession risk low

Since the mid-1970s, the average span between a peak in the LEI and the start of the subsequent recession had been about 13 months. The dotted lines on the chart below show the spans of what I think of as the LEI’s “round trips” (from the peak in the prior cycle to the point when the LEI took out that prior high). This is when recoveries become expansions—when the leading indicators have recovered all of their recession-related weakness and move to new higher ground.

Leading Economic Index Accelerating

Source: Charles Schwab, FactSet, The Conference Board, as of April 30, 2018.

The solid lines—and commensurate years’ markers—show the spans between the round trip point and the subsequent recessions. In other words, for the past three cycles (with the double-dip early-1980s recessions considered as one), once the LEI completed its round-trip, a recession was still four-to-eight years ahead. It’s only been a year since the LEI took out its pre-financial crisis high—after the longest period below it in modern history. So, history suggests there could still be a long runway between now and the next recession. It may be a stretch to hope for another three-to-seven years, but it’s not a stretch to assume near-term recession risk is quite low.

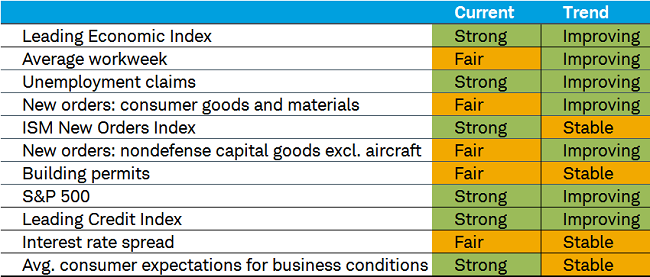

The table below highlights both the current reading and, more importantly, the trend in the 10 sub-components of the LEI. As you can see, none of them are currently flashing red.

Source: Charles Schwab, as of April 30, 2018.

LEI as economic forecaster

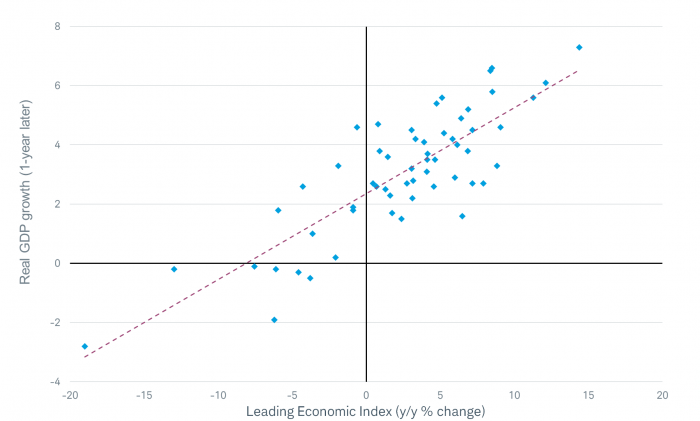

As studied by The Leuthold Group, and constructed into scattergram charts by us, the LEI has done a great job of forecasting real GDP growth with a one-year time horizon—at least based on its current constitution (The Conference Board makes adjustments to the indicators from time to time). As you can see in the chart below, the correlation between the year-end 12-month change in the LEI and the subsequent year’s growth in real GDP has been a strong 0.83%.

LEI Leads Economy

Source: Charles Schwab, Bloomberg, Bureau of Economic Analysis, FactSet, The Conference Board. 1960-2017.

In fact, as you can eyeball in the chart, when the LEI was up by any amount during a given year, real GDP growth in the following year was never below 1.5%.

LEI as stock market forecaster?

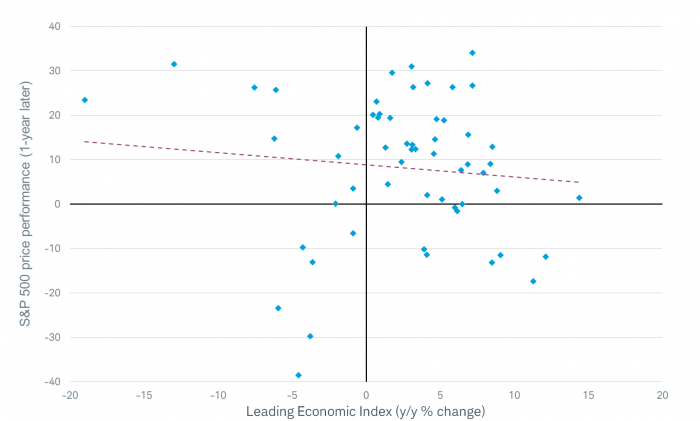

Given that the stock market is one of the LEI’s components, and given that many bulls use the argument that a recession remains well in the future, many assume the LEI is also sending an all-clear sign for stocks. Not so fast. As you can see in the related scattergram below, there is historically no relationship between changes in the LEI and subsequent one-year performance of the S&P 500. In fact, the regression line actually shows a slight inverse correlation.

LEI Doesn’t Lead Stocks

Source: Charles Schwab, Bloomberg, FactSet, The Conference Board. 1960-2017.

This relationship—or lack thereof—highlights two important factors: the stock market often leads many of the other leading indicators (and the index collectively); and there are myriad other drivers of stock market behavior. Interestingly though, if you reverse the causality in the chart above, and look at how real GDP has performed following changes in the S&P’s performance, Leuthold calculated a positive correlation of 0.55%: “…the stock market has a huge advantage over human forecasters in that its own action influences the outcome.”

In sum

Investors can take comfort, when observing leading economic indicators, that there is limited recession risk at present. But one should not extrapolate the LEI’s strength into a guarantee of continued stock market strength given the myriad other drivers of stock market behavior. That said, the stock market’s latest strength is a fillip to the economy.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

©2018 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

Read more commentaries by Charles Schwab