Merger arbitrage can create highly attractive returns. But there’s a big problem: hedge-fund managers typically take 30%–50% in fees. We advocate a smarter way to approach merger arbitrage investing, with much lower fees.

In merger arbitrage, arbitrageurs purchase a target company’s stock at a discount (or “spread”) to the merger consideration that’s being offered. If a merger closes as expected, the arbitrageur realizes the spread. If a merger falls through, large losses are possible. Over time, returns from merger arbitrage approaches have proved to be consistently attractive, with very high Sharpe ratios, shallow drawdowns and low correlations both with conventional assets and with style premia such as value, size, quality, momentum and low volatility. That makes merger arbitrage a strong portfolio diversifier.

So, merger arbitrage can be a valuable component of a well-structured portfolio. But do investors really need to lose so much of the returns in fees?

Merger Arbitrage Is a Risk Premium Not a Strategy

The answer to that question is rooted in the longstanding association with hedge funds. Many investors view merger arbitrage as a hedge-fund strategy and think the return streams depend on the unique skills of the hedgies in appraising each deal on a case-by-case basis. That’s why those investors have been prepared to share so much of the cake in fees.

But in our view, the core driver of returns is essentially a risk premium. For a variety of reasons, the stock price of a target company seldom trades in line with the offer price. It typically trades at a discount/spread. The spread value represents a risk premium—because it reflects the risk that the deal may fall through. In fact, it exists to compensate arbitrageurs for taking that risk. Over time, some deals will fall through, but many more will likely complete. And so, merger arbitrage is a way to profit from the risk premium generated routinely as part of the merger process. This common-sense insight is validated by a substantial body of academic research.*

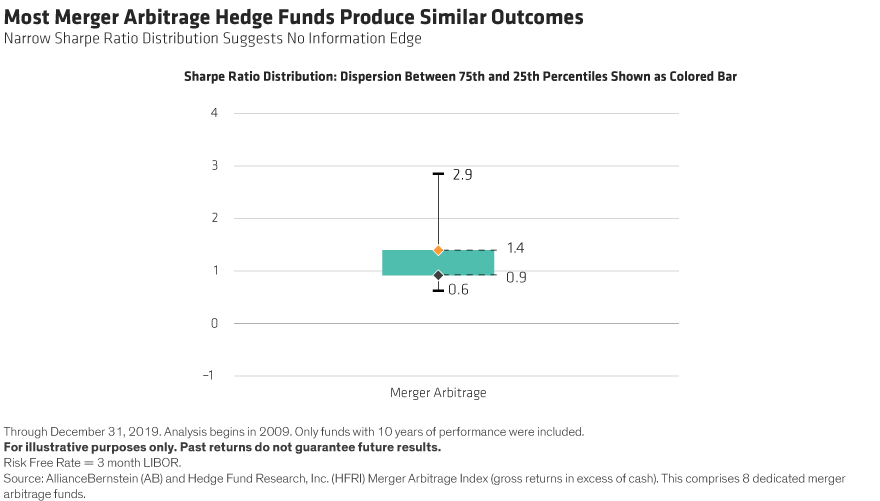

Because the core return stream from merger arbitrage results from a risk premium, it can be captured at relatively low cost through a well-researched systematic, rules-based strategy. Of course, by applying their unique skills and insights, the hedgies may be able to add value over and above that risk premium, and so justify their fees. Indeed, in the era before strict regulation and rapid news flow via digital technology, many were able to leverage an information advantage to generate superior returns. But in today’s markets, our research suggests that few managers can consistently add value (Display).

Two of our research findings illustrate why the principal driver of merger arbitrage returns is in fact the underlying risk premium.

1. Most manager outcomes are tightly bunched. The Sharpe ratio dispersion between the 75th and 25th percentiles is very low. That suggests most hedgies do not add value over and above the merger arbitrage risk premium by employing skills that are special or different. By contrast, some other Hedge Fund categories show wider dispersion, suggesting that specialist skill and insight may add value in strategies where the risk premium is less dominant.

2. Managers’ performance has been inconsistent. Every manager has endured worst-quartile calendar-year performance since 2012, and at least 75% of the managers have also achieved first-quartile calendar-year returns. This suggests it’s mean reversion that has mostly determined the pattern of hedgies’ returns.