Milemarker 92: Record String of Positive Payrolls

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Points

-

The May employment report was strong across nearly all metrics, with the notable exception of the labor force participation rate.

-

The unemployment rate is comfortably below the natural rate of unemployment, which has implications for inflation.

-

Labor force participation remains moribund, but the devil is in the details.

The May employment report, put out by the Bureau of Labor Statistics (BLS) this past Friday, made the cover of Saturday’s NY Post with a headline of “We’re in the Money.” I’m not sure that represents a classic contrarian signal, but it’s not a stretch to say that the labor market has become quite tight and that it represents one of many signs that the economic expansion is in its latter stage(s).

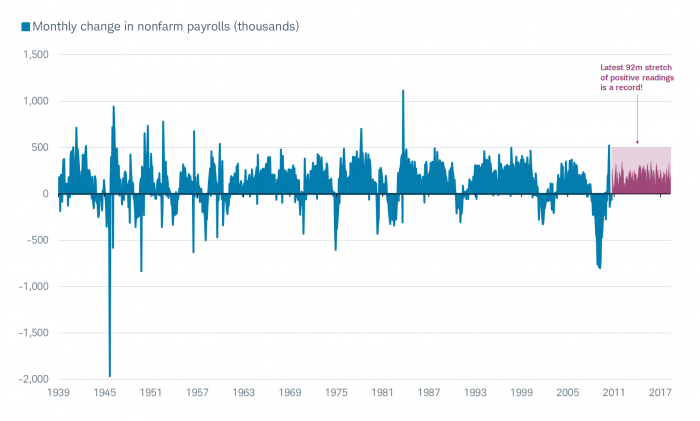

92 months and counting

The employment report for May had much in it for the economic bulls to cheer. It was the 92nd month during which there was positive payrolls growth—the longest stretch in the history of the data.

Record Run For Job Growth

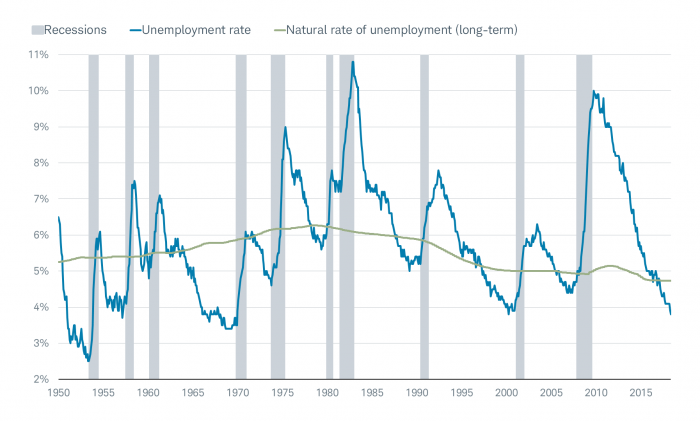

The unemployment rate dipped further to 3.8%—in fact, it was precisely 3.755%, so it almost made it to 3.7% when rounded. It’s often the case that when I mention or show the standard (U3) measure of unemployment, it’s met with criticism that it fails to incorporate the marginally-attached worker and/or those working part-time for economic reasons. Those are captured by the broader U6 measure of unemployment.

It’s natural

The chart below shows the traditional U3 measure of unemployment back to 1950, tracked against the “natural rate of unemployment” (NRU)—a trend that, in theory, should boost inflation. The NRU is the minimum unemployment rate resulting from real, or voluntary, economic forces. Even in a healthy economy, there is some level of unemployment for three primary reasons:

- Frictional unemployment: workers in between jobs

- Structural unemployment: unavoidable mismatch between workers’ job skills and employers’ needs

- Surplus unemployment: government or union intervention with minimum wages and/or wage controls

Unemployment Rate Well Below NRU

Source: Charles Schwab, Bureau of Labor Statistics, Congressional Budget Office, Factset. Unemployment rate as of May 31, 2018. Natural rate of unemployment as of December 31, 2017.

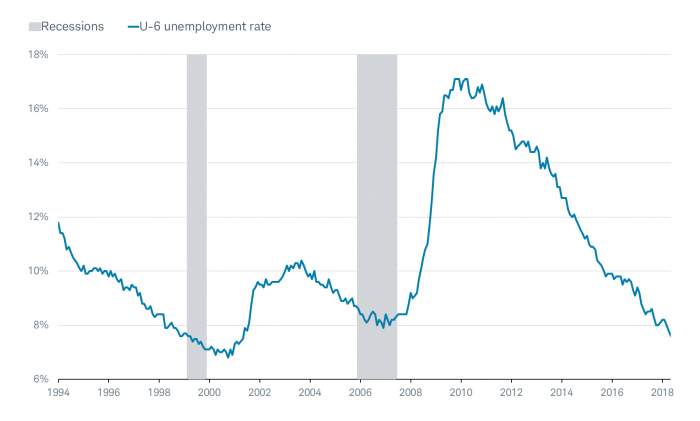

The chart below shows the “underemployment rate,” or U6, which is a 17-year low and below the trough of the past economic expansion.

Underemployment Way Down

Source: Charles Schwab, Bureau of Labor Statistics, Factset, as of May 31, 2018.

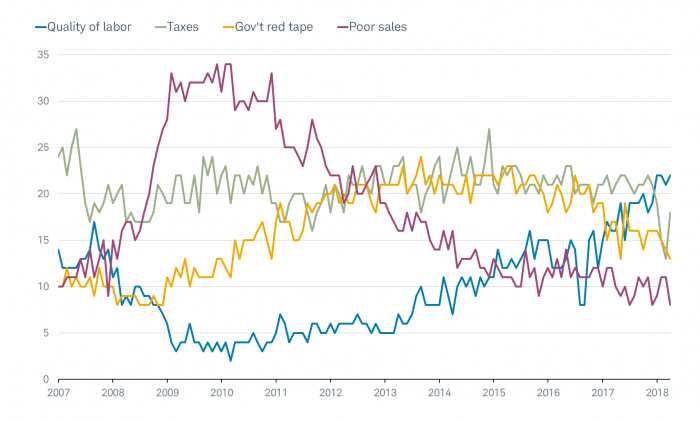

Skills gap

Within the definition of NRU above, you’ll see mention of structural unemployment—specifically the skills mismatch problem. This is an increasingly vexing problem, confirmed by the monthly survey conducted by the National Federation of Independent Business (NFIB). When asked about their “single most important problem,” companies are most frequently citing “quality of labor.” You’ll see that this was the lowest among concerns at the start of this expansion in 2009, but now it’s the highest.

NFIB’s Single Most Important Problem

Source: Charles Schwab, FactSet, as of April 30, 2018.

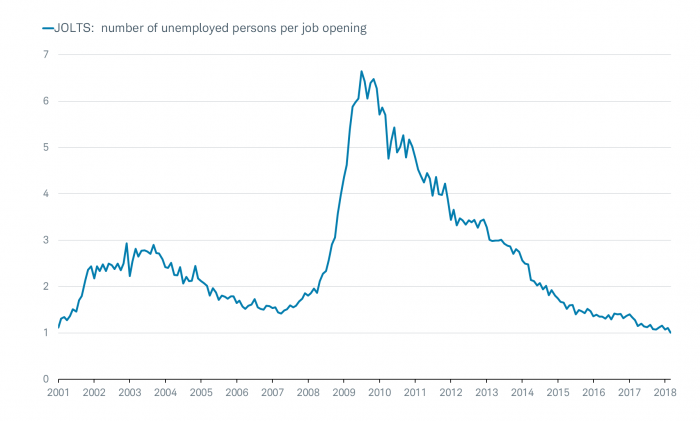

This is why, although there is presently one job available for every person who is unemployed (see chart below), there remains reasonably high angst about employment prospects. I think of the skills gap as an “ocean liner” problem vs. a “speed boat” problem, in that it will take time to turn that around.

One Job Opening For Everyone Unemployed

Source: Charles Schwab, Bureau of Labor Statistics, FactSet, as of March 31, 2018. JOLTS= Job Openings and Labor Turnover Survey.

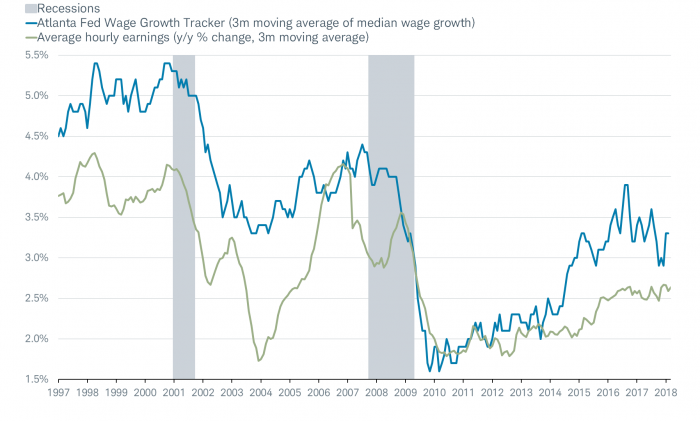

Lackadaisical wage growth

The May jobs report also brought a much-awaited pick-up in wage growth, as measured by average hourly earnings (AHE), which grew at 2.7% year-over-year. Although that is at the upper end of the range in which they’ve been since 2016, wage growth remains fairly lackadaisical. Part of the problem is that a growing percentage of the new jobs being created are among lower-wage industries, like education/health services and retail.

That said, as I’ve highlighted in the past, the average in AHE also causes some “mix shift” problems. In other words, AHE is presently somewhat biased down courtesy of younger new workers coming into the job market at naturally lower wage levels; while older, higher-wage earners are retiring. This is why “median” measures of wage growth are also tracked (they eliminate the mix shift problem by only looking at wage growth of workers who have been in the work force for the full measurement period).

Both measurements are in the chart below (using three-month averages); and as you’ll see, the median measure has run consistently higher than the average measure over the past six years.

Improving Wage Growth

Source: Charles Schwab, Current Population Survey, Bureau of Labor Statistics, FactSet, Federal Reserve Bank of Atlanta calculations. Average hourly earnings as of May 31, 2018. Atlanta Fed Wage Growth Tracker as of April 30, 2018.

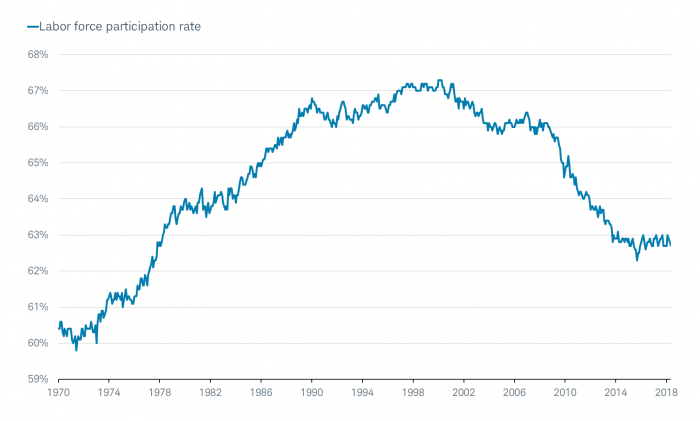

Moribund LFPR

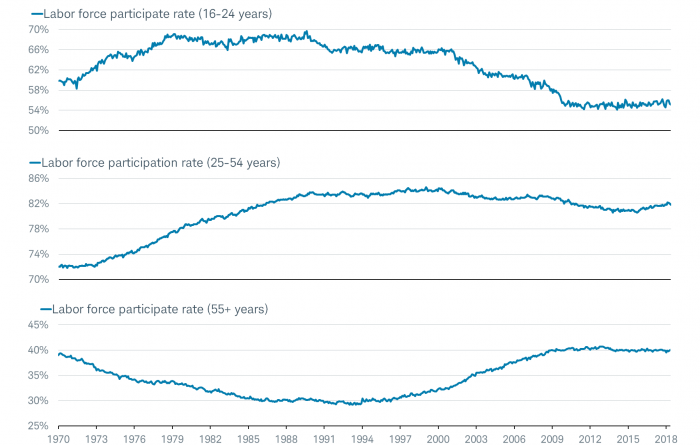

Finally, not all the news was cheered in last Friday’s jobs report. The labor force participation rate (LFPR) has made virtually no headway over the past five years. However, there are differences in the trends based on age cohort, as you can see in the charts below. For the youngest and oldest cohorts, the flatness in the trend has mirrored the overall LFPR. However, for the prime-working age cohort (25-54 years), the trend turned up a few years ago.

Flat LFPR

Less Flat for Prime Working Age

Source: Charles Schwab, Bureau of Labor Statistics, Factset, as of May 31, 2018.

LFPRs

Some calculations, including by Oxford Economics and Haver Analytics, show the age-adjusted LFPR (with demographic adjustments made) at about 67%; comfortably higher than the 62.7% overall LFPR rate.

The LFPR has evolved with different patterns, and for different reasons, across demographic groups. A rise in school enrollment has largely offset declining participation for younger workers since the 1990s. But there are also some sad details in the numbers.

Devil in the details

According to research by Alan Krueger of Princeton University earlier this year, “…participation has been declining for prime-age men for decades, and about half of prime age men who are not in the labor force may have a serious health condition that is a barrier to working. Nearly half of prime age men who are not in the labor force take pain medication on any given day; and in nearly two-thirds of these cases, they take prescription pain medication. In fact, labor force participation has fallen more in U.S. counties where relatively more opioid pain medication is prescribed, causing the problem of depressed participate and the opioid crisis to become intertwined.”

In sum

The data remains more than strong enough to keep downward pressure on the unemployment rate; and upward pressure on the trend in short-term interest rates. In fact, in the immediate aftermath of the jobs report on Friday, expectations for four (or more) total rate hikes this year by the Federal Reserve jumped from less than 15% to nearly 30%. The likelihood of a June rate hike is a virtual certainty.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

©2018 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All