Schwab Sector Views is our three- to six-month outlook for 11 stock sectors, which represent broad sectors of the economy. It is designed for investors looking for tactical ideas. We typically update our views every two weeks.

U.S. stocks have made limited headway over the past 20 months, with the S&P 500® index up around 4% from its January 2018 high.1 Most of the choppiness has been tied to trade-related news, although concerns about Fed policy and the flattening and at times inverted Treasury yield curve have come into play, as well.

One of the lessons that should come from observing what has been happening is that trying to trade around headlines is a potentially treacherous exercise. With so much daily noise, we continue to recommend a disciplined strategy around diversification and rebalancing.

Tied to that has been our sector strategy, which has been fairly “neutral” over the past year, having only one outperform rating (Health Care) and only one underperform rating (Communication Services). The remaining nine sectors have marketperform ratings.

Frankly, what has “worked” well over the past year or so has been factors over sectors. For those who are unfamiliar with factor investing, it’s an investment approach that focuses on stock characteristics, such as size, price momentum, value, volatility and other potential factors. Over the past year or so, stocks with low volatility and strong price momentum have consistently led the pack, while traditional and relative value factors have lagged the most.

However, as overall market volatility declined at the beginning of September, both value factors and more-cyclical sectors rebounded, along with higher-volatility stocks. This was an interesting reversal of a trend, but for now it was short-lived, lasting only a week or so. Last week saw a return to the factors that had dominated the year-to-date performance up to September. Any additional rotation would bear watching to see whether factors become as volatile as sectors, and/or whether a more-cyclical leadership trend portends a better economic outlook.

Sector performance has been choppy, too

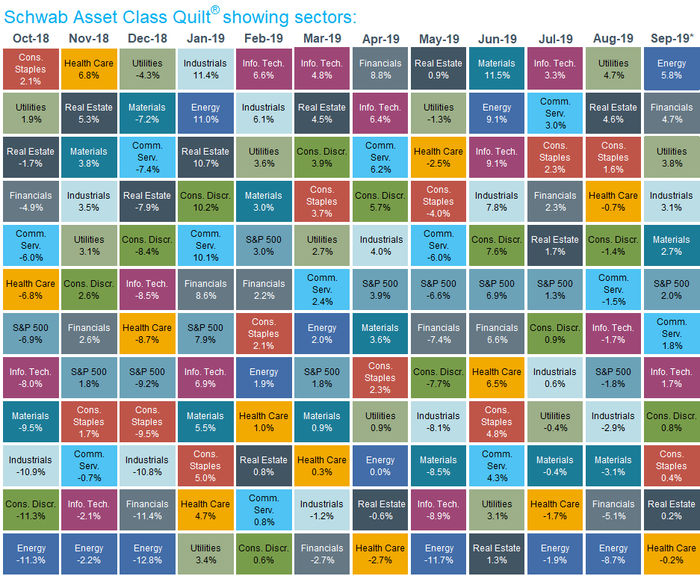

Highlighting the volatility of sectors and the rationale for a relatively neutral overall recommendation, we put together a handy “quilt chart” showing the movement of the S&P 500’s 11 sectors on a month-to-month basis over the past year. Similar to quilt charts that show asset classes on a year-to-year basis, this version highlights the difficulty of trading sectors in the short term: The monthly fluctuations have been all over the place.

Sector leadership has been volatile on a month-to-month basis

Source: Charles Schwab, Bloomberg, as of 9/25/2019. Sector performance is represented by price returns of the following 11 GICS sector indices: Communication Services, Consumer Discretionary, Consumer Staples, Energy, Financials, Health Care, Industrials, Information Technology, Materials, Real Estate, and Utilities. Returns of the broad market are represented by the S&P 500® index. Past performance is no guarantee of future results. For illustrative purposes only.

What investors can consider now

It continues to be a difficult environment in which to trade around short-term news, even if short-term news is having an outsized impact on day-to-day and month-to-month market behavior. As I often say, investing should always be a process over time; never about a moment in time. There are no free lunches in the business of investing; but sticking to the tried-and-true disciplines around diversification and periodic rebalancing is as close as it gets.

1 Source: S&P Dow Jones Indices. The S&P 500 closed at 2872.87 on 1/26/2018, and at 2,984.87 on 9/25/2019.

Schwab Sector Views: Our current outlook

Source: Schwab Center for Financial Research, FactSet (for YTD total returns) and S&P Dow Jones Indices (for S&P 500 sector weightings). Sector performance data is based on total return for each S&P 500 sector subindex (see “Important Disclosures” for index definitions). Sector weighting data is as of 08/30/2019; data is rounded to the nearest tenth of a percent, so the aggregate weights for the index may not equal 100%.

What do the ratings mean?

The sectors we analyze are from the widely recognized Global Industry Classification Standard (GICS®) groupings. After a review of risks and opportunities, we give each stock sector one of the following ratings:

- Outperform: likely to perform better than the broader stock market*

- Underperform: likely to perform worse than the broader stock market

- Marketperform: likely to track the broader stock market

*As represented by the S&P 500 index

How should I use Schwab Sector Views?

Investors should generally be well-diversified across all stock market sectors. You can use the Standard & Poor's 500® Index allocations to each sector, listed in the chart above, as a guideline.

Investors who want to make tactical shifts in their portfolios can use Schwab Sector Views' outperform, underperform and marketperform ratings as a resource. These ratings can be helpful in evaluating and monitoring the domestic equity portion of your portfolio.

Important Disclosures

Schwab Sector Views do not represent a personalized recommendation of a particular investment strategy to you. You should not buy or sell an investment without first considering whether it is appropriate for you and your portfolio. Additionally, you should review and consider any recent market news. Supporting documentation for any claims or statistical information is available upon request.

All expressions of opinion are subject to change without notice in reaction to shifting market or other conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Diversification and rebalancing strategies do not ensure a profit and do not protect against losses in declining markets. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

© Charles Schwab & Co.

© Charles Schwab

More Alternative Investments Topics >