Key Points

- As if the past two weeks weren’t enough, the market is “limit down” pre-open today.

- The economic implications of COVID-19, and now the crash in oil prices, are significant enough to make a recession likely.

- Stocks and bond yields have reconnected – both sending a dire message to monetary and fiscal authorities.

In the easiest of times (are they ever, really?) it’s futile to make predictions about the market with any semblance of accuracy. Clearly, these are not the easiest of times; so the futility is magnified. Even with non-stop coverage of COVID-19; with every question answered, there’s another question to ask. The human toll is immeasurable; but at this stage, so are the economic and market tolls. Ideally, we do look back and say some of the hysteria was overdone; but being prepared (and disciplined when it comes to investing) is unlikely to make things worse.

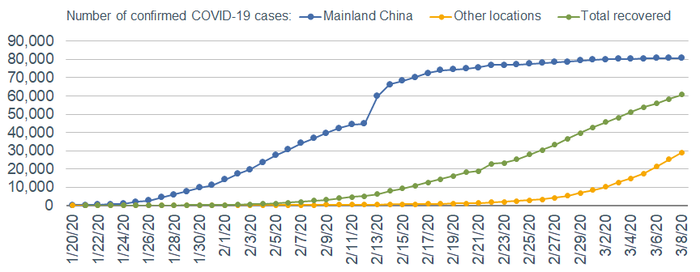

As most know, there is some reason for hope given the flattening out of the number of confirmed COVID-19 cases in Mainland China. There is also a still-sharp trajectory for the number of recoveries. The problem is that cases outside Mainland China have only recently begun to accelerate—with expectations of significant jumps to come in the United States once testing can be done more widely. In the meantime, markets are at the mercy of virus news—good and bad.

Yellow Line Needs to Stabilize

Source: Charles Schwab, Johns Hopkins’ Center for Systems Science and Engineering, as of 3/8/2020.

Manic week

To say today’s market open is treacherous would be an understatement. As I was putting this report to bed, S&P 500 futures were “limit down” (when trading curbs are triggered), meaning a drop at the open of at least 5%. Contributing to today’s renewed plunge is the 30% crash in oil prices courtesy of the disintegration of the OPEC+ alliance triggering an all-out price war between Russia and Saudi Arabia.

From a recent high of nearly $63 last April, WTI crude futures fell below $30 intraday this morning. This is likely to put increasing pressure on the credit markets given that energy companies are the largest issuers of junk bonds. In addition, more than 11% of the investment grade corporate bond market sits within the energy sector, with many companies rated BBB—the lowest rung. Increasing cash flow pressures are likely to result in downgrades, which would further weigh on junk debt.

Last week’s S&P 500 market action was a manic set-up to what we are seeing today:

- Monday +4.6%

- Tuesday -2.8%

- Wednesday +4.2%

- Thursday -3.4%

- Friday -1.7% (thanks to a +2.4% rally in the final hour of trading)

That of course followed a week with five straight declines—two of which were more than -3% and one which was nearly -4.5%. According to Bespoke Investment Group (BIG) we have only seen daily action like this over a two week span a few other times since the S&P 500’s inception in 1928. Aside from the multiple occurrences during the Great Depression era and a brief period around the Crash of ’87; it’s since only happened in late-2008 during the depths of the Global Financial Crisis (GFC) and again in August 2011 when U.S. debt was downgraded.

Fedication not what the doctor ordered

The Federal Reserve tried to play doctor with a surprise intermeeting interest rate cut of 50 basis points. The market has quickly built in expectations that the Fed is likely to move rates to the zero bound. But as we’ve been pointing out, although lower rates on the margin can aid the economy; they’re not the elixir for what ails us at present. Lower rates aren’t a vaccine. Lower rates can’t unclog the global supply chain. Lower rates can’t entice people to fly or cruise again. Lower rates can’t keep the virus from spreading or incidents of contraction or death from rising.

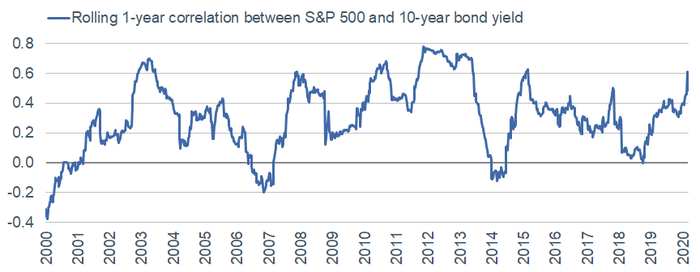

The bond market has certainly been sending a more ominous message; one that the stock market only recently began to heed. Alongside the plunge in stocks has been a plunge in longer-term interest rates. From a November 2019 high of 3.2%, the 10-year Treasury yield plunged to below 0.4% intraday this morning; with every duration on the yield curve out to 30 years below 1%. Stocks have reconnected to yields—most recently on the downside. As you can see in the one-year rolling correlation chart below, over the past year or so, the correlation has gone from nil to about 0.6 today (a positive correlation means they’re moving in the same direction).

Stocks Reconnecting to Bond Yields

Source: Charles Schwab, Bloomberg, as of 3/6/2020. Rolling 1-year correlation between weekly % change in S&P 500 and 10-year bond yields.

Since its all-time high on February 19, the S&P 500 is down 12.2%; with other major U.S. averages down a similar amount from their respective February all-time highs. The Russell 2000 index of small cap stocks has continued to fare worse, and is down 16.8% from its all-time high, which was in August 2018. But those are all returns before today.

Now that the S&P 500 and other major averages are down more than 10%, we’re “officially” in a correction. The day this report is being published—March 9—happens to mark the (ostensible) 11th anniversary of the bull market, which began on March 9, 2009. But before you don your celebration hat, keep in mind that if the current correction morphs into a bear market (defined as a drop of at least 20%), then the bull market will be marked as having ended last month (February 19 in the case of the S&P 500). That’s not a prediction, just a notation.

But speaking of the bull market, assuming it’s ongoing, the current correction is the seventh one since March 2009. Corrections during this bull market have lasted an average 78 calendar days and saw an average decline of nearly 15%. Looking longer-term (since 1990), BIG data shows the average correction has averaged a decline of 18.8% at the low, over an average span of 83 days.

Why so fast?

In addition to the speed with which the coronavirus escalated; there are two other reasons (in my opinion) why the market’s correction occurred with even greater speed and volatility. One is that investor sentiment had been stratospherically optimistic in January—a topic on which I wrote in late-January—suggesting vulnerability to the extent there was a negative catalyst (and boy, was there). Second is that the dominance of machine-driven trading (algorithmic- and quant-driven strategies) can exacerbate and momentum in both directions; as well as condensing time frames.

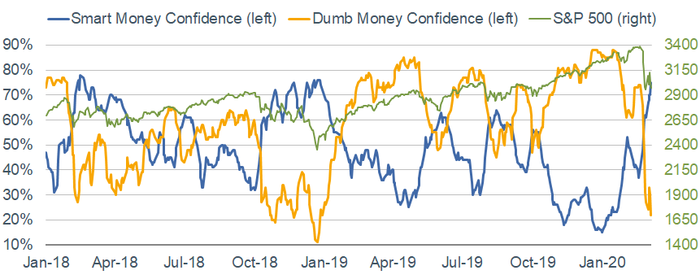

Let’s start with the sentiment angle. When I penned my “Virus: Could it be the Catalyst to Change Sentiment?” report on January 27, most measures of investor sentiment were showing extremely elevated optimism. One such pair of metrics I watch are tracked on a daily basis by SentimenTrader (ST). They are ST’s so-called “Smart Money” and “Dumb Money” confidence indexes; which are real-time gauges of how these cohorts are positioned (see the footnote for definitions of the cohorts). As one can surmise by the labels, the former tend to be the non-contrarian indicator, while it’s the opposite for the latter.

As you can see in the chart below, from an extended period of extreme optimism by the “dumb money” and equally extreme pessimism by the “smart money,” the correction over the past couple of weeks has led to a sharp reversal in positioning. Although not quite to the “perfectly-timed” extreme spread of December 2018, it’s sure getting close. Just as extreme optimism can establish vulnerability for a pullback or correction; extreme pessimism can establish opportunity for a reversal rally.

Smart Money Confidence on the Rise

Source: Charles Schwab, SentimenTrader, as of 3/6/2020. Confidence Indexes are measured on a scale of 0% to 100%. When Smart Money (long-term investors including large commercial hedgers and institutions) is at 100%, it means those most correct on market direction are 100% confident of a rising market. When it is at 0%, it means good market timers are 0% confident in a rally. Dumb Money (short-term speculators, inclusive of retail investors and odd-lot traders, who typically follow market trends) works in the opposite manner. Past performance is no guarantee of future results.

Options traders in particular have been in panic mode. According to ST, among the major equity index exchange traded funds (ETFs), options traders are paying record prices for puts relative to calls—likely driven by the smallest of options traders. As ST notes, this could be large traders who break up their orders into tiny lots; but more likely it’s been retail investors reacting emotionally to market moves. Last week, they spent more than $3 billion on put options—a record by a very large amount. [Caveat: they’ve been buying quite a few call options as well, so overall put/call ratios are not as extreme.]

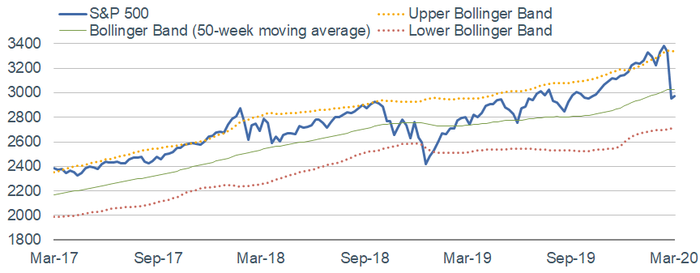

Also in my late-January report, I highlighted a technical indicator that looks at Bollinger Bands, which measures moves relative to standard deviations (see the footnote for a full definition). As you can see in the chart below, in late-January, the S&P 500 was stretched to the extreme above its Upper Bollinger Band. Since the correction unfolded, the index has made some headway south; but still has a ways to go before hitting the kind of downside extreme seen most recently in December 2018.

Stocks Reversing from Technical Extreme

Source: Charles Schwab, Bloomberg, as of 3/6/2020. For more info information on Bollinger Bands®, see Bollinger Bands®: What They Are, and How to Use Them.

Rise of the machines

Trading desks across the spectrum of institutional investors, hedge funds, and some wirehouse brokerage firms often use computer-driven algorithms routinely—which are complex equations and triggers used to make decisions programmatically. They are often added to the mix of high-frequency traders (HFTs) and “quants” when blame is placed for periods of spiking volatility. Algorithmic or quant-based trading can kick in when there are any number of triggers hit—including most likely levels of the volatility index (VIX), certain technical thresholds, index moving average crosses; and possibly even specific words uttered by the likes of Federal Reserve officials. (I have no particular knowledge of these triggers … those are simply possible examples.)

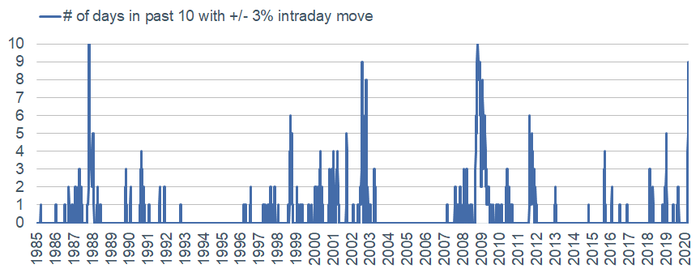

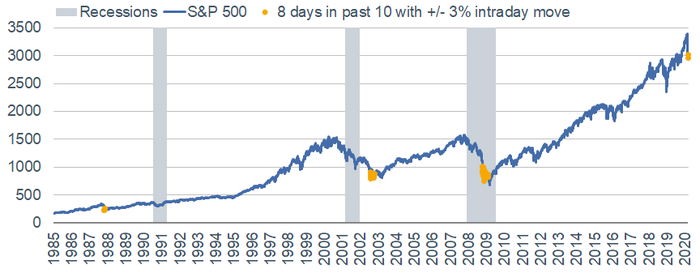

This “rise of the machines” likely leads to larger moves in either direction than the fundamentals may dictate—including intraday moves. The chart below shows the number of days in the prior 10 day period with +/- 3% intraday moves. As you can see, the recent spike has only been seen three times over the past 35 years—during the GFC, coming out of the 2000-2002 tech bust and in the aftermath of the Crash of ’87. You can see the corresponding yellow dots on the S&P 500 chart over the same span. In the case of the first two prior experiences, the market was near its bottom; but in the case of 2008, there was still a bit more pain ahead.

Spike in Large Intraday Moves

Source: Charles Schwab, Bloomberg, as of 3/6/2020.

What about the “fundamentals?”

As noted, the latest wild volatility isn’t necessarily connected to the change in the fundamental picture on a day-to-day basis. The rub with the current picture is multi-fold and stems from the unique uncertainty with which we are all faced in terms of the impact of COVID-19. Economists don’t quite know what to do with GDP forecasts; and analysts and strategists don’t know quite what to do with earnings estimates. In the case of the latter, it makes valuation analysis extremely difficult.

We do know that stocks have become “cheaper” with the major averages down at least 12%. The problem is that it’s not just the “P” in the P/E that’s falling—it’s the “E” as well. When both the numerator and denominator are plunging, good luck assessing valuations. Many of the most hard-hit companies—a plurality of which are in the travel/hospitality/leisure industries—have simply “cancelled guidance” to Wall Street analysts—starkly different than the typical upward or downward guidance companies provide. Published estimates are still too high; but how far they still have to fall is anyone’s guess. At least one firm—Goldman Sachs, who publishes their own aggregate S&P 500 earnings estimates—has brought their estimate to zero growth for the full year.

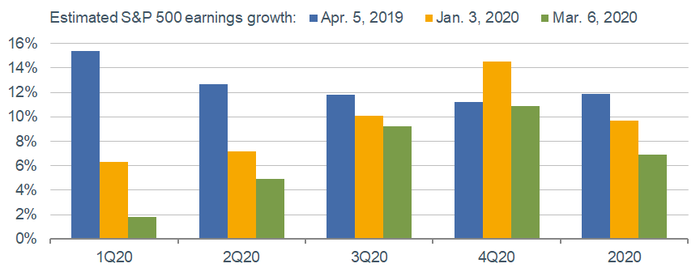

As you can see in the chart below, from when consensus estimates were first tabulated by Refinitiv a year ago, estimates for the first three quarters and full-year 2020 have been in descent. There are more cuts coming for sure; most notably for the energy sector. Does anyone think the S&P 500 energy sector will see 17-18% earnings growth in this year’s second half (which is the current consensus)? No way.

More Cuts to EPS Growth Coming

Source: Charles Schwab, I/B/E/S data from Refinitiv, as of 3/6/2020.

Also hurt will be U.S. companies that generate a large portion of their sales from China. Evercore ISI conducts widely-watched weekly company surveys, and as you can see in the chart below, the recent plunge takes their Survey of China Sales to the lowest level in the survey’s history.

Grim Look at Sales to China

Source: Charles Schwab, Evercore ISI as of 3/6/2020. Evercore ISI's Company Survey of China Sales is comprised of large U.S.- and global-based firms with both foreign and U.S. sales. The survey is a weekly series and is based on a scale of 0 to 100 where readings closer to 0 indicate weaker sales and those closer to 100 indicate stronger sales.

No more bifurcation?

For the past year or so, we have been writing about the bifurcation in the U.S. economy. Whether divided by manufacturing vs. services; or business investment vs. consumer spending; the former have been in recession, while the latter have remained in healthy shape. Unfortunately, COVID-19 likely means a significant delay in the hoped-for recovery in manufacturing and/or business investment; and means a likely significant hit to services and consumer confidence/spending in the near term. Think about the areas we’re already seeing a change in behavior: travel, schools, sporting events, shopping centers, restaurants, corporate conferences … as well as the rapid growth of interest in telecommuting and virtual meetings. It’s a no-brainer that our consumer/services-oriented economy will take a hit.

The good news is that we came into COVID-19’s wake with a decent amount of economic momentum—certainly in terms of the labor market, as Friday’s robust jobs report will attest. The rub is that most of the data within that report is only through February 12; so it doesn’t yet show the impact of the virus on the economy. Sadly, the days (at least near-term) of better-than-expected economic data are a thing of the past.

What to do … or not to do

In the meantime, our advice to investors hasn’t changed. For the past couple of years—given our perspective that we were entering the latter stages of the cycle—we have been pounding the table on diversification (across and within asset classes) as well as periodic/systematic rebalancing. Those tried-and-true disciplines are the closest thing an investor can get to a “free lunch” in this crazy business.

Perhaps most important is that investors heed our age-old warnings:

- Neither “get in” nor “get out” are investment strategies … they represent gambling on moments in time; when investing should ALWAYS be a process over time.

- Panic is not an investment strategy.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

©2019 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

More Alternative Investments Topics >