Key Points

-

At the March lows, stocks were discounting the kind of economic collapse we’re currently in the midst of; but the subsequent rally is less about economic optimism, and more about Fed-provided liquidity.

-

The stock market’s V-shaped rebound is unlikely to be matched by a V-shaped economic rebound.

-

Longer-term, we will likely see the U.S. economy shift from consumption-driven to investment-driven.

The speed with which the U.S. stock market went from all-time highs to deep bear market territory broke all historical records. Then the rally that ensued was one of the fastest “new bull markets” ever in history; allowing the month of April to be the strongest since early-1987. Given the weaker start to the current month, expect to hear louder chants of “sell in May and go away.”

The warp speed nature of the past few months is unprecedented in many ways—both in terms of the economy and the stock market. The speed of the stock market’s collapse was directly tied to the collapse now underway in the economy. But what of the speed with which stocks retraced more than 60% of the collapse? In a phrase (coined by my first boss, the late-great Marty Zweig), “don’t fight the Fed.”

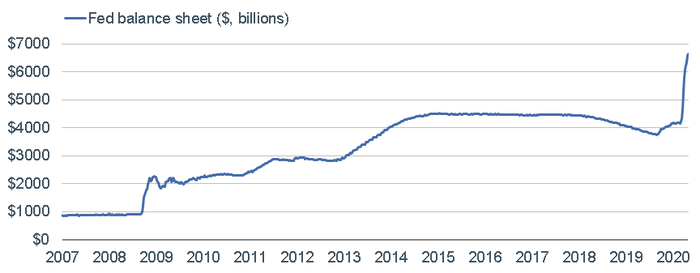

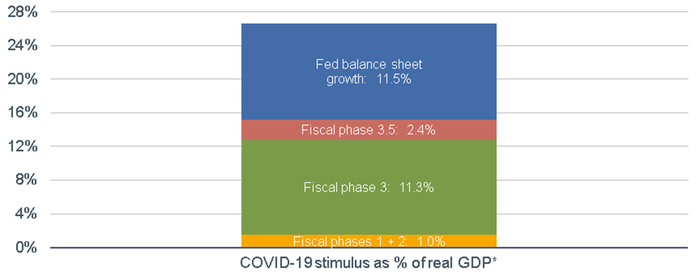

The Federal Reserve’s balance sheet has ballooned to about $6.7 trillion (see first chart below); as part of an unprecedented (there’s that word again) set of actions to save the economy during the COVID-19 crisis. Adding the relief packages from Congress and the Treasury Department, the combination of monetary and fiscal stimulus has reached more than 26% of expected 2020 GDP (see second chart below).

Fed’s Balance Sheet Goes Parabolic

Source: Charles Schwab, Bloomberg, as of 4/29/2020.

Fiscal Plus Monetary Stimulus

Source: Charles Schwab, as of 4/29/2020. *Real GDP based on CBO (Congressional Budget Office) economic projections for 2020. Phase 1 provides funding for vaccine, therapeutic, and diagnostic development; Phase 2 provides grants for unemployment insurance, a 6.2% increase in Federal Medical Assistance Percentage (FMAP) for Medicaid, and refundable tax credits for paid medical and sick leave; Phase 3 establishes the Paycheck Protection Program (PPP); Phase 3.5 provides enhancements for the PPP and additional health care enhancements.

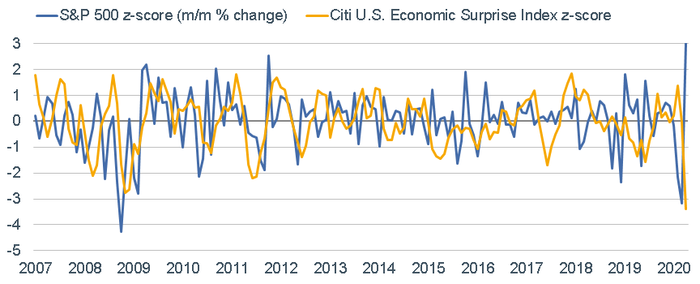

It appears the “Fed put” was alive and well in April—a period during which the spread between how stocks were performing and how the economy was performing hit a record. As you can see in the chart below, the z-scores (representing standard deviations from the mean) for the S&P 500 and Citi’s U.S. Economic Surprise Index have moved dramatically in opposite directions.

Extreme Divergence Between Stocks and Economy

Source: Charles Schwab, Bloomberg, as of 4/30/2020. A Z-score measures a value's relationship to the mean (average) of a group of values, measured in terms of standard deviations from the mean.

Fed to rescue?

As we’ve been pointing out, the Fed’s actions may be sufficient to keep the economic crisis from becoming a financial system crisis; but this is at its core a health crisis, for which the Fed has no direct tools. The stock market’s rally has been fueled by Fed-provided liquidity, but the 62% retracement between March 23 and April 29 suggests stocks were pricing in a V-shaped recovery in the economy. That is unlikely. The damage being done—notably within the labor market—will test optimists’ wont to look through the valley of this crisis.

Epic collapse

Embedded in the economic surprise index above has been a rash of recent economic data points that have rewritten the “rules” around how the economy moves from expansion to recession. Most recently, ISM released its manufacturing index, which was actually a positive surprise … for the “wrong” reason. The headline number was slightly better than expectations. However, the headline was boosted by the supplier deliveries component, which jumped to the highest reading in 46 years. Looking under the hood reveals reality: the production index hit a record low, indicating that weak deliveries reflect supply chain interruptions, not high demand. In addition, the new orders component collapsed to Global Financial Crisis (GFC)-era levels—which is a direct warning of a coming plunge in corporate profits. That was followed today by the worst-ever decline in factory orders.

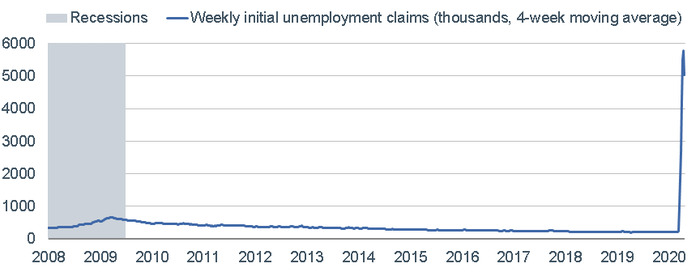

Unemployment claims—a key leading indicator—also continue their epic ascent on a cumulative weekly basis. Now that we have more than a month’s worth of COVID-19 hits to the labor market, the four-week moving average is a key indicator to watch. It’s one of those charts that if you showed it to me at the start of this year, I wouldn’t have believed it.

Unemployment Claims Go Parabolic

Source: Charles Schwab, Bloomberg, as of 4/25/2020.

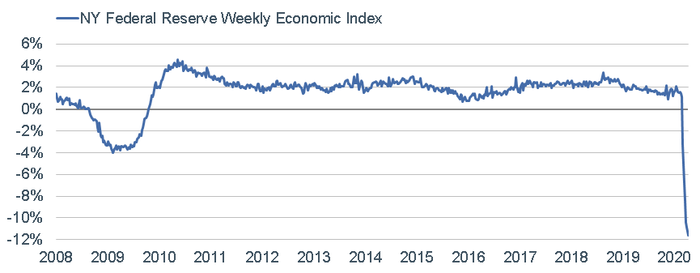

Woe is WEI

Claims are not only a long-standing component of The Conference Board’s Leading Economic Index (LEI); but they are also a component of the NY Fed’s newly-created Weekly Economic Index (WEI), as you can see in the table below. The chart that follows shows the continued plunge in the WEI—it’s now well below even the worst phase of the GFC. This will be a key indicator to watch for an eventual stabilization given the high-frequency and virus-relevant nature of the WEI’s components.

Source: Federal Reserve Bank of New York.

Source: Charles Schwab, Bloomberg, as of 4/25/2020. Daniel Lewis, Karel Mertens, and Jim Stock, “Monitoring Real Activity in Real Time: The Weekly Economic Index,” Federal Reserve Bank of New York Liberty Street Economics.

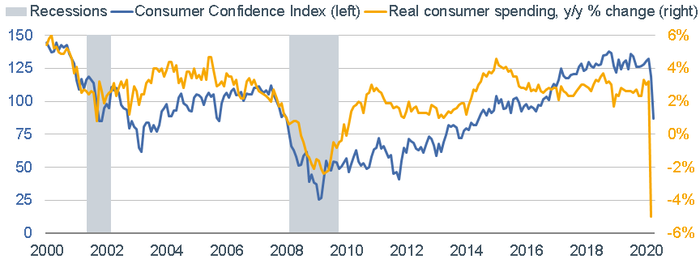

What they do is more important than what they say

I showed the dichotomy between the stock market and economic surprise data above. There are also some notable dichotomies within economic and market statistics. Let’s start with consumer confidence vs. consumer spending. As you can see in the chart below, the decline in consumer confidence has been significantly more muted than the plunge in real consumer spending. This likely reflects the reality of the current economic situation; but the “hope” for a quick recovery.

Consumers’ Actions Weaker Than Their Words

Source: Charles Schwab, Bloomberg, Bureau of Economic Analysis (BEA), The Conference Board. Consumer Confidence as of 4/30/2020. Consumer spending as of 3/31/2020.

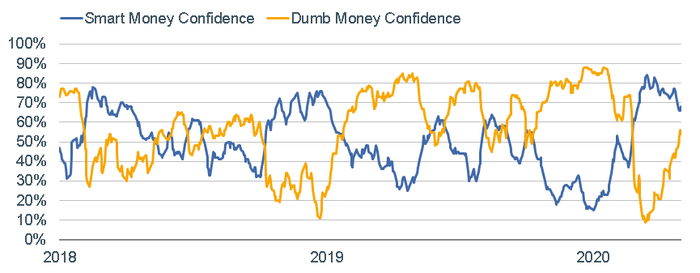

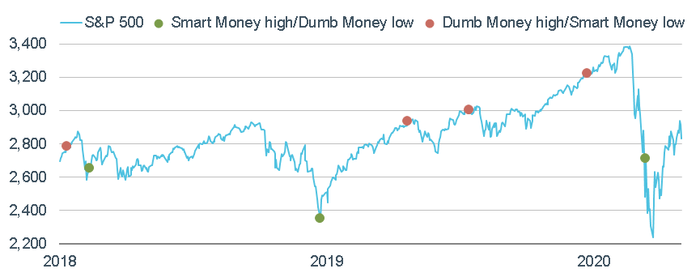

In terms of stock market confidence, there has also been a divergence in what investors are saying vs. what they are doing. The first chart below shows a pair of indicators that I show quite often. They are SentimenTrader’s “Smart Money and Dumb Money Confidence Indexes” and are real money gauges (not opinion surveys) of what the “good” market timers are doing with their money compared to what “bad” market timers are doing. As you can see, the “dumb money” has been positioning much more bullishly since the market’s March 23 low (at which point they were at an ill-timed extreme bearish position).

“Dumb Money” Optimism Surging

Source: Charles Schwab, Bloomberg, SentimenTrader, as of 5/1/2020. Confidence Indexes are measured on a scale of 0% to 100%. When Smart Money (long-term investors including large commercial hedgers and institutions) is at 100%, it means those most correct on market direction are 100% confident of a rising market. When it is at 0%, it means good market timers are 0% confident in a rally. Dumb Money (short-term speculators, inclusive of retail investors and odd-lot traders, who typically follow market trends) works in the opposite manner. Past performance is no guarantee of future results.

On the S&P 500 chart below, I put red dots at the points on the chart above when the “dumb money” was extremely bullishly positioned and the “smart money” was at the opposite extreme. I put green dots at the points when it was the “smart money” that was extremely bullishly positioned and the “dumb money” was at the opposite extreme. Although not a perfect indicator by any means, the red dots tended to be at or near short-term market peaks; while the green dots were followed by rallies. A caveat is the most recent period of market volatility. The “dumb money” was right for a while—coming into this year more bullishly-positioned than the “smart money;” while the “smart money” positioned itself bullishly in advance of the final leg down to the March 23 low. The two are beginning to converge and would represent a risk if they continue to reach opposite extremes again.

“Smart Money” Tends to be Smarter

Source: Charles Schwab, Bloomberg, SentimenTrader, as of 5/1/2020. Past performance is no guarantee of future results.

In contrast to the more bullish outlook being expressed by the “dumb money” and the still fairly bullish positioning of the “smart money,” investor sentiment in opinion surveys is significantly more subdued. The American Association of Individual Investors (AAII) does a weekly survey of its members; and its latest readings were less than 31% bulls and more than 44% bears (about 25% are neutral). So, from an investor perspective, unlike consumer confidence vs. consumer spending, investors are saying they’re more bearish, but acting more bullish.

Narrow

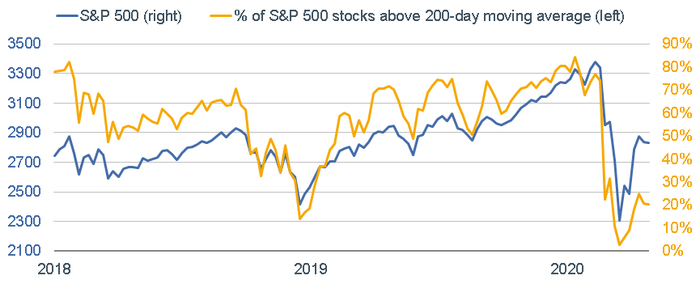

Looking under the hood of the sharp rally off the March 23 low, neither measures of market breadth nor leadership trends are indicative of a healthy advance. As you can see in the chart below, the percentage of S&P 500 stocks trading above their 200-day moving average remain extremely low at only 20%. That is significantly lower than 70-80% at this point last year (when the S&P was at about the same level as today). You can also see the difference between the move off the December 2018 low and the move off the March 2020 low—in the case of the former, breadth improved even more rapidly than stocks, which is clearly not the case this time.

Not All Stocks Participating in Rally

Source: Charles Schwab, Bloomberg, as of 5/1/2020. Past performance is no guarantee of future results.

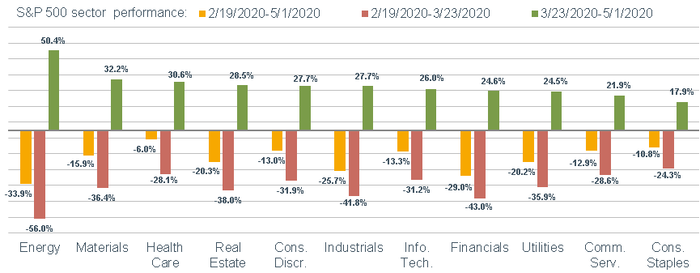

Sector leadership trends also suggest skepticism about the health of the rally is warranted. As you can see in the chart below, the best-performing sector (by far) since the March 23 low has been energy, which is up 50%, after a -56% plunge when the bear was roaring. That reversal smacks of speculative extremes in both directions vs. a sign of a stronger economy on the horizon.

Sector Leadership Does a 180

Source: Charles Schwab, Bloomberg, as of 5/1/2020. Past performance is no guarantee of future results.

None of the aforementioned concerns suggest the stock market is on its way to retesting its March low. I have no idea whether that’s likely—it would probably happen only if the data for the economy and/or the virus itself significantly disappoints relative to current expectations. But I would expect continued bouts of volatility.

Green shoots

I’ll end with an attempt to shed a more positive light on the situation. The damage being done to our economy will be unlike anything most of us have experienced in our lifetimes. But, as has been the case historically, when we come out of the depths of this recession, there will be new engines for growth. As highlighted in an interesting report from our friends at Cornerstone Macro, we are likely transitioning to an economy that will be less dependent on consumers, and more dependent on investments—from housing to manufacturing; from low tech to high tech; from offshoring to onshoring; and health care of course.

Since the early-1980s, the U.S. economy has been highly-consumer spending-driven. But that wasn’t always the case. From the WWII era up until the 1980s began, the make-up of the economy was quite different than it’s been over the past four decades:

- From 1943-1979, total investment as a percentage of U.S. gross domestic product (GDP) rose from about 4% to nearly 20% (including both capital spending and housing).

- From 1943-1980, capital spending as a percentage of GDP rose from about 3% to 15%.

- From 1944-1980, housing’s share of GDP rose from 1% to nearly 6% (popping to as high as 7% coming out of WWII).

- From 1944-1979, consumer spending rose from 49% to 60% of GDP; but total investment rose faster than consumption, increasing from 8% of consumption to 33% of consumption.

There are other factors that will likely lead to a shift toward investment over consumption, including China’s descent and the United States’ ascent as a cost-effective place for business investment. This adjustment won’t happen overnight, but it’s something we can put in our back pocket to look forward to down the road.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Commodity-related products, including futures, carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions, regardless of the length of time shares are held.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

©2020 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

(0520-0D1P)

© Charles Schwab

More Volatility/Downside Protection Topics >