Key Points

-

The Fed left rates unchanged and reiterated its pledge to increase its holdings of Treasuries and mortgage-backed securities.

-

There was no mention in the statement of inflation targeting, new forward guidance or yield curve control; but heavy emphasis on the “course of the virus.”

-

The Fed reiterated that it will use its “full range of tools” to support the economy.

In a unanimous vote, the Federal Open Market Committee (FOMC) left the benchmark federal funds rate near zero and reiterated its commitment to using all necessary tools to underpin the U.S. economy amid an inconsistent and at times faltering recovery from the COVID-19 pandemic. In the FOMC’s statement, it said the “path of the economy will depend significantly on the course of the virus;” and that economic activity and employment “have picked up somewhat in recent months but remain well below their levels at the beginning of the year.”

The statement reiterated that the pandemic “poses considerable risks to the economic outlook over the medium term” and that the federal funds rate would remain near zero “until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.” The Fed is closely monitoring the virus noting “the path of the economy will depend significantly on the course of the virus.” That comment was directly related to the sharp reversal in some of the highest-frequency economic indicators since virus cases began to surge again last month.

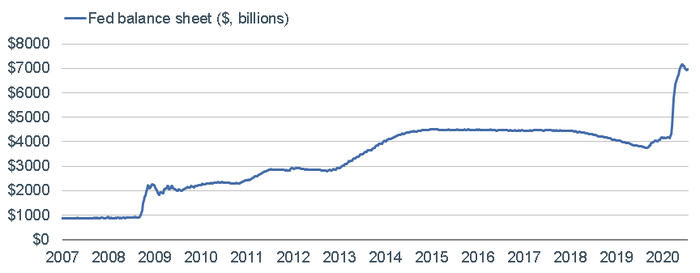

In terms of the Federal Reserve’s balance sheet—shown below—the FOMC reiterated its pledge to increase its holdings of Treasuries and mortgage-backed securities “at least at the current pace” in the near future. Separately, the Fed said it extended its temporary repurchase agreement facility for foreign and international monetary authorities, and its dollar liquidity swap lines, through the end of next March.

Notably, the dollar swap lines have had limited “take up,” which has contributed to the recent rolling over in the size of the balance sheet. As my colleague Kathy Jones, Schwab’s Chief Fixed Income Strategist, tweeted today, extending the swap lines is for insurance and to signal that dollar liquidity will remain ample. Even if not used heavily, their presence removes one of the fears of holding other currencies—especially emerging market (EM) currencies. The swap line extension, which boosts access to U.S. dollars within the global financial markets, is likely to keep downward pressure on the U.S. dollar.

Source: Charles Schwab, Bloomberg, as of 7/22/2020.

The statement did not provide any detail on the expectation by some economists that the Fed may begin linking the path of the federal funds rate to specific inflation and/or unemployment thresholds. There was also no mention in the statement of new forward guidance on asset purchases and/or interest rates; yield curve control; or the overall monetary policy framework (although Fed Chair Jerome Powell mentioned it in his comments at the start of the press conference). All of the above could be under consideration heading into the September FOMC meeting.

During the press conference, Chair Powell was asked about fiscal policy, and he praised the swiftness with which Congress acted at the outset of the pandemic; adding that “fiscal policy is essential” and that “fiscal policy can address things we can’t address.” Powell was also asked about inflation risk and he was emphatic that it’s not a risk—at least not one likely to arise due to the Fed’s aggressive policy measures. Finally, in terms of the outlook for rates, Powell repeated one of his most popular recent “lines,” saying “as I said earlier, we’re not even thinking about thinking about raising rates.”

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

©2020 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

(0720-0S77)

© Charles Schwab

Read more commentaries by Charles Schwab