Rotation away from the market’s prior momentum darlings continues.

Friday’s jobs report had bullets for both the optimists’ and pessimists’ case studies.

Improving productivity, partly due to work-from-home trends, could persist as a positive economic driver.

Today’s report will look at the latest labor market data; but before we get to that, an update on the market is in order. My last report of two weeks ago focused on the narrowness of the market’s advance to new all-time highs, along with some of the troubling speculative froth being witnessed. Given the early weakness in the prior high-fliers as we start the holiday-shortened week, a brief update is warranted.

I concluded that late-August report with the following: “I worry about the signs of froth in the market and among some behavioral measures of investor sentiment; not to mention traditional valuation metrics that are historically-stretched. This is not an environment in which greed should dominate investment decisions; but instead one for discipline around diversification and periodic rebalancing.”

So where do things stand today?

In terms of “signs of froth,” small traders continue to dominate the options market. According to SentimenTrader, since mid-July, trades for 10 contracts or fewer have consistently accounted for more than 60% of all opening call purchase premiums, massively dwarfing larger trade sizes. Importantly, last week’s volatility did not discourage these traders; it did the opposite: they added to their bullish bets.

Rotation is likely to continue to characterize the market’s behavior. Year-to-date (YTD) through the end of August, we hit the widest spread since 1932 between the best (technology) and worst (energy) performing sector—76%—according to SentimenTrader. In fact, the only years since 1932 when the YTD-August difference neared or exceeded 50% were 1987 and 2000. Historically, the ratios between best and worst sectors tended to narrow after such wide differences in returns.

Conclusion: caveat emptor.

Back to the job(s) at hand

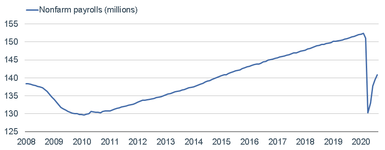

Amid the cheering of a better-than-expected August non-farm payrolls report from the Bureau of Labor Statistics (BLS) reported this past Friday, a look under the hood reveals a mixed picture. Yes, the creation of 1.371 million jobs and the unemployment rate falling to 8.4% (from 10.2% in July) were both good news. However, as you can see in the chart below, the gain in payrolls since the trough of the plunge hasn’t been anywhere near enough to erase the prior carnage.

Payroll Gains Recovering, But Not Recovered

Source: Charles Schwab, Bloomberg, as of 8/31/2020.

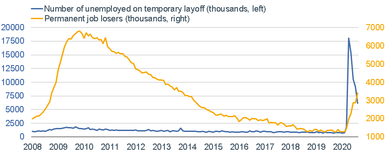

In addition, as you can see in the chart below, permanent job losses continue to increase—rising to 3.4 million last month—while those on temporary layoff continue to decline—falling to 6.16 million last month (down from the peak of 20.6 million in April). In April, the number of people without a job who believed their job losses were permanent had barely budged; but it has grown steadily since then. Plus, the increase in permanent job losses is being accompanied by a longer duration of unemployment, even though the unemployment rate is falling (an unusual occurrence in an unusual recession).

Permanent Job Losses on Rise

Source: Charles Schwab, Bloomberg, as of 8/31/2020.

The unemployment rate has been falling due to the temporarily unemployed getting their jobs back. A back-of-the-envelope calculation of those having lost their jobs permanently gets you to about an 8% unemployment rate—not much below the official headline number—suggesting a likely leveling out in the near-term. In other words, don’t extrapolate last month’s improvement on an ongoing basis … especially if there is no additional fiscal relief package passed by Congress.

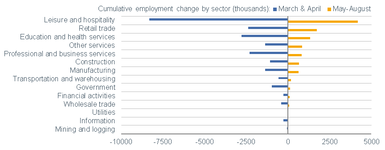

Below we look at the sector-based employment trends; covering the plunge period from March through April; as well as the recovery since then. As you can see, leisure/hospitality and retail trade have had the largest payroll gains; but nowhere sufficient enough to recover the prior job losses.

Most Beleaguered Sectors Driving Employment Gains

Source: Charles Schwab, Bureau of Labor Statistics, as of 8/31/2020.

Less grim

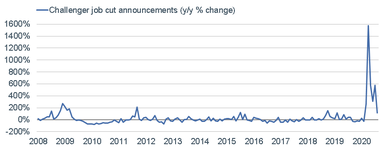

There is some underlying better news in some of the labor market’s leading indicators; including a continued plunge in job cut announcements and a recent uptick in job openings (see charts below).

Job Cut Announcements Plunging

Source: Charles Schwab, Bloomberg, as of 8/31/2020.

Job Openings Tick Higher

Source: Charles Schwab, Bloomberg, as of 6/30/2020.

More positive

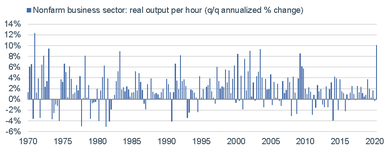

In addition, productivity has been on a tear—likely aided by the COVID-19 pandemic and the work-from-home (WFH) shift by many companies/workers. The extreme fall in gross domestic product (detailed later in this report) was accompanied by an ever larger fall in employment, which boosted productivity to its highest reading since the beginning of 1971, as you can see below. As I, and likely most folks who are working from home, can attest, much of the time we spent commuting and/or traveling has been devoted to longer work hours. Morgan Stanley’s economics team recently conducted a WFH study and found that the “shift to work from home is creating a new normal that is remaking the workplace, consumer behavior, spending patterns, productivity and more” and that “ultimately, these shifts could be longer term positives for the economy.”

Productivity Surging

Source: Charles Schwab, Bloomberg, as of 6/30/2020.

The productivity improvement has important implications; not least for corporate profit margins and keeping inflation contained. Productivity is one of the two main drivers of GDP—the other being labor force growth, which has been rising. Productivity has been, and likely will continue to be, boosted by investments in technology/efficiency. According to Cornerstone Macro, capital spending for equipment (about 40% of total capex) is on track to increase nearly 30%, based on nondefense capital goods orders; and the regional manufacturing indices show capex gained traction in August. In fact, “new economy capex”—encompassing technology equipment, software and research/development (R&D)—now account for more than half of all capex.

Speaking of GDP…

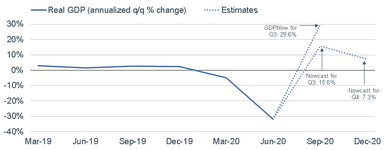

Partly courtesy of the improved labor statistics (as well as the COVID-19 statistics), estimates for third quarter real GDP have been on the rise—albeit with a fairly wide range of economists’ forecasts. In terms of the annualized quarter/quarter change, which is how GDP is reported, you can see the trajectory over the past 18 months; including the epic 31% plunge courtesy of the pandemic-related economic shut down. The subsequent dotted lines show two sets of estimates that are widely tracked—the much more significant improvement to nearly +30% in the third quarter is the Atlanta Fed’s GDPNow forecast; while the more subdued forecast of about half of that is the NY Fed’s Nowcast. In the case of the latter, the NY Fed also has a forecast for the fourth quarter of a lesser, but still-positive ~7%.

GDP in % Terms Likely to Surge

Source: Charles Schwab, Bloomberg, Federal Reserve Bank of Atlanta (GDPNow), Federal Reserve Bank of New York (Nowcast), as of 9/4/2020.

Lest you conclude, by looking at the chart below, that we are in the midst of a more than V-shaped recovery, remember how the math works coming off large percentage contractions. If you look at GDP in level terms ($ trillions), even the more robust GDPNow forecast would mean the recovery still has a ways to go to round-trip back to the prior peak in activity.

GDP in $ Terms Less Impressive

Source: Charles Schwab, Bloomberg, Federal Reserve Bank of Atlanta (GDPNow), Federal Reserve Bank of New York (Nowcast), as of 9/4/2020.

In sum

For reasons discussed above, payroll gains are likely to shift into lower gear as real GDP growth ebbs from its initial rebound; while the rate of the decline in the unemployment rate is also likely to ebb. Key to watch over the next several months’ worth of labor market data is the relationship between temporary and permanent job losses.

Cueing Joseph Schumpeter, we are arguably in the midst of the “gale of creative destruction” in the drivers of the U.S. economy and its labor force. It can (and will) create space for creative new companies and technologies to emerge; but not without some destruction along the way—hopefully with much of it now behind us.