Key Points

-

The next decade will not look like the last one; nor will the next year likely look like the last year.

-

Economic bifurcation is expected to persist to start 2020; with trade/political uncertainty plaguing business confidence and manufacturing; but labor conditions continuing to support consumers and services.

-

Fed policy should continue to support stocks; but stretched valuations suggest earnings will need to step up and do more of the market’s heavy lifting.

Below is Liz Ann Sonders’ full 2020 outlook for U.S. stocks and the economy. For more, you can read her previously published summary outlook, as well as the complete 2020 Schwab Market Outlook.

As we are about to turn the page on another decade, I was reminded of a quote from Mother Teresa that is etched on a plaque in my daughter’s room. She, too, is about to leave the teen years behind next month.

“You will teach them to fly, but they will not fly your flight. You will teach them to dream, but they will not dream your dream. You will teach them to live, but they will not live your life. Nevertheless, in every flight, in every life, in every dream, the print of the way you taught them will remain.”

The next decade will likely not look like this past decade; but there are lessons for investors that should resonate throughout time. Given that nearly every market across the spectrum of equities and fixed income had above-average returns over the past decade, it is likely a feat which won’t be repeated in the next decade.

2020 vision

But for now, let’s focus on the next year. In the summary outlook we released last week, the theme was “What may tip the scale?” It highlighted the competing positive and negative forces that will continue to work both for and against the U.S. and global economies and markets. My section was of course on the U.S. economy and stock market. Its key points:

- The U.S. economy likely will remain bifurcated—at least to start the year—with beleaguered manufacturing and business investment, but healthier services and consumer spending.

- Easy monetary policy should carry over to 2020; but it isn’t the elixir to ongoing trade and political uncertainty.

- The recently announced “Phase One” trade deal between the United States and China could help stabilize manufacturing/business investment; but corporate animal spirits are unlikely to be meaningfully revived.

The net as we enter 2020 is that we remain tactically neutral on U.S. equities—which means we continue to recommend investors stay at their long-term strategic allocation to equities, while using volatility to rebalance back to those long-term targets. Within U.S. equities, we remain biased toward large cap stocks at the expense of small cap stocks given the latter’s weaker profitability path and higher debt ratios; although small caps’ valuation discount should continue to provide some relative support. But let’s shift to the macro to start.

Manufacturing weightier than its economic weight

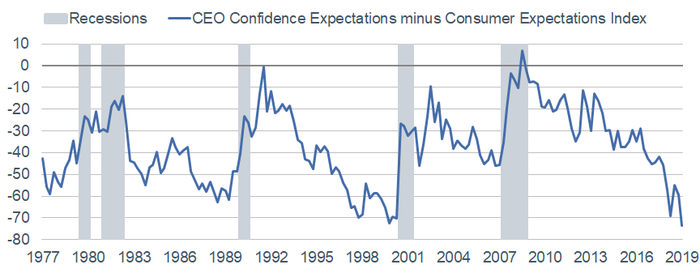

As we head into 2020, we will likely continue to focus on what to-date has been a fairly firm dividing line between the manufacturing/business investment side of the economy and the services/consumer spending side. The divide in confidence has been stark and could persist at least at the outset of 2020. CEOs’ forward-looking confidence is currently at levels last seen during the global financial crisis; while consumers’ expectations remain near historic highs. As you can see in the chart below, the spread between the two has rarely been wider historically—potentially warning of a recession (gray bars) as per history.

CEOs Morose … Consumers Optimistic

Source: Charles Schwab, Bloomberg, FactSet, The Conference Board, as of 9/30/2019.

Both manufacturing and business investment tend to punch above their weights in the economy as they are more cyclical and leading in nature. Historically, it’s via the labor market that the morphing of manufacturing/business investment into the broader economy has occurred. On that note, heading into 2020, so far so good.

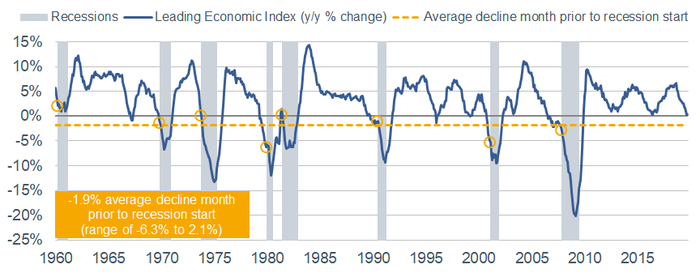

The labor market has significant momentum heading into the new year; with the unemployment rate (a lagging indicator) at a 50-year low; payrolls (a coincident indicator) growing at a robust pace; but unemployment claims (a leading indicator) recently ticking higher—albeit still at historically-low levels. Unemployment claims bear close scrutiny heading into 2020, as they typically carry signals for the future health of the labor market. In fact, they are one of the 10 components of The Conference Board’s Leading Economic Index (LEI), on which I keep a close eye.

The level of the LEI has been flattening over the past year; while the year-over-year rate of change has yet again dipped to the zero line, as you can see in the chart below. For now, this recent weakness is reminiscent of the two prior intra-cycle slowdowns—both of which had a manufacturing bent to them. But further weakness from here would likely elevate the risk of a broader contraction in the economy. Some good news may be coming from the rest of the world. Global LEIs have been leading U.S. LEIs since the eruption of the trade war in 2018; and they have recently stabilized. Further improvement outside the United States could lead—with a lag—to a stabilization in U.S. LEIs.

Third Slowdown in Leading Indicators

Source: Charles Schwab, Bloomberg, FactSet, The Conference Board, as of 10/31/2019.

Soft vs. hard data

The LEI has some soft data components within it. Soft data refers to survey/confidence-based economic readings; while hard data refers to quantifiable measures of economic output. In 2017 and 2018, it was a story of the soft data outperforming the hard data; while that began to reverse in 2020. The ongoing uncertainty regarding the trade war has been the culprit in bringing down confidence-based measures of economic growth—including the aforementioned weak CEO confidence, as well as the ISM manufacturing index (another leading indicator).

Deal lite or real deal?

Although a “Phase One” trade deal has been agreed to by the United States and China; it falls quite short of the initial U.S. goals of forcing China to morph its state-driven economy to a more open/fair economy. It does, for now, defer the tariffs that were set to go in effect on December 15, 2019. That’s good news as they targeted a mass of consumer-oriented goods. In addition, there was a partial roll-back of prior tariffs—with those having been imposed last September getting cut from 15% to 7.5%.

However, the “original” 25% tariffs on $250 billion of Chinese goods remain in place. China also agreed to increase its purchases of agricultural products to $40 billion, up from its current annual run rate of less than $10 billion (and the all-time peak of $29 billion). However, the product lists will not be publicly disclosed; meaning monitoring capabilities will be limited. Finally, China has promised to revise some laws and regulations on foreign investment and intellectual property (IP); but it doesn’t prevent China from continuing to “import” (aka, steal) U.S. IP through its powerful technology ecosystem.

The “deal” also doesn’t mean the Trump administration won’t continue to use tariffs and other trade barriers as a tool to coerce various concessions from, or to punish, other countries. This ongoing uncertainty is likely to keep a lid on corporate confidence—and in turn capital spending. Even with trade tensions somewhat reduced, corporate confidence will also likely remain muted in what is likely to be a very contentious election year. In fact, for the first time in 11 years, as per the ISM Manufacturing survey, U.S. manufacturers are expecting to reduce capital spending in 2020. The expected 2.1% decline follows a 6.4% increase in 2019.

Fed to the rescue?

Courtesy of monetary policy and financial conditions, 2019 was the mirror image of 2018. In 2018, although earnings growth skyrocketed thanks to corporate tax cuts, price/earnings (P/E) multiples contracted because of the weight of tighter monetary policy and financial conditions. But when the Fed moved to easing mode in 2019, financial conditions eased as well; allowing P/E multiples to expand—even without the benefit of any earnings growth in 2019.

The Federal Reserve’s three interest rate cuts in 2019 clearly supported asset markets, as well as interest-sensitive areas of the economy. The Fed currently expects to stay “on hold” in 2020; recently declaring that they have essentially set the bar higher for inflation to lead to rate increases; even if the tight labor market causes wage gains to accelerate. We do believe inflation could surprise marginally on the upside this year; which could be a cause of some market volatility.

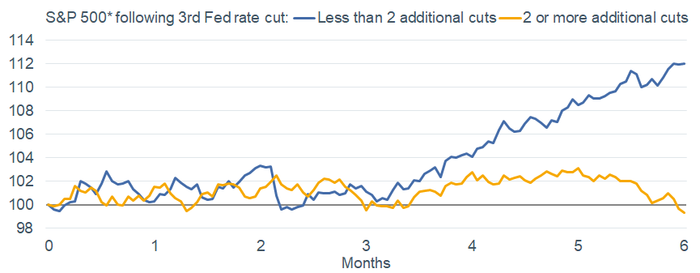

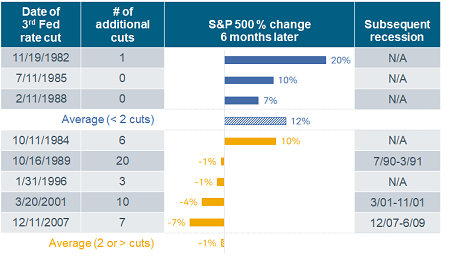

The chart below looks at the history of the stock market following the Fed’s third rate cut in a cycle. Interestingly, for those who are hoping the Fed reverts back to aggressive easing mode, history shows that during cycles when the Fed continued to cut aggressively (two or more additional times after the third cut), the stock market suffered relative to times when the Fed continued to cut less than two additional times. This should be intuitive given that a Fed that continued to cut rates aggressively was likely combating recessions.

3 + <2 = Good for Stocks

Source: Charles Schwab, Bloomberg. Past performance is no guarantee of future results, as of 12/16/2019. *Average S&P 500 price performance indexed to 100.

Earnings need to step up

So for now, the Fed’s position supports the intra-cycle slowdown thesis as well as the equity market. However, the tailwind behind P/E multiples may have run (most of) its course. Most valuation metrics—including P/Es—are stretched relative to history; and now likely require earnings growth to begin to do some of the market’s heavy-lifting. According to Refinitiv, S&P 500 earnings growth is expected to rebound back into double-digit territory by the second half of 2020; but estimates have been trending down for several months, and are likely to continue to do so.

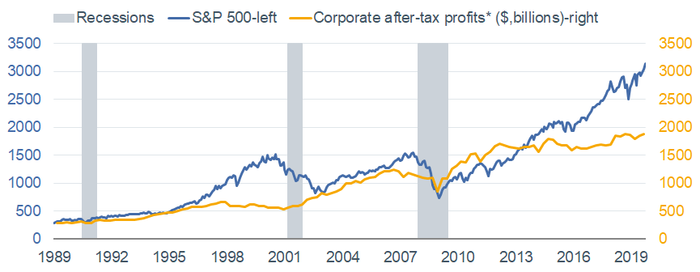

In particular, profit margins are under pressure courtesy of both tariffs as well as rising unit labor costs; not to mention the more secular weight of de-globalization. The chart below looks at a broad measure of corporate after-tax profits, which have flattened out; compared to the S&P 500 which has been on a tear over the past year. The historically-wide spread suggests either profits will eventually need to catch up to the market; or stocks may have to correct to move more in line with profits. At this point, I expect a combination of both for the coming year.

S&P Stretched Relative to Profits

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics. S&P 500 as of 11/30/2019. *Profits as of 9/30/2019 and with inventory valuation and capital consumption adjustments. Past performance is no guarantee of future results.

Sentiment says?

Until the U.S. stock market broke out to new highs at the end of October 2019, it had been in a trading range since January of 2018. Most of the peaks and troughs during that span were as much a function of investor sentiment extremes as any traditional market-related fundamentals. I would expect that to continue in 2020; with the possibility that a “melt-up” type environment could bring investor sentiment to extremely elevated levels.

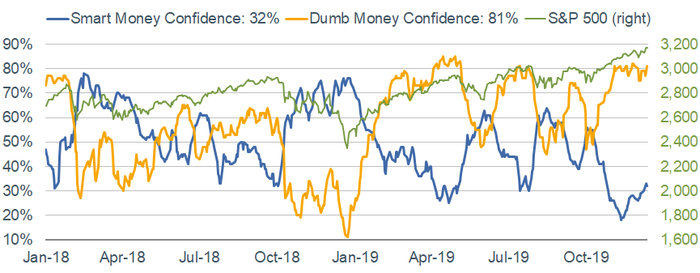

One set of sentiment measures on which I keep a close eye is SentimenTrader’s “Smart Money” and “Dumb Money” Confidence indexes. I like them because they are updated on a daily basis; and they are behavioral measures of sentiment—ST actually tracks what these cohorts are doing with their money—they are not measures of opinions.

Examples of some Smart Money indicators include the OEX put/call and open interest ratios, commercial hedger positions in the equity index futures, and the current relationship between stocks and bonds. Generally, investors have been rewarded by following the Smart Money traders when they reach an extreme. In contrast, investors have been rewarded by doing the opposite of what the Dumb Money is doing when they reach an extreme. Examples of some Dumb Money indicators include the equity-only put/call ratio, the flow into and out of the Rydex series of index mutual funds, and small speculators in the equity index futures contracts.

As you can see below, in December 2018—right at the point the market bottomed on Christmas Eve—the Smart Money was at an optimistic extreme and the Dumb Money was at a pessimistic extreme. That was a perfect setup for the huge rally that ensued. Since then, we have seen three extreme spreads with the opposite characteristics—Dumb Money at optimistic extremes vs. Smart Money at pessimistic extremes. In the prior two cases, the spread “called” the market weakness that ensued in both May and August of 2019. So far, the “Dumb Money” has been right given that stocks have remained in rally mode; but this is a spread on which I will be keeping an eye as we head into 2020.

Mind the Spread

Source: Charles Schwab, SentimenTrader.com, as of 12/13/2019.

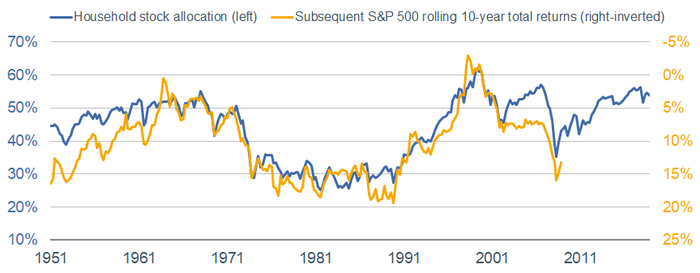

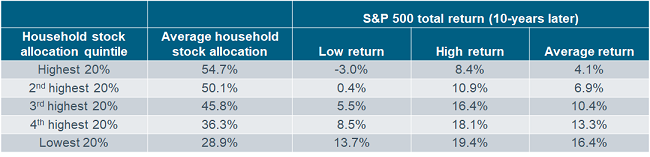

Finally, another longer-term measure of sentiment can be used to “forecast” longer-term returns for the stock market. U.S. households’ exposure to equities has historically been a factor in forward 10-year market returns. Clearly, when investors have limited excess firepower to buy stocks, future returns are more limited. Currently, U.S. households have nearly 54% of their assets exposed to stocks, which is in the highest quintile historically—the quintile with the lowest (albeit still positive) average subsequent 10-year return.

Households “Fully” Invested

Source: Source: Charles Schwab, FactSet, Copyright 2019 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/. As of 9/30/2019. Equity allocation (includes mutual funds and pension funds) is % of total equites, bonds and cash.

So, as we close the book on one decade and open the book on another, perhaps one message longer term for investors is to be wary of assuming the next 10 years looks as healthy as the past 10 years in terms of stock market performance.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

©2019 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

Read more commentaries by Charles Schwab