Key Points

-

Visual look at the latest trends and statistics across the spectrum of the economy, policy and the stock market.

-

Stocks’ rally off the lows is not inconsistent with historical trends; albeit at warp speed.

-

Emphasis on quality is likely to continue to lead the performance derby.

On a day that started with good news on an experimental COVID-19 vaccine, with the stock market showing strong early gains, today’s report is more visual and less wordy than normal. Since I know not every reader of these publications follows me on Twitter—where I’m constantly posting charts, tables and data that I find compelling—this report has a sampling of what has recently caught my eye (and some bright spots). It combines economic, monetary and market data (in that order), while also a connecting of the dots between the economy and the stock market.

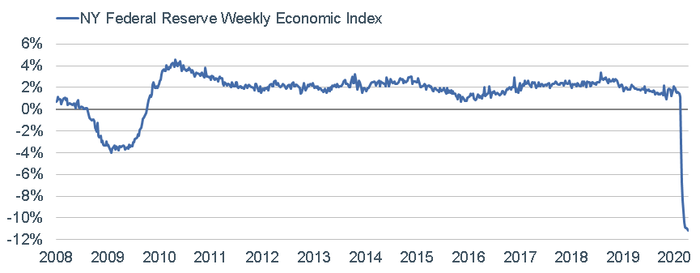

Let’s start with the “Weekly Economic Index” (WEI) created in March by the Federal Reserve Bank of New York. It encompasses 10 high-frequency and timely components, and is a good broad assessment of the hit to the economy. As you can see, “hit” is an understatement as the index has plunged through even the worst levels of the 2008 Global Financial Crisis (GFC).

Woe is WEI

Source: Charles Schwab, Bloomberg, as of 5/9/2020. Daniel Lewis, Karel Mertens, and Jim Stock, “Monitoring Real Activity in Real Time: The Weekly Economic Index,” Federal Reserve Bank of New York Liberty Street Economics.

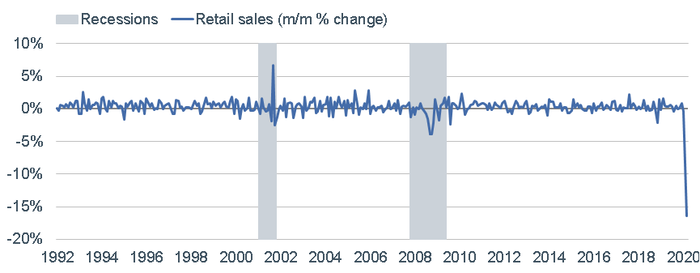

Retail sales were also eye-popping, with a -16.4% plunge in April. Sales in most categories fell more in April than March; with traditional retail and leisure spending hit hardest—including an epic 90% implosion in clothing store sales. Even categories that held up well in March were hit, including grocery and healthy/personal care stores (grocery stores are still up 10% since February). There was some positive news as online retail sales were up 8.4% in April.

Retail Sales Implode

Source: Charles Schwab, U.S. Census Bureau, Bloomberg, as of 4/30/2020.

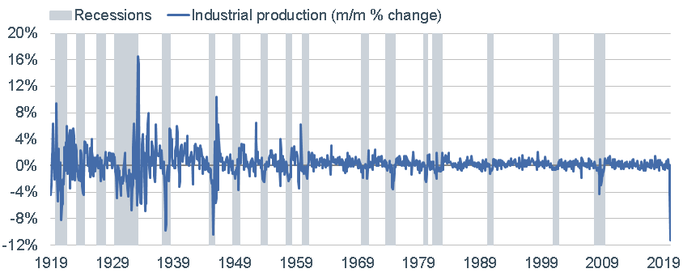

Of course it’s not just the consumer side of the economy suffering, with an 11.2% drop in industrial production in April. That was the largest decline in the index’s 100-year history (including the Great Depression and WWII). The decline was led by a 13.7% drop in manufacturing output, which plunged to its lowest level since mid-2009; and a drop to 61.1% in capacity utilization (a post-WWII record low).

Industrial Production’s Record Drop

Source: Charles Schwab, Federal Reserve, Bloomberg, as of 4/30/2020.

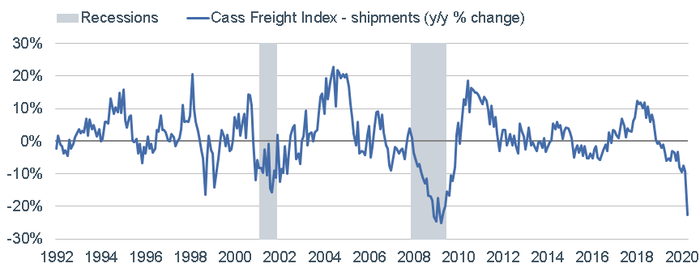

In keeping with the weak industrial/manufacturing side of the economy, the Cass Freight Index measures the number of intra-continental shipments across North America, and it has plunged to the lowest level since the GFC.

Cass Freight

Source: Charles Schwab, Bloomberg, as of 4/30/2020. The Cass shipments index is a measure of the number of intra-continental freight shipments across North America, for everything from raw materials to finished goods.

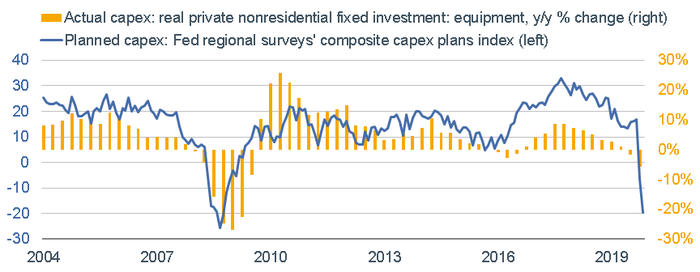

Capital spending (capex) was already under pressure in the past year due to the trade war and impact of tariffs that U.S. companies have been paying on imported goods from China. The impact of COVID-19 on planned capex has been particularly swift, and points to even more weakness to come in longer-term corporate investment.

Planned Capex Sinks

Source: Charles Schwab, Bloomberg, Bureau of Economic Analysis, Federal Reserve Banks of Dallas, Kansas City, New York, Philadelphia and Richmond, Strategas Securities, LLC. Actual capex as of 3/31/2020. Planned capex as of 4/30/2020.

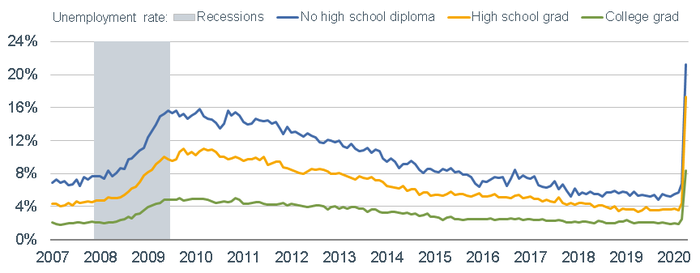

The impact on employment has been well-documented, including the spike in the unemployment rate to 14.7%—which is inevitably heading higher. Education level is having an outsized impact on the rate, with a surge in unemployment among those without a high school diploma to more than 20% (while it’s “only” a little more than 8% for those with college degrees).

Unemployment Rate by Education Level

Source: Charles Schwab, Bloomberg, as of 4/30/2020.

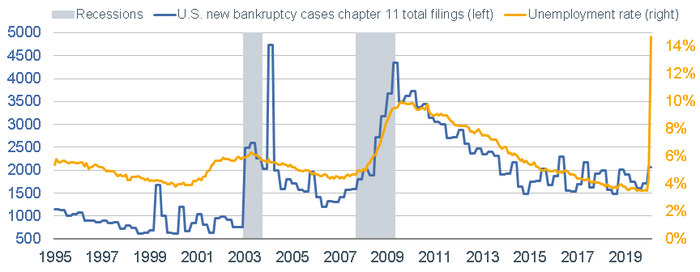

The spike in the unemployment rate bodes ill for the expected coming increase in new bankruptcy filings by U.S. companies, based on a historical comparison.

Unemployment Rate vs. Bankruptcies

Source: Charles Schwab, Administrative Office of U.S. Courts, Bureau of Labor Statistics, as of 4/30/2020.

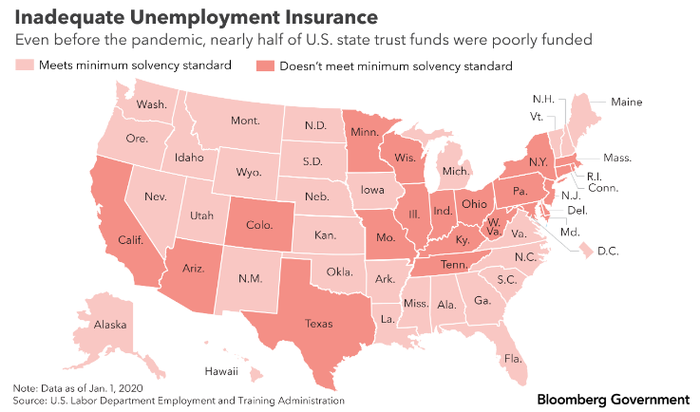

The unemployment rate—typically a lagging indicator—has obviously been pushed higher by the cumulative increase of more than 36 million filings for unemployment insurance. This will continue to have an impact on individual states’ financial health. Even before the COVID-19 pandemic, 40% of states’ trust funds were poorly-funded; and it’s expected to get worse from here.

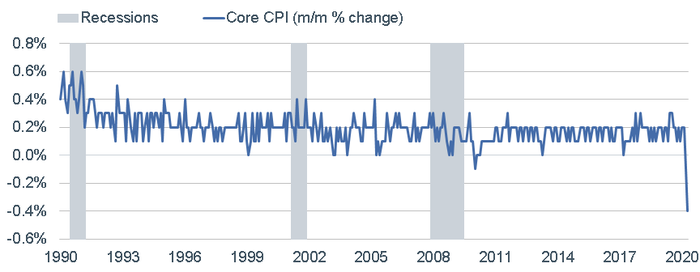

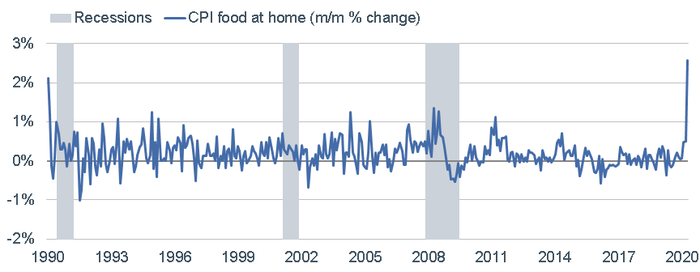

The shutdown of the economy has compressed both the demand and supply sides of the economy; which has also had an impact on inflation. The latest consumer inflation statistics were quite weak—although not across-the-board (more on inflation—or the lack thereof below). Core (excluding food and energy) consumer price index (CPI) inflation sunk in April. About the only category within overall headline inflation that was up was, not surprisingly, “food at home.”

Core CPI Inflation Plunges with Notable Exception

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics (BLS), as of 4/30/2020.

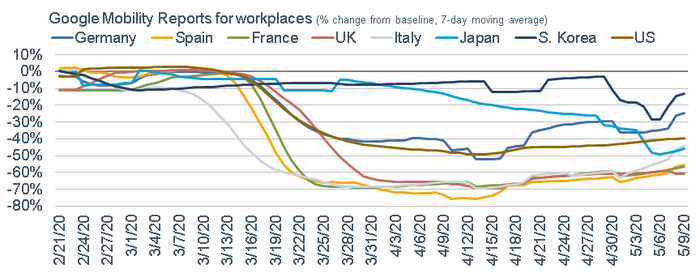

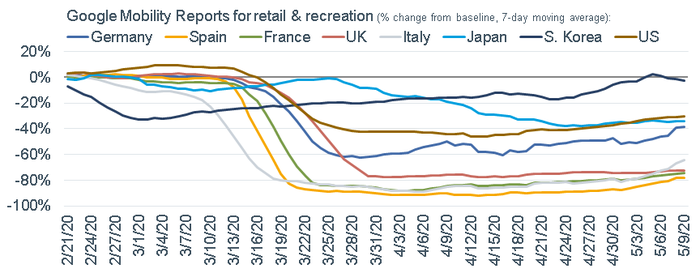

There are a number of newer economic metrics I’ve been tracking that should give us a real-time look at the trajectory of higher-frequency economic data as the U.S. economy is in the process of opening back up. Google puts together “mobility reports” (tracking movement trends over time), and in today’s environment, they’re particularly useful for tracking what’s going on in workplaces in general—and retail/recreation specifically. Globally, they have begun to trend higher—with the United States having compressed less than many European countries; but still lagging the improvement in places like South Korea.

Google Global Mobility Trends

Source: Charles Schwab, Google LLC "Google COVID-19 Community Mobility Reports" https://www.google.com/covid19/mobility/, as of 5/9/2020. Google Mobility Reports chart movement trends over time by geography, across different categories of places such as workplaces and retail and recreation.

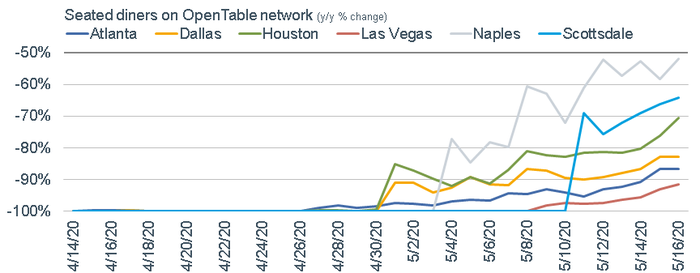

I noted the spike in inflation for food-at-home—which has obviously been a beneficiary of the closure of restaurants for dining in across the country. Now that restaurants are in the process of opening (with limited capacity), we can keep an eye on OpenTable “seated diners” statistics across metropolitan areas). One of the largest improvements off the low (which was -100% across nearly all of the country) has occurred in my new home city of Naples, FL; followed by another “hot spot” in Scottsdale. Even within states, there are differences (Houston has recovered a bit more than Dallas).

Dining Out Picking Up Regionally

Source: Charles Schwab, OpenTable, as of 5/16/2020.

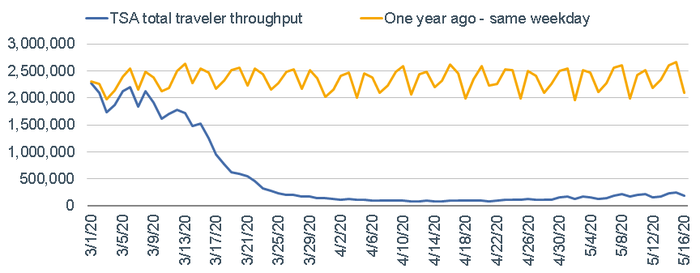

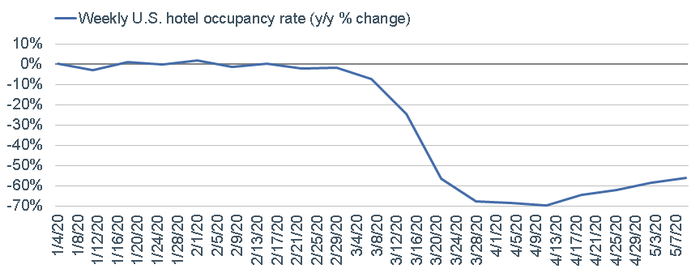

Although people are beginning to venture out to restaurants, they’ve been more hesitant to book a flight and/or stay at a hotel. The Transportation Security Administration (TSA) tracks total traveler throughput and it’s barely registering a pulse; although there has been a mild improvement in the hotel occupancy rate. Travel—both leisure and business—is likely to take more time to start to recover given the notable difference between daring to venture out to your local establishments vs. making the commitment to take a trip.

Not Much Flying Still

Source: Charles Schwab, Transportation Security Administration (TSA), as of 5/16/2020.

Hotel Occupancy Off Lows

Source: Charles Schwab, STR, as of 5/9/2020.

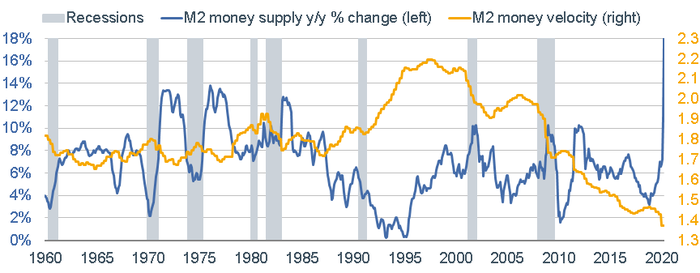

We’ve written extensively on the record-breaking relief/liquidity/lending programs instituted by both U.S. monetary and fiscal authorities. In total, they equate to more than 25% of 2020’s real gross domestic product (as estimated by the Congressional Budget Office). This has resulted in a record-breaking spike in M2 money supply (cash, checking deposits, money market securities, mutual funds and other time deposits.)

We are consistently asked why this spike in money supply hasn’t (or won’t) lead to a commensurate spike in inflation. There is also money “velocity” that needs to be considered—measuring whether the money being pumped into the financial system and/or households’ hands is moving into the economy (via borrowing, investing, spending, etc.). Although money supply has spiked, the velocity of money has imploded.

M2 Money Supply vs. Velocity

Source: Charles Schwab, Bloomberg, Federal Reserve, as of 4/30/2020. The velocity of money is the number of times one dollar is spent to buy goods and services per unit of time. If the velocity is increasing, then more transactions are occurring between individuals in an economy.

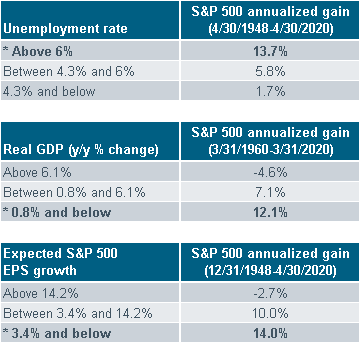

The stock market appears to many to have rallied off its March low in complete ignorance of the breathtaking decline in economic activity. Although there is no precedent for the nature/speed/magnitude of this health and economic crisis, there is a look at history that can provide some understanding of the relationship between the stock market and economic data.

Remember, the stock market is a leading indicator—typically starting its move into a bear market in advance of the economy entering a recession; and typically starting its move into a bull market in advance of the economy exiting a recession. Although the latest moves have occurred at warp speed, history shows that the stock market has actually had its best performance in the highest zone of the unemployment rate, the weakest zone of real GDP and the weakest zone of S&P 500 earnings growth.

* Indicates current range. Source: Charles Schwab, ©Copyright 2020 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/.

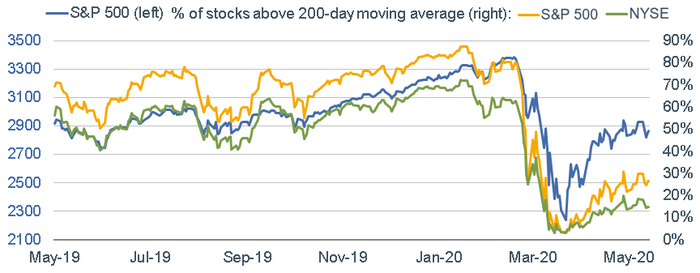

The stock market’s rally off the March lows is not as healthy as a cursory look at the major index’s levels would suggest. The S&P 500 has recovered more than 60% of its move from an all-time high on February 19 to a decline of 34% as of March 23. However, a much smaller share of its component stocks are trading above their 200-day moving averages (and an even lower percentage of the broader New York Stock Exchange stocks). This points to the relative “narrowness” of the market’s advance—not a healthy technical condition.

Narrow Market Advance

Source: Charles Schwab, Bloomberg, as of 5/13/2020.

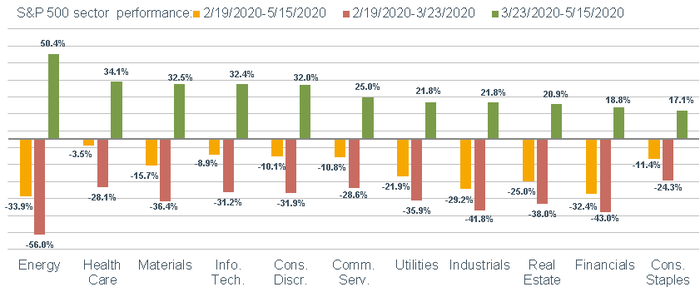

The market’s advance—in addition to being narrow in breadth—has also shown leadership that is more about a “reversion trade” than a sign of improving economic conditions to come near-term. Energy is the leading sector; after having been the worst performer during the initial bear market move; while financials, which typically rally alongside other cyclical sectors when the economy is recovering, are the most lagging of all sectors.

Sector Performance: Reversion Trade

Source: Charles Schwab, Bloomberg, as of 5/15/2020. Past performance is no guarantee of future results.

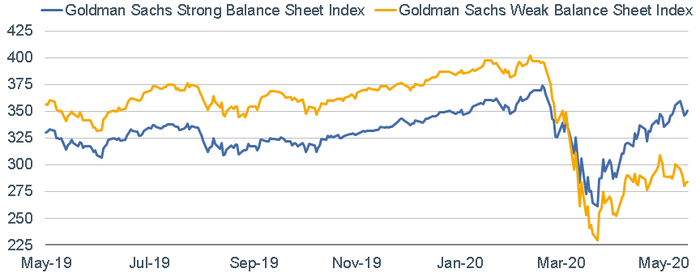

We continue to suggest that “factors” are likely (and have been) more important in defining leadership than sectors—with quality among the most important factors to consider when picking stocks. Goldman Sachs recently created “strong balance sheet” and “weak balance sheet” baskets of stocks; with the former significantly outperforming the latter. [The usual caveat of past performance is no guarantee of future results applies here.]

Strong Balance Sheets Rule

Source: Charles Schwab, Goldman Sachs, Bloomberg, as of 5/15/2020. Goldman Sachs' strong and weak balance sheet indices each contain 50 S&P 500 companies across eight sectors with strong and weak balance sheets, respectively; using the Altman Z-score to measure balance sheet strength.

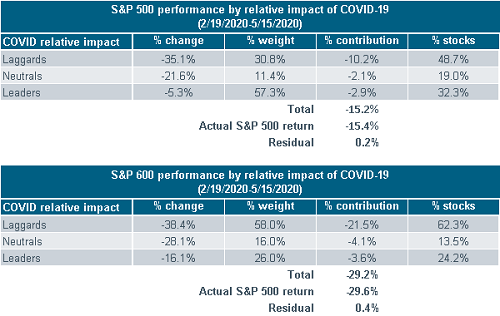

Finally, we also continue to be biased toward large cap stocks at the expense of small cap stocks—based on quality factors, but also virus-related factors. My dear friends at Ned Davis Research recently did an interesting analysis comparing the S&P 500 (representing large caps) and the S&P 600 (representing small caps) in terms of COVID-19 “exposure.” [Caveat: NDR used the S&P 600 for ease of analysis—the benchmark we (and many institutions) use is the larger Russell 2000 Index.]

Based on both quantitative and qualitative analysis, NDR found that more than 57% of the larger cap stocks in the S&P 500 are “beneficiaries” of the economic environment brought on by the virus (or the virus itself). It’s the near-mirror image in the case of smaller cap stocks in the S&P 600; with 58% found to be hurt by the impact of the virus on the economy.

Large Caps’ Higher % of COVID “Winners”

Source: Charles Schwab, ©Copyright 2020 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/, S&P Dow Jones Indices, as of 5/15/2020. COVID laggard: sub-industries not meaningfully or positively impacted by economic impact of COVID-19. COVID leader: sub-industries significantly negatively impacted by COVID-19 related stoppage of economic activity.

I could have added even more interesting charts; but this was getting long enough. For minute-to-minute updates on what I’m finding is most compelling, follow me on Twitter at @lizannsonders. In the meantime, let’s pray the good vaccine news hitting the newswires today proves to be an elixir for what ails the economy and humankind.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

©2020 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

(0520-0FWX)

© Charles Schwab

Read more commentaries by Charles Schwab