Key Points

-

When it comes to the relationship between economic data and stock market behavior, “better or worse tends to matter more than good or bad.”

-

But in today’s uniquely-traumatic economic crisis, it’s important to consider both rate of change and level.

-

It’s likely going to take a significant span of time to get to pre-pandemic levels; with the recovery likely to be more “rolling Ws” and less an ongoing “V.”

For decades, when discussing the relationship between economic data and stock market behavior, I’ve shared the perspective that “better or worse tends to matter more than good or bad.” In other words, trends—and in particular, inflection points—in the data tends to have a larger impact on stock market action than levels. It’s human nature to think about the economy and its component drivers with a good vs. bad or strong vs. weak perspective. But as has clearly been seen in the past couple of months, the turn in economic data—even if the levels of that data—can be a powerful elixir for the stock market.

A V-shaped economic recovery narrative has taken root; courtesy of both the move off the bottom in a wide variety of economic data points; but also the epic rally in stocks off the S&P 500’s March 23 trough. There is no quibbling with the V-shape surge off the economic bottom (which for now appears to have been April or May depending on the metric); but in these unique times, level should be considered as well. The “law” of small numbers is such that, when you compress economic activity to near-nil courtesy of a full-stop economic shutdown by government mandate, the percentage gains off those lows will look exceptionally strong. But be careful with regard to extrapolating these early percentage gains.

Remember this simple math—a drop of 50% in the price of anything requires a 100% gain to get back to even. Even a 25% drop requires more than a 33% gain to get back to even. I think you get the point. Below are charts showing monthly or weekly change for a variety of well-watched economic data points; as well as their level or yearly change versions. As you will see, there is a huge difference in what is likely perceived if you limit your analysis to the shorter-term/rate-of-change perspectives.

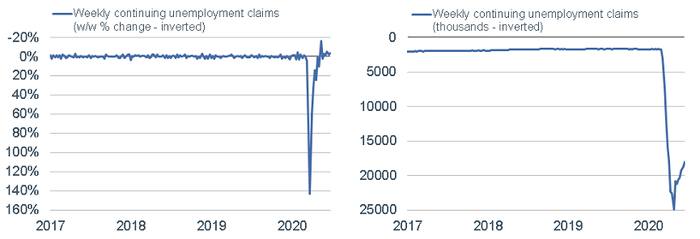

In all cycles, but especially during this historically-unique crisis, looking at leading economic indicators is crucial. Key among them are unemployment claims; and the variety of its component indicators. The first chart below is a simple (and inverted) look at weekly continuing unemployment claims (“continuing” representing those remaining on unemployment insurance because they’ve yet to find a job). This looks like a complete V recovery; but in level terms, it’s not even close.

Continuing Claims

Source: Charles Schwab, Bloomberg, as of 6/27/2020.

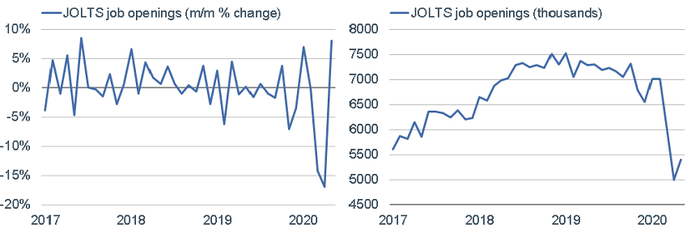

Another leading labor market indicator is job openings; with data curated by the Job Openings and Labor Turnover Survey (JOLTS). In monthly change terms, the latest surge has been exceptionally strong. However, the change in level terms is significantly more subdued.

Job Openings

Source: Charles Schwab, Bloomberg, as of 5/31/2020.

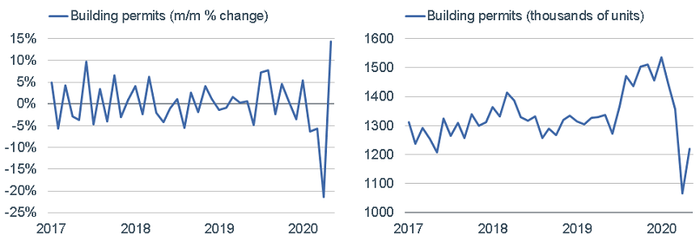

A final leading indicator worth noting is building permits; which like retail sales (see below), have seen a remarkable surge off the pandemic low. That said, in level terms, less than a third has been recovered.

Building Permits

Source: Charles Schwab, Bloomberg, as of 5/31/2020.

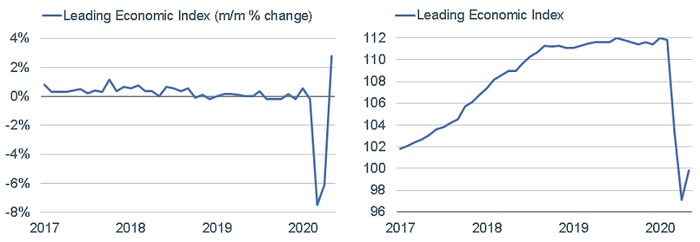

As noted, claims, job openings and building permits are all leading economic indicators. In fact, claims and permits are two of the 10 components of the Leading Economic Index (LEI) put out by The Conference Board. As with much of the data above, in monthly change terms, the recovery in the LEI is more than a complete V. However, in level terms, it’s only slightly off the recent low.

LEI

Source: Charles Schwab, Bloomberg, The Conference Board, as of 5/31/2020.

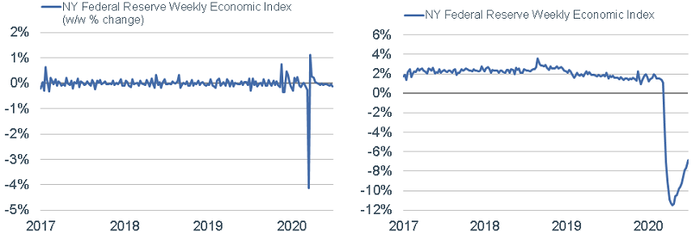

A newer compendium of leading economic indicators was put together early in the pandemic era by the New York Federal Reserve. The Weekly Economic Index (WEI) incorporates a few “standard” leading indicators, like claims, but also higher-frequency leading indicators most relevant to the current crisis (like shorter-term consumer confidence, temporary staffing, electricity output and fuel sales). As seen in the weekly change version of the WEI, the recovery off the pandemic low was straight up; but in level terms, only about a third of a recovery to prior levels has occurred.

WEI

Source: Charles Schwab, Bloomberg, as of 7/4/2020. Daniel Lewis, Karel Mertens, and Jim Stock, “Monitoring Real Activity in Real Time: The Weekly Economic Index,” Federal Reserve Bank of New York Liberty Street Economics.

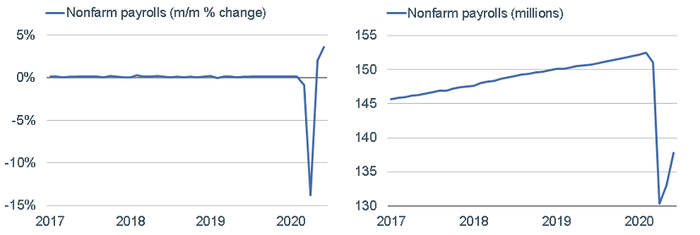

We can also look at coincident economic indicators; of which payrolls is one. Nonfarm payrolls’ monthly change shows a pure V, with the latest reading well above pre-pandemic levels. However, showing the same data, but instead in level terms (millions of people), the recovery to-date isn’t even close to bringing payrolls back to pre-pandemic levels.

Payrolls

Source: Charles Schwab, Bloomberg, as of 6/30/2020.

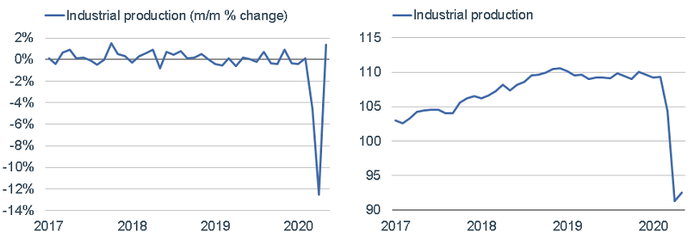

Another coincident economic indicator is industrial production. As seen below, the monthly change shows a perfect V recovery; while in level terms, the move off the low is still miniscule.

Industrial Production

Source: Charles Schwab, Bloomberg, as of 5/31/2020.

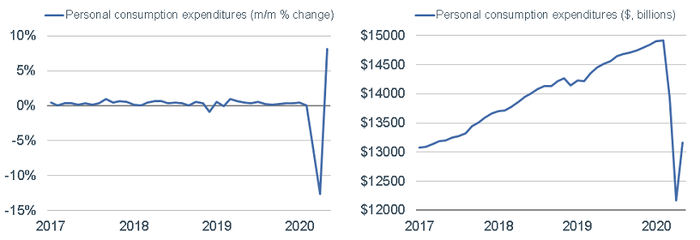

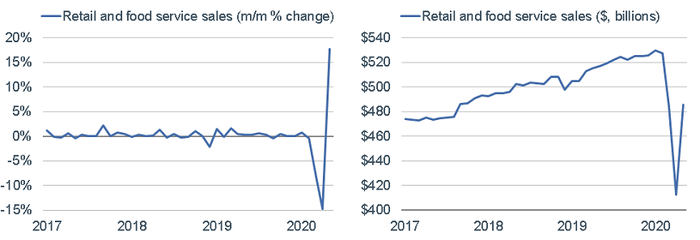

Consumer behavior is also generally a coincident indicator (while consumer confidence is a leading indicator). Two ways to measure consumer behavior are shown below. The first pair of charts is for personal consumption expenditures (PCE); and as you can see, the monthly change version shows more than a full V recovery; while in level terms, the retracement has only been about one-third of the way toward pre-pandemic levels. Looking at retail sales, the monthly change has been even more remarkable, having gone from a contraction of -15% to a gain of 18%. Here, even the change in level terms is healthier than many other indicators—with more than half of the retracement job done.

PCE

Source: Charles Schwab, Bloomberg, as of 5/31/2020.

Retail Sales

Source: Charles Schwab, Bloomberg, as of 5/31/2020.

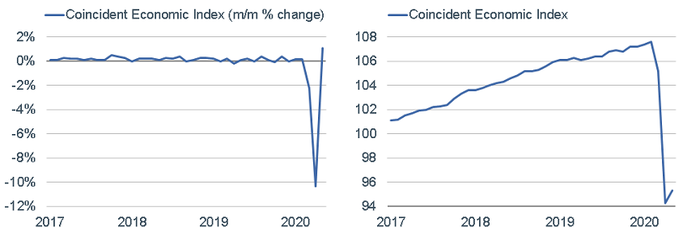

Summing it all up, we can look at The Conference Board’s Coincident Economic Index (CEI), which includes payrolls, industrial production, wholesale/retail sales and personal income. Not “coincidentally,” these are the metrics the National Bureau of Economic Research (NBER) uses to officially date recessions. Like with the LEI, the recent monthly change in the CEI looks like a V, while in level terms, the jump is more of a hop.

CEI

Source: Charles Schwab, Bloomberg, The Conference Board, as of 5/31/2020.

Concluding thoughts

The ongoing surge in COVID-19 cases in many newer U.S. hot spots continues to point to more of a “rolling Ws”-type recovery vs. a continuation of the V-type recovery seen in many shorter-term looks of economic data. Even without a full-scale shutdown of the economy—either at the federal or state/local level—economic activity is likely to be volatile and subject to consumers’ and businesses’ fears about the virus impacting activity and behavior.

But the news is not all grim. Although uneven, the recovery is unlikely to fully peter out—especially given ongoing support from the Federal Reserve and likely-additional support from Congress. Although increasing layoffs associated with the weaker business climate, and climbing bankruptcies, will weigh on confidence and the labor market, businesses’ fixed costs will decline, aiding profit margins. Longer-term, consumer spending and the services side of the U.S. economy are unlikely to resume their pre-pandemic weights within overall economic growth. However, the investment side of the economy—including technology, health care and housing—could pick up a significant amount of that slack.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

©2020 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

(0720-0RDT)

© Charles Schwab

Read more commentaries by Charles Schwab