Key Points

-

Stocks have been consolidating their post-March 23 gains over the past few weeks, with a shift back toward growth characteristics.

-

Differences in age cohorts’ attitudes toward both the stock market and the virus may be at play.

-

A full market cycle condensed into a few months suggests investors should “react” by rebalancing; not try to anticipate the market’s short-term peaks and valleys.

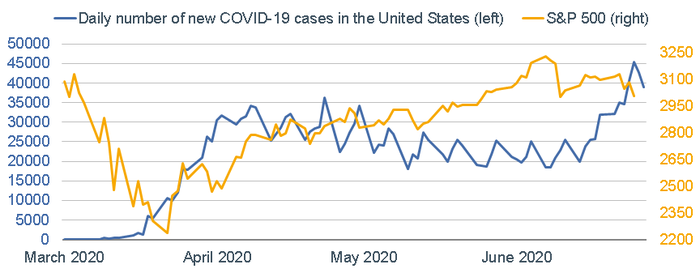

COVID-19 headlines dominated equity market action last week, with the S&P 500 suffering a near-3% decline; although all is not grim. The number of virus cases has been spiking in states that opened earliest—including my new home state of Florida, which went from a mid-60s average age for confirmed cases to the current mid-30s average age. The relatively good news, in the midst of more cases, is that new reported deaths declined over the weekend; with the seven-day average also moving lower. Coming about a week after virus-related hospitalizations began to move up—which has been the average lag—it highlights younger folks’ better chances at fighting the virus.

As an aside though, I witnessed first-hand the lower “compliance” in Florida with social distancing and the donning of face masks; especially among the younger set. I’m on Nantucket now for the remainder of the summer, where face masks are donned by nearly everyone—certainly in stores, where they’re mandated, but also out and about on the streets. It’s not been a scientific study by any means; but I believe the proximity to hot spots in the Northeast weighed more on the psyche of its population.

Since June 8, which was the most recent peak, the S&P 500 initially suffered a -7.1% pullback through June 11, followed by a 4.3% rally through June 23, and another selloff since then of -3.9%. The most recent peak in the S&P 500 corresponded to the point at which COVID-19 cases shot up again—likely not coincidentally.

COVID Cases vs. S&P 500

Source: Charles Schwab, Bloomberg, Johns Hopkins University, World Health Organization, as of 6/28/2020. S&P 500 as of 6/26/2020.

Don’t fight the Fed?

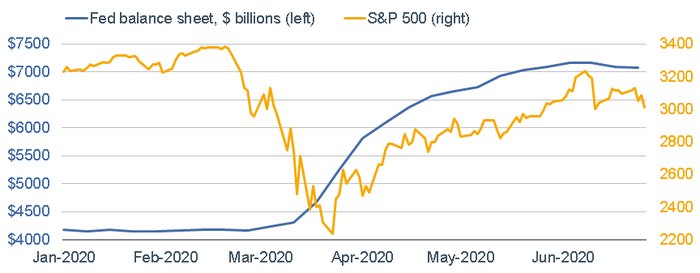

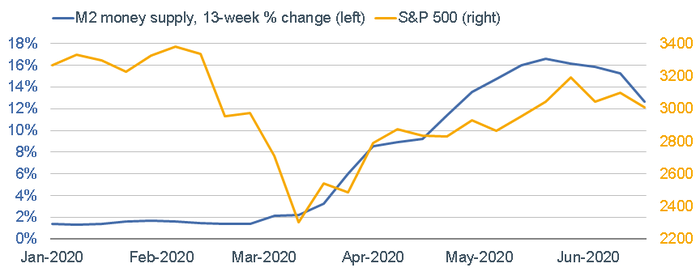

I won’t claim direct correlation (or even causation), but as you’ll see in the first chart below, the peak in the S&P 500 also came within the same time frame as the recent peak in the Federal Reserve’s balance sheet (which has had two consecutive weeks of slight declines). Related, the peak in the S&P 500 also came just after the peak in the 13-week percentage change in M2 money supply, as you can see in the second chart below. In essence, the “shock and awe” stage of Fed policy announcements is, for now, in the rear-view mirror.

Fed’s Balance Sheet vs. S&P 500

Source: Charles Schwab, Bloomberg, as of 6/26/2020.

M2 vs. S&P 500

Source: Charles Schwab, Bloomberg, as of 6/26/2020.

Phase-based sector leadership

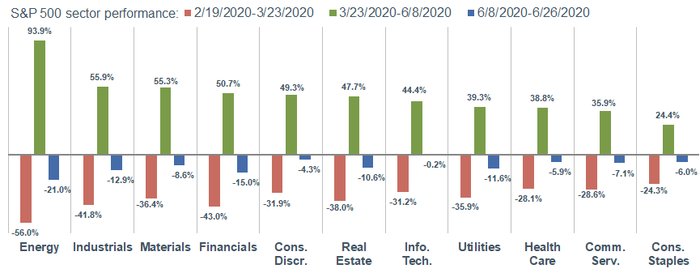

The chart below covers three distinct time periods in terms of sector leadership: the bear phase (February 19 through March 23); the recovery phase (March 23 through June 8); and what I’ll call the consolidation phase (June 8 through last Friday’s close). As you will see, the most-cyclical of sectors were hurt the most during the bear phase, with the energy sector taking it squarely on the chin and consumer stables suffering the least. During the recovery phase, cyclical sectors led; including a massive reversal in energy’s performance, followed by industrials and materials; while consumer staples brought up the rear. During the more recent consolidation phase, we’ve seen investors again favor growth sectors like technology and consumer discretionary; while energy and financials have been the laggards.

3 Phases of Sector Leadership

Source: Charles Schwab, Bloomberg, as 6/26/2020. Past performance is no guarantee of future results.

Speculation; but not everywhere

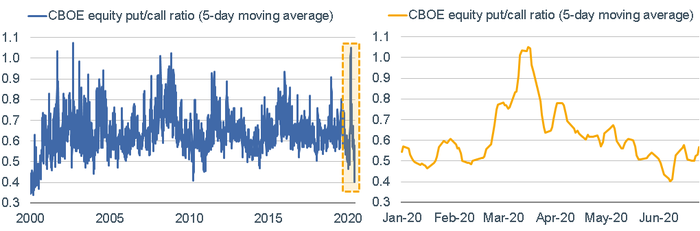

At the market’s recent early-June high, there was increasing attention devoted to signs of speculation in the market—notably among smaller newly-minted day traders’ activity in bankruptcy stocks and in the options market. In my recently-published mid-year outlook, and as seen in the chart below, I highlighted a post-2000 low in the five-day moving average of the CBOE put/call ratio as a sign of rampant bullish speculation (much more call buying than put buying). That bottomed a day after the recent June 8 peak in the S&P, and has since been generally trending higher—a better sign.

Put/Call Ratio Ticks Higher

Source: Charles Schwab, Bloomberg, as of 6/26/2020.

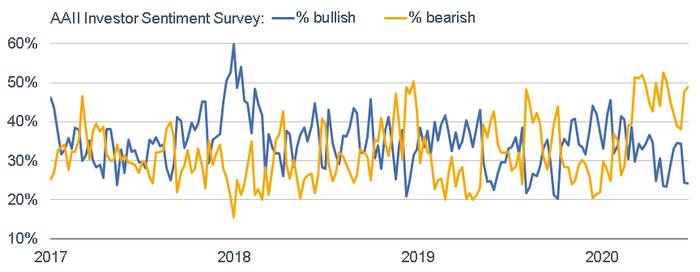

The put/call ratio is a behavioral measure of investor sentiment; with attitudinal measures significantly less stretched. The American Association of Individual Investors (AAII) does a weekly survey, and as seen in the chart below, the latest shows much more subdued optimism. Last week was the 18th consecutive week with the survey showing more bears than bulls, which is the second-longest streak since the survey’s inception in late-1987.

AAII Bears Still Outnumber Bulls

Source: Charles Schwab, Bloomberg, as of 6/24/2020.

Party like it’s 1999

For what it’s worth, I think there is a relationship between the virus and investor sentiment in terms of age cohorts. Much of the speculation in the stock market over the past few months has been concentrated among younger/newer investors and traders—who also happen to be the cohort often highlighted in the media as throwing caution to the wind with regard to social distancing and mask wearing. A survey like AAII has an older bias and may be indicative of a more cautious attitude about the stock market (as well as the virus).

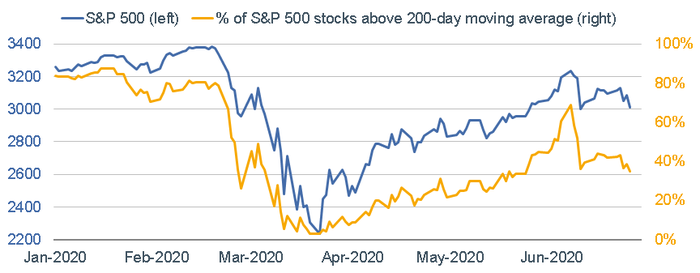

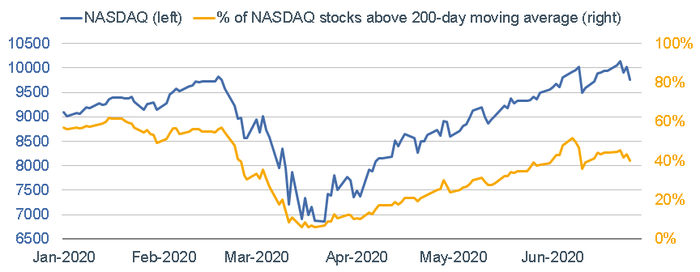

Sentiment is a mixed bag, as are technical conditions. As you can see in the first chart below, at the S&P 500’s June 8 high, the percentage of stocks within the index above their 200-day moving averages was more than 70%; while as of Friday, it was only 43%. In the case of the NASDAQ, as seen in the second chart below, the spread is even more severe.

Stocks vs. % > 200-DMA

Source: Charles Schwab, Bloomberg, as of 6/26/2020.

Source: Charles Schwab, Bloomberg, as of 6/26/2020.

On the other hand, there has been an extremely low percentage of new lows among all institutional-grade common stocks on all three major U.S. exchanged. In fact, from May 29 through June 19, there were zero. Bears will point out that there are also not a high percentage of new highs; but for now, the fact that there is no distinct bearish leadership is a near-term offsetting positive.

Hard to anticipate, better to “react”

I’ve been highlighting the warp speed nature of this crisis—with a “full” market cycle having been condensed into a few months. The wild swings have emboldened some investors and traders; while leaving others in a state of confusion. We’ve been recommending that investors remain at their long-term strategic equity allocations; but “react” to the larger swings by considering rebalancing more frequently. This allows portfolios to “stay in gear” by trimming into strength and adding into weakness; vs. trying to time short-term peaks and troughs (which is always extremely difficult).

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Rebalancing a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

©2020 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

(0620-07T7)

© Charles Schwab

Read more commentaries by Charles Schwab