As we move toward the finale of first quarter earnings season, results have been a bit better than expected, but barely in positive territory.

The earnings beat rate has been above historical norms; while revenues have been a touch more disappointing relative to expectations.

Multiples have expanded this year thanks to a strong stock market; but earnings will have to do more of the heavy lifting at some point.

First, jobs

Before I get to the subject at hand, I want to provide a quick update on last Friday’s April jobs report from the Bureau of Labor Statistics. Similar to the first quarter gross domestic product (GDP) report, the headline strength in the employment report masked less-robust underlying details. The non-farm payroll print of +263k was well above the 190k consensus expectation per Bloomberg, with a net small positive revision to the prior two months. Average hourly earnings (AHE) were +0.2% month/month (+3.2% year/year), which was below the consensus expectation.

The unemployment rate dropped to 3.6%, the lowest in nearly 50 years; however, the reasons why represent the cloud in an otherwise sunny sky. The payroll figure comes from the “establishment survey,” while the unemployment rate is derived from the “household survey.” Within the latter survey, there was a 490k plunge in the labor force, which was the sharpest decline since October 2017 and followed a 224k drop in March. In addition, the pool of available labor also sank by 493k and has been down for three consecutive months by a total of 844k; which is the lowest level in 18 years. Finally, the labor force participation rate (LFPR) also pulled back, from 63% in March to 62.8% in April; with another blemish being the drop in the average workweek.

In other economic news, both ISM surveys—manufacturing and non-manufacturing—were also weaker than expected. These are both surveys, as opposed to hard data, and are consistent with other “soft” economic data, which has been disappointing relative to expectations. That’s a good segue to today’s topic, which is first quarter earnings for the S&P 500.

Earnings highlights

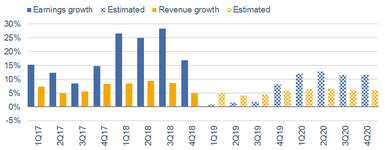

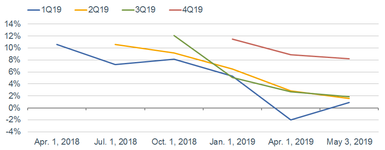

After a gangbuster year in 2018, expectations for earnings growth this year began falling off a cliff last summer. Some of that was due to simple “math”—given that the year/year comparisons became much more difficult after the boost provided to 2018’s earnings from the late-2017 corporate tax cut. In the first chart below, which uses data from Refinitiv, you can see the dent in growth expected for this year, but an expected pickup in 2020. The chart following that shows the trajectory of each quarter’s estimates from their initial readings to the latest set of expectations.

The Big 2019 Dip

Source: Charles Schwab, I/B/E/S data from Refinitiv, as of May 3, 2019.

As you can see above, from a dip into negative territory last month, now that most companies’ earnings have been reported, the expectation has moved back into ever-so-slightly positive territory. As you can see though, there has been no lift yet to the remaining quarters’ estimates.

Earnings details

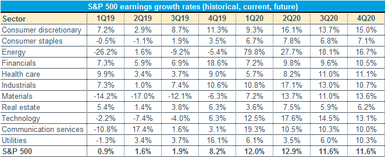

As of Friday, 390 of the S&P 500’s constituents had reported earnings for the first quarter. The year/year “blended” estimate (actual plus expected for those companies’ earnings not yet reported) is now 0.9%. A better-than-average 75% of companies have reported earnings above estimates, with a better-than-average 18% coming in shy of those estimates. Over the past 25 years, the averages are 65% and 21%, respectively. Revenues have been a bit more disappointing relative to expectations. Although revenue growth is 5.1% so far for the quarter, less than 58% of companies have beaten expectations, while 42% have missed expectations. Over the past 17 years, the averages are 60% and 40%, respectively.

Source: Charles Schwab, I/B/E/S data from Refinitiv, as of May 3, 2019.

Likely courtesy of weak global growth, S&P 500 companies with a higher proportion of foreign sales have reported weaker relative earnings vs. their domestic peers. Courtesy of last year’s collapse in oil prices, energy is taking it most on the chin; but with the sharpest recovery expected in 2020. Unlike much of last year, stocks of companies beating estimates have been generally outperforming those who have missed. But also unlike last year is the relationship between earnings and valuation.

2019’s mirror image

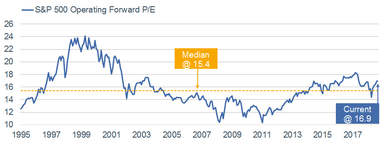

Last year was marked by a surge in earnings growth (the “E” in P/E), a plunge in the “P” in the fourth quarter, and a resultant contraction in multiples throughout the course of the year. There are a few key reasons why that occurred. First, the stock market is a discounting mechanism and was likely looking ahead to the fall off in earnings seen as likely in 2019. Second, the Fed was raising interest rates last year and financial conditions were tightening (according to the Bloomberg Financial Conditions Index)—macro conditions that we’ve historically seen herald a contraction in multiples. Fast-forward to this year and we’re experiencing the mirror image of 2018. Earnings estimates have fallen sharply, but multiples have been expanding alongside a strong stock market. Part of this phenomenon can be explained by the Fed having moved to pause mode in January; plus the corresponding loosening of financial conditions since the stock market’s crescendo low on Christmas Eve 2018. You can see a chart of the forward P/E for the S&P 500 below. Although not at a historical extreme, it’s elevated enough now that absent a “throw caution to the wind melt-up in stocks” scenario, earnings growth and expectations thereof likely need to turn more positive to justify continued multiple expansion from these levels.

P/E Back Above Historical Median

Source: Charles Schwab, FactSet, as of May 3, 2019.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.