2021 Mid-Year Outlook: U.S. Stocks and Economy

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Points

-

Second quarter is likely the peak growth rate for both the economy and corporate earnings; with positive economic surprises waning.

-

For now, inflation looks “transitory,” but labor market slack holds the key to whether it becomes more persistent.

-

Sentiment, including margin debt and CEO confidence, suggest some contrarian market risk.

I’m a “rock chick” and nearly all my written reports are titled with a rock song title … but our twice-yearly outlooks don’t leave room for that levity; so I’ll weave them in another way. Last year at this time, I was asked on a virtual event what song(s) I felt best characterized the environment in which we were living. Immediately I thought of both Gimme Shelter by The Rolling Stones and Don’t Stand So Close to Me by The Police. Today I might choose Back in the Saddle Again by Aerosmith, reflecting the fact that we are in the midst of the U.S. economy likely surpassing its pre-pandemic level as measured by gross domestic product (GDP). This is unquestionably good news; but may not mean smooth sailing for the stock market as you’ll read below.

Boom-what?

The question as we head toward the second half of the year is whether we’re facing a long-lasting boom (aka, a new “Roaring Twenties”), a boom-settle, or a boom-bust scenario. At this point, I lean toward the boom-settle scenario; in part because we may be facing another peak in the growth rate for both the economy and corporate earnings (distinguished from peak growth). Last year at this time we were in the midst of the second quarter of 2020, when GDP contracted by -31.4 (quarter-over-quarter annualized rate). That was followed by the eye-popping initial rebound of +33.4% in the third quarter; with the fourth quarter coming in at a more tepid +4.3%.

This year’s first quarter saw growth of +6.4%, with the second quarter expected to jump to +9.4% as the economy fully opens. Bloomberg’s tracking of economists’ estimates suggests this will be followed by steadily descending, but still positive, growth rates in the subsequent two quarters (+6.8% and +4.8%, respectively). In fact, after some epically strong readings, the latest economic data has been mixed-to-weaker; including worse-than-expected readings for personal income, new and pending home sales, durable goods, consumer confidence and the Chicago Fed’s National Activity Index.

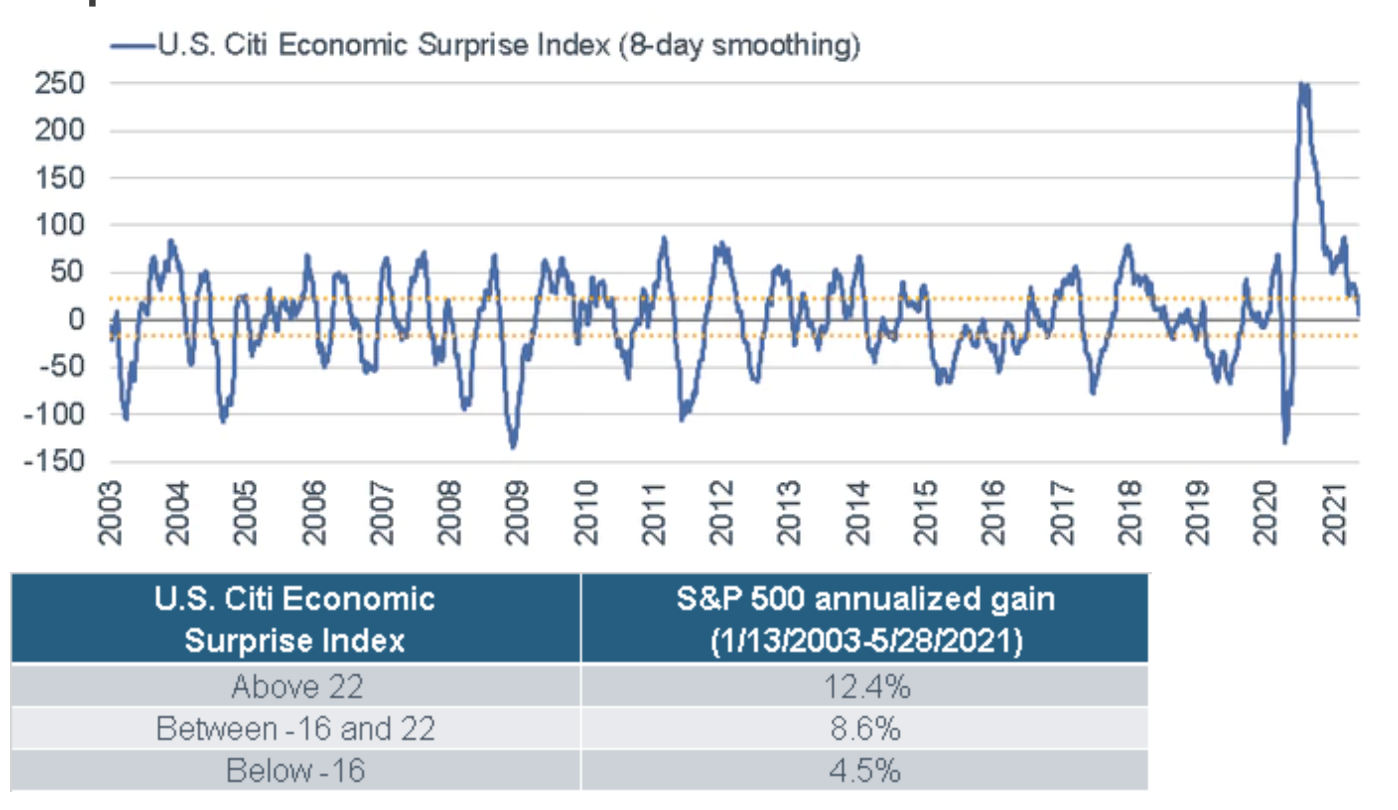

As you can see below, the Citi Economic Surprise Index—which measures how economic data is coming in relative to expectations—has come significantly off the boil relative to its peak last July. The accompanying table shows that as the index descended historically, so did annualized returns for the S&P 500.

Surprise?

Source: Charles Schwab, The Conference Board, ©Copyright 2021 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/, as of 2Q2021. Yellow dotted lines represent Citi Economic Surprise Index readings of above 22 and below -16. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly Past performance is no guarantee of future results.

Liquidity drain?

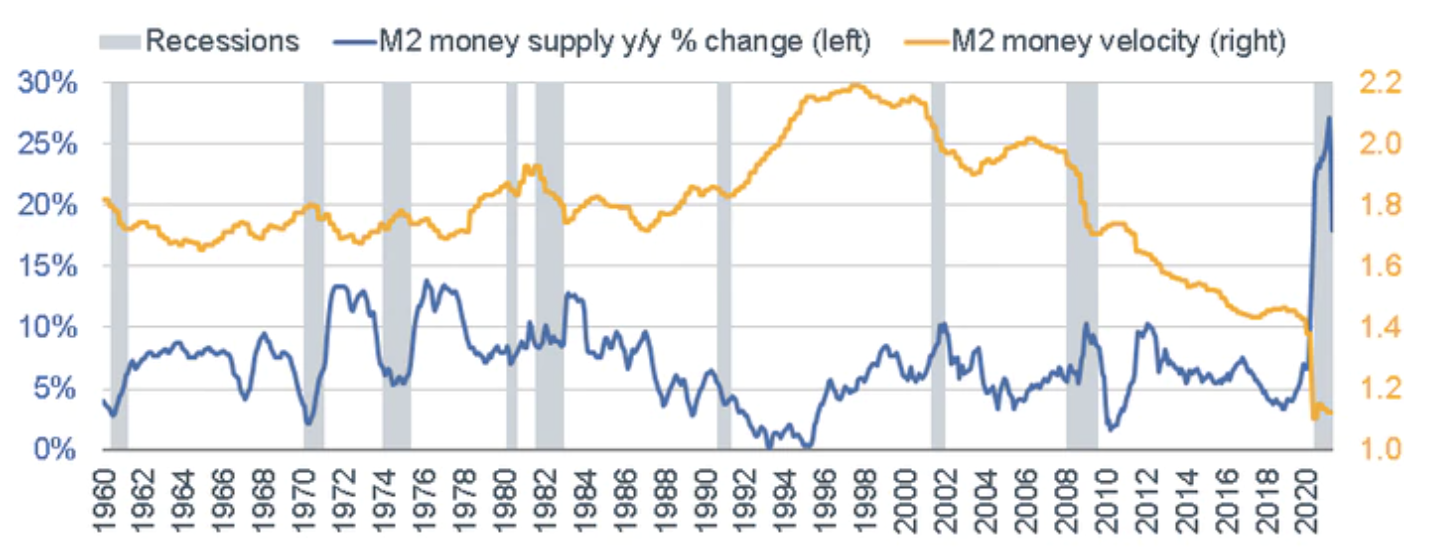

A contributing driver of less-robust economic data is likely the fading impact of fiscal stimulus thanks to direct stimulus checks being in the rear-view mirror; and supplemental unemployment insurance set to expire in early September (for those states which opted not to end it sooner). Although the Federal Reserve has not yet begun to put some of its crisis tools back in the toolbox, the impact of waning fiscal stimulus has led to a reversal in money supply growth, as you can see below. In the meantime, the velocity of money—the rate at which money is exchanged in the economy—remains historically low. This is one reason to hope that the current bout of inflation is indeed transitory, which continues to be the Fed’s mantra. [For more on inflation, see https://www.schwab.com/resource-center/insights/content/world-inflation-transitory-or-more-nefarious]

M2 Growth Coming Off Boil

Source: Charles Schwab, Bloomberg, Federal Reserve Bank of St. Louis, as of 4/30/2021. The velocity of money is the number of times one dollar is spent to buy goods and services per unit of time. If the velocity is increasing, then more transactions are occurring between individuals in an economy.

In addition, real M2 growth is now exceeded by industrial production growth, which means there has been negative liquidity growth over the past year. Speaking of liquidity, we expect the Fed to begin telegraphing the first step in normalizing monetary policy; perhaps as soon as the mid-June Federal Open Market Committee (FOMC) meeting. Including in the recent release of the minutes of the April FOMC meeting, and by several Fed officials since, discussions are underway about when to start tapering the Fed’s balance sheet. Its current $120 billion per month pace of purchases of Treasuries and mortgage-backed securities (MBS) will likely be pared steadily, but gradually, given the risk associated with its massive $7 trillion balance sheet. Like was the case in 2013, when the Fed announced a balance sheet tapering and stocks had a “taper tantrum,” the market could be at risk of a pickup in volatility.

Labor market, inflation and Fed’s reaction function

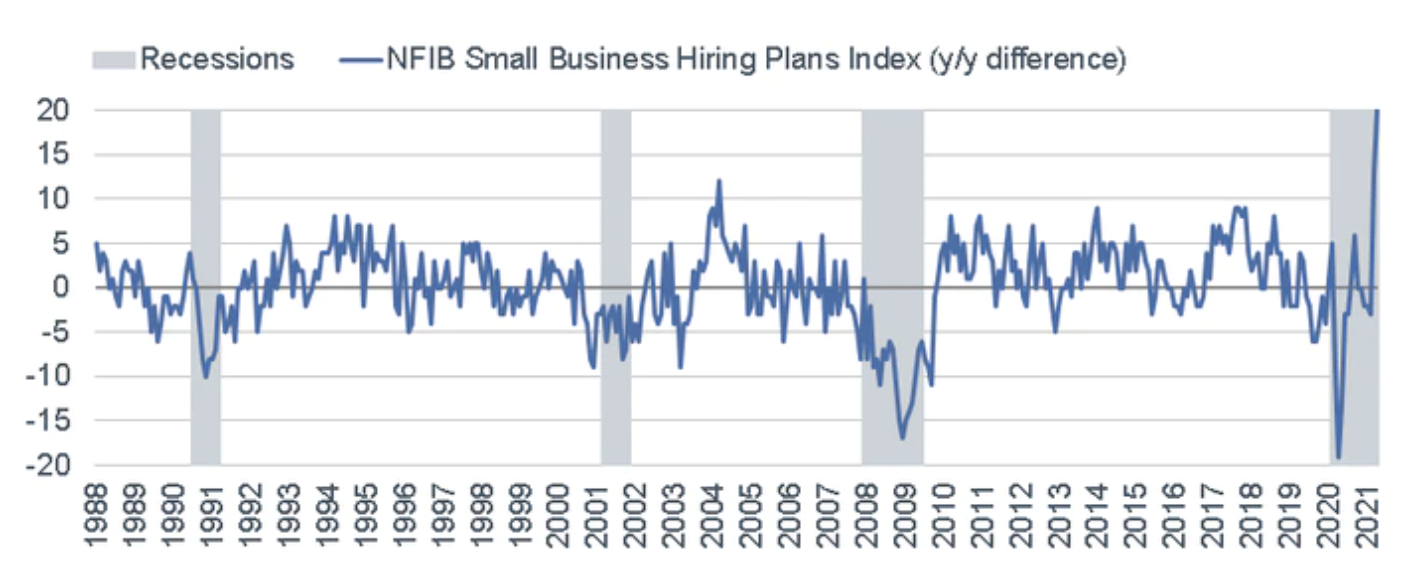

Key to the outlook for the economy broadly, as well as Fed policy and inflation, are labor market conditions. Small businesses—which are the largest net U.S. job creators—have robust hiring plans, as you can see below.

Small Business Hiring Plans’ Surge

Source: Charles Schwab, Bloomberg, as of 4/30/2021. NFIB’s (National Federation of Independent Business) Hiring Plans Index is based on Small Business Economic Trends Data which is a monthly assessment of the U.S. small-business economy and its near-term prospects.

Notwithstanding the weak April jobs report (this was written prior to the May report), the NFIB survey—as well as other leading labor market indicators, like job openings—point to a pickup in job growth. Payrolls are still more than 8 million shy of pre-pandemic levels; a gap unlikely to close this year unless we see a string of million-plus payroll gains. We have posited that although there are ample near-term upward pressures on inflation; absent a significant reduction in labor market slack and a sustainable increase in wage growth, inflation is unlikely to morph into a 1970s-style systemic wage/price spiral version. [https://www.schwab.com/resource-center/insights/content/is-1970s-style-inflation-coming-back]

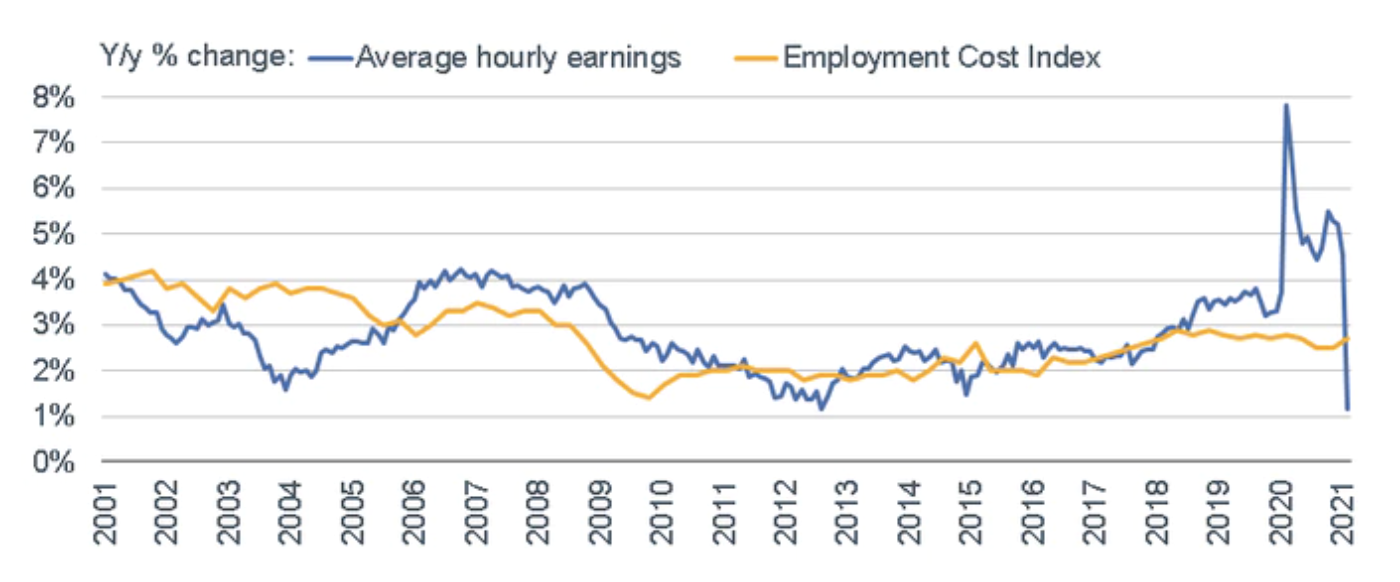

To rule that out, we need to keep a close eye on wage data; but would caution against using the standard average hourly earnings (AHE) metric, as it can be heavily-skewed by wage-level mix-shifts, as you can see below. When lower-wage jobs were lost en masse last year, it biased the average way up, and the opposite is happening now. That’s the way the math of a simple average works. That is why we prefer other metrics; notably the employment cost index (ECI), also shown below, which for now remains subdued.

Pandemic-Fueled Wage Volatility

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics (BLS), as of 4/30/2021. The Employment Cost Index (ECI) is a quarterly economic series published by the Bureau of Labor Statistics that details the growth of total employee compensation.

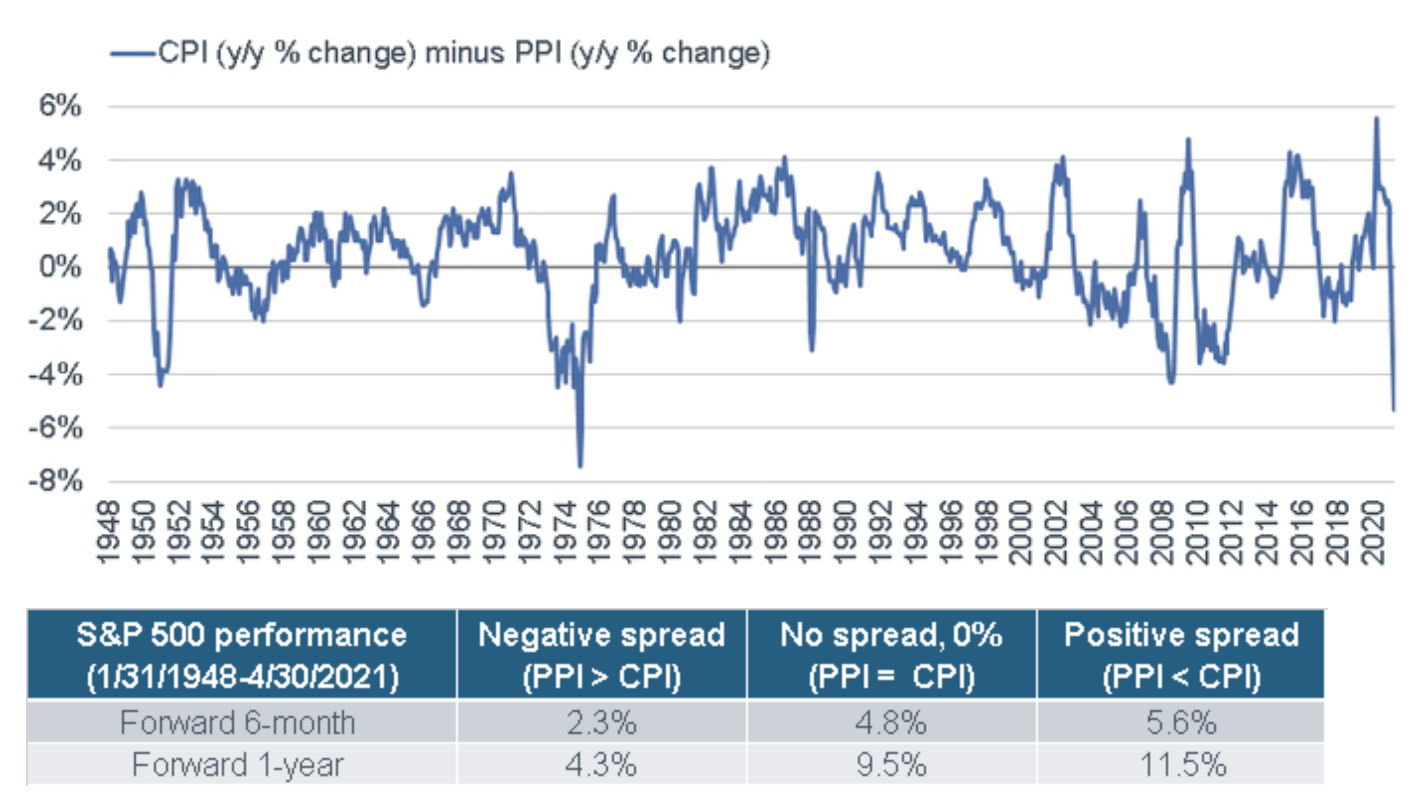

As mentioned, there are ample upward pressures on inflation at least near-term; including base effects (year-over-year comparisons to last year’s pandemic-related decline in inflation), and supply chain disruptions alongside rising demand. Raw material costs for businesses have spiked; and as such, the spread between the consumer price index (CPI) and producer price index (PPI) is historically wide; as you can see below. In fact, it’s the most negative since 1974. As you can see in the accompanying table, when the spread has been negative historically, stock market returns have been weaker; however as the spread narrowed and moved back into positive territory, stocks fared better.

Near-Record Spread Between CPI and PPI

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 4/30/2021. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Another spread that corroborates the data above is between the new orders and prices paid components of the Institute for Supply Management Manufacturing (ISM-M) index. The latest release of the ISM-M data kept the spread in deeply negative territory (-21%), which is up slightly from the prior month’s reading of -25% (the lowest since August 2008). According to SentimenTrader, when the spread was below -25% historically (data back to 1948), the S&P had an average -6% annualized return. We will be looking for a narrowing of these spreads, which may be aided by the retreat in some commodity prices; but will also require some easing in supply chain disruptions, which could persist.

Real earnings yield’s plunge

The recent spike in inflation has put a significant dent in one of the few stock market valuation metrics that had not been in the expensive camp. The real earnings yield of the S&P 500 is the inflation-adjusted earnings/price ratio (the inverse of the P/E ratio). As you can see below, it’s now negative to a degree not seen since the 1979-1980 time period.

Real Earnings Yield Goes Negative

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 4/30/2021. Real earnings yield is defined as S&P 500 current earnings yield minus y/y % change in CPI. Past performance is no guarantee of future results.

There have been five prior occurrences of the S&P 500’s real earnings yield turning negative for the first time in at least three years: August 1973, January 1980, August 1987, March 2000 and July 2008. With the exception of the 1980 occurrence, each was followed by weak equity market returns over the subsequent six-to-12 months. According to SentimenTrader data, three months after each of these occurrences (using month-end data), the S&P 500 was down every time; with a range of -3% in 2000, to -30% in 1987 thanks to the market crash that October.

Earnings on fire

In the interest of not being a total Debbie Downer with regard to equity market valuations, the relatively good news is that the traditional P/E ratio has been falling courtesy of the rapid acceleration of earnings growth since last year’s low. S&P 500 earnings bottomed in the second quarter of last year at -31%, which was followed by -7% and +4% in the third and fourth quarters, respectively. This year’s first quarter was significantly better than expectations, with growth coming in at +52% year-over-year. The consensus expectation for the second quarter now sits at more than +62%; after which earnings growth is expected to slip to +24% in the third quarter and +16% in the fourth quarter.

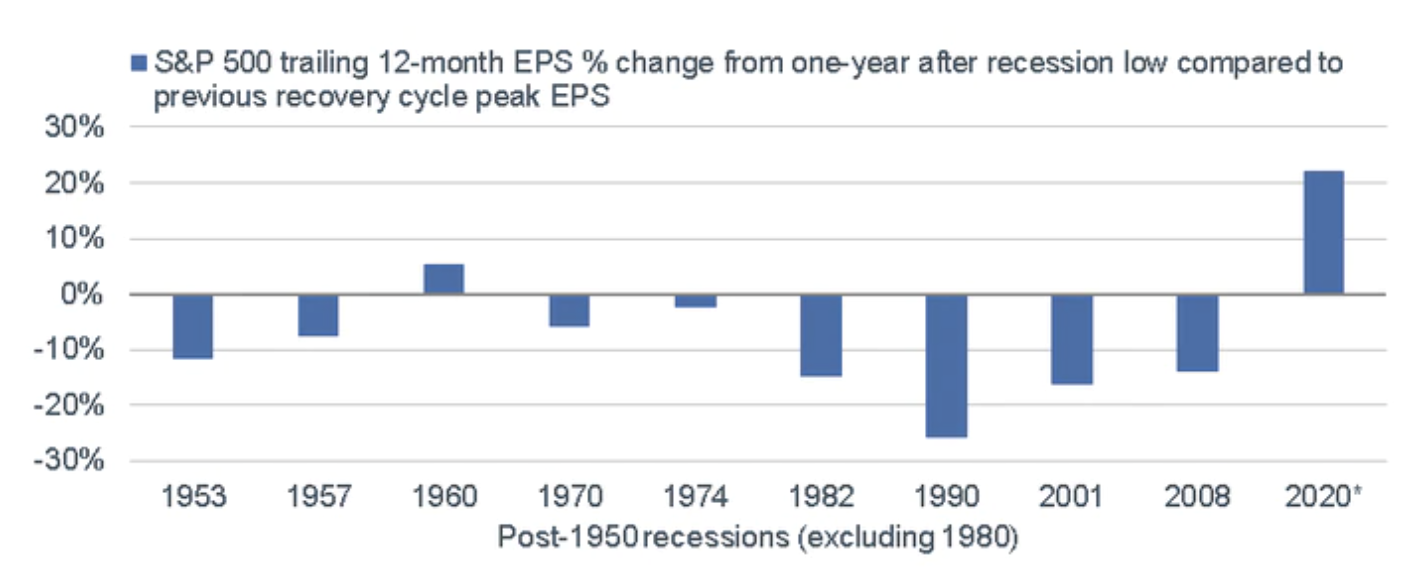

In essence, the U.S. economy and corporate earnings went from a depression-like bust to a wartime-like boom in the span of a year. Companies cut operations to the bone amid the early phase of the pandemic; then courtesy of record-breaking monetary/fiscal stimulus, the economy quickly found its footing. The study below by The Leuthold Group looked at every recession in the post-WWII period and examined the profit recovery one year after each recession low, compared to the prior expansion’s peak profit. Based on Bloomberg’s S&P 500 earnings-per-share (EPS) consensus for 2021 of $185 (which may prove too low given that first quarter growth came in at an annualized run-rate of more than $200); by the end of this year, earnings are likely to be more than 20% above the prior peak.

Epic Earnings Rebound

Source: Charles Schwab, Bloomberg, The Leuthold Group. *Based on median Bloomberg estimate of $185 EPS for 2021. Past performance is no guarantee of future results.

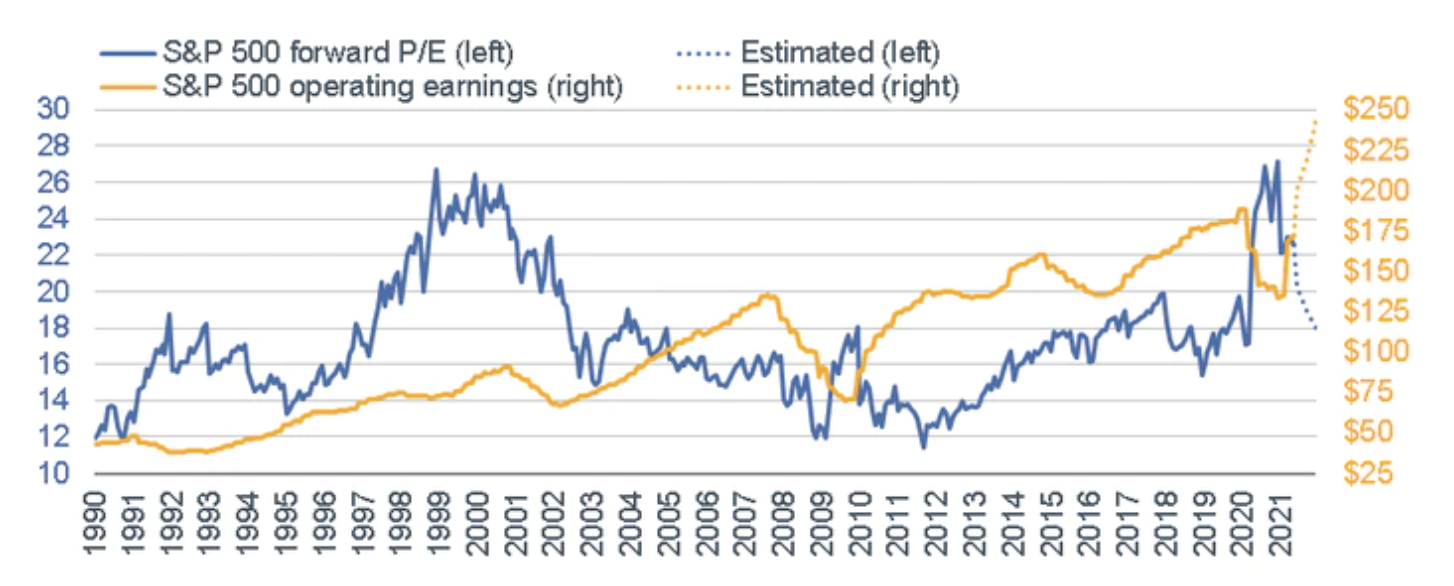

So, although the year-over-year growth rate for earnings is likely to peak in the second quarter, earnings should remain strong throughout the remainder of this year. Of course, the stock market has been moving up as well; but with its pace undercutting the pace of earnings growth, the forward P/E has been trending down, as you can see in the chart below. I expect stock market gains to continue to be lower than earnings gains, which would mean a further retreat in the S&P’s multiple. That said if inflation continues to accelerate, it may mean some downward macro pressure on higher-multiple segments of the market.

E Doing More of Market’s Heavy Lifting

Source: Charles Schwab, Bloomberg, as of 5/28/2021. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data

Emotional rescue

When discussing valuation, I often tie it to investor sentiment. Investors think of most valuation metrics as fundamental and quantitative in nature. In the case of a traditional P/E, there is a quantifiable numerator and denominator. However, the reality is valuation is to a large degree a sentiment indicator; or perhaps better put, an indicator of sentiment. There are times (like the late-1990s, and perhaps today) when investors are willing to pay lofty multiples for certain stocks; and other times (like early 2009) when investors are unwilling to pay even historically-low multiples for stocks.

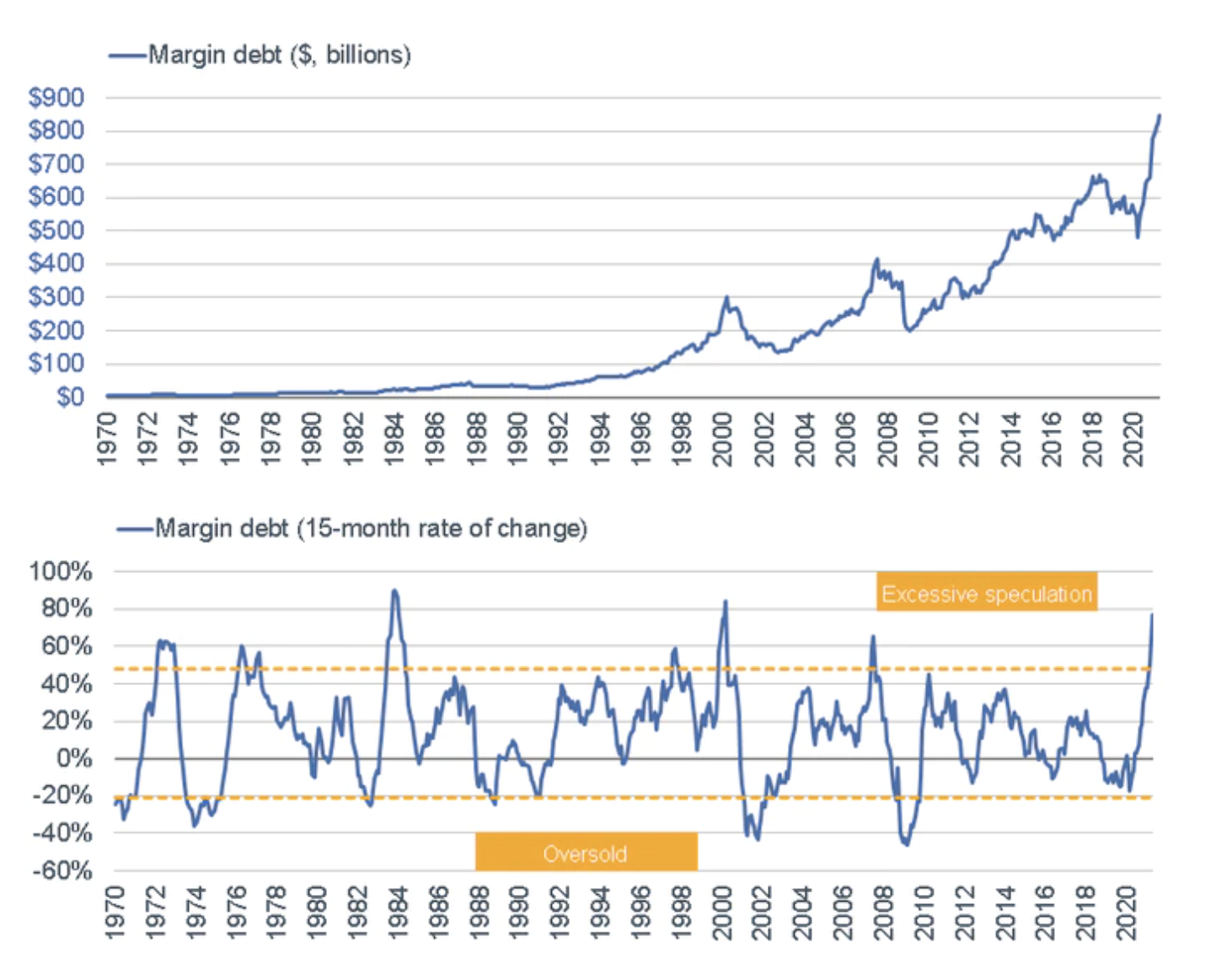

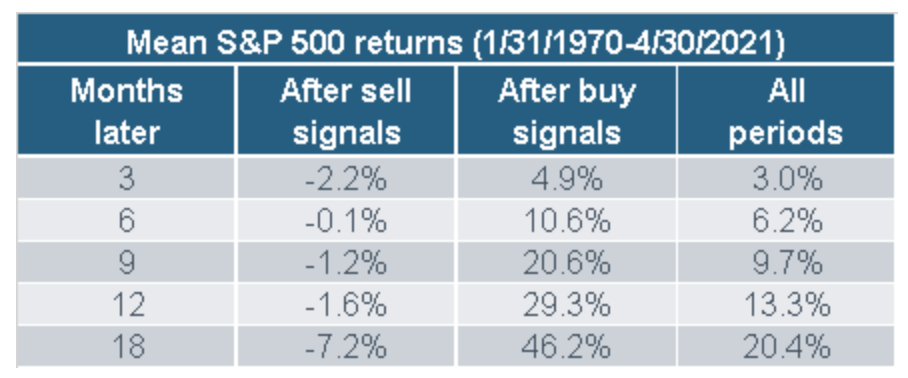

I want to focus attention on sentiment via two metrics particularly relevant to the current environment. The growth in investors’ margin debt has rightly received a lot of attention over the past few quarters. As you can see in the charts below, overall margin debt (first chart) is not far from $1 trillion; with the 15-month rate of change (second chart) in rarified air based on history.

Margin Debt Soars

Source: Charles Schwab, ©Copyright 2021 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/, as of 4/30/2021.

Our friends at Ned Davis Research have looked at those points in time when margin debt hit a peak and then began descending—considering them “sell signals.” Following those signals, the average subsequent returns for the S&P 500 for time periods ranging from three-to-18 months since 1970 were all in negative territory—although not to a significant degree. I will be keeping a close eye on margin debt—especially for a possible inflection point this year. For now, it’s not a contrarian indicator; but a reversal would represent a market risk. For comparison purposes, the table also highlights the average subsequent returns following “buy signals” (when margin debt hit a trough and then began ascending), which tended to be extraordinarily strong.

Source: Charles Schwab, ©Copyright 2021 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/, as of 4/30/2021. Sell signals generated when rate of change in margin debt falls below 48%; buy signals generated when rate of change in margin debt rises above -21%. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

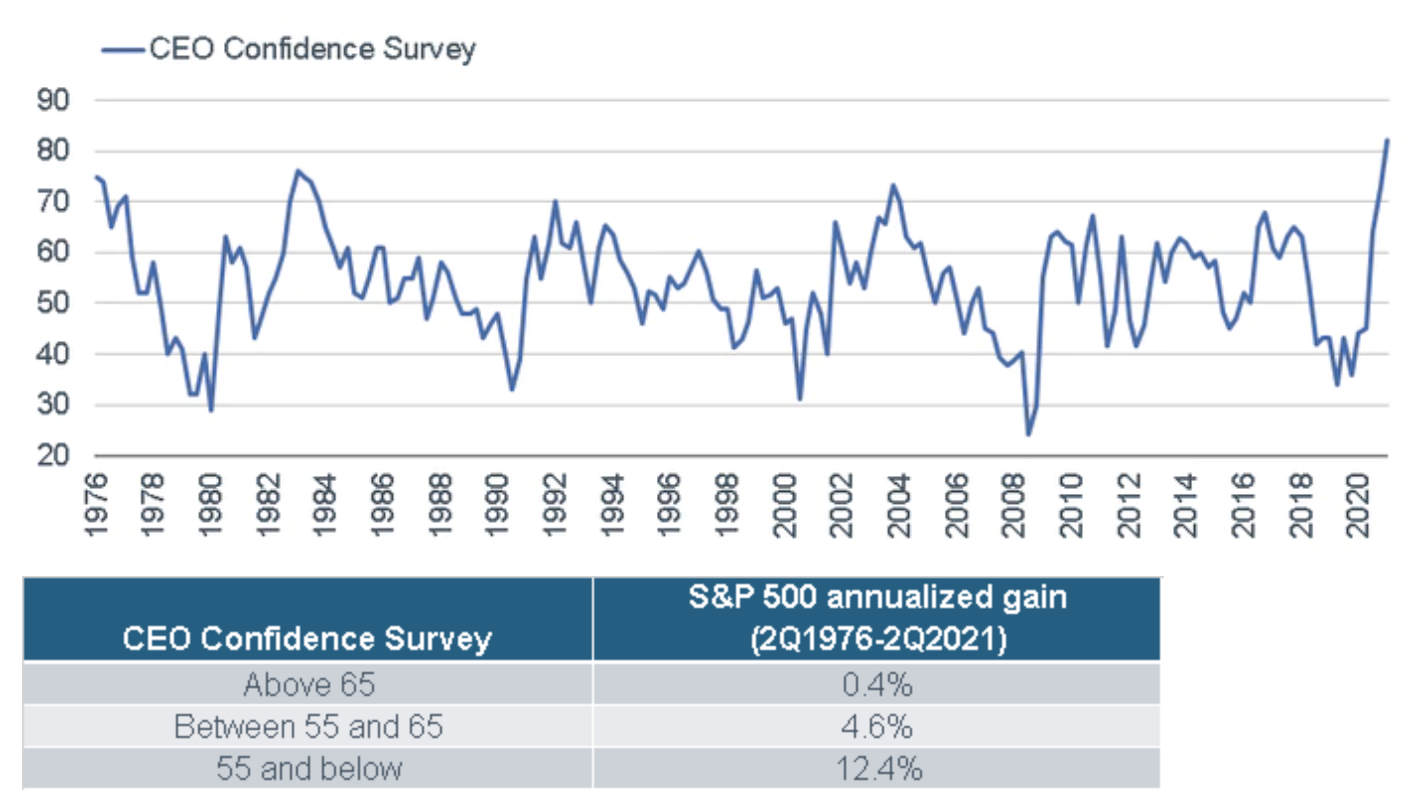

Another sentiment measure on which I keep an eye, which is not directly associated with investors, is CEO confidence. As measured by The Conference Board, CEO confidence is at a record high as you can see in the chart below. Historically, this has worked as a contrary indicator as it possibly signals the environment is “as good as it gets,” which you can see in the accompanying table.

CEO Confidence Soars

Source: Charles Schwab, The Conference Board, ©Copyright 2021 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/, as of 2Q2021. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Factors to consider

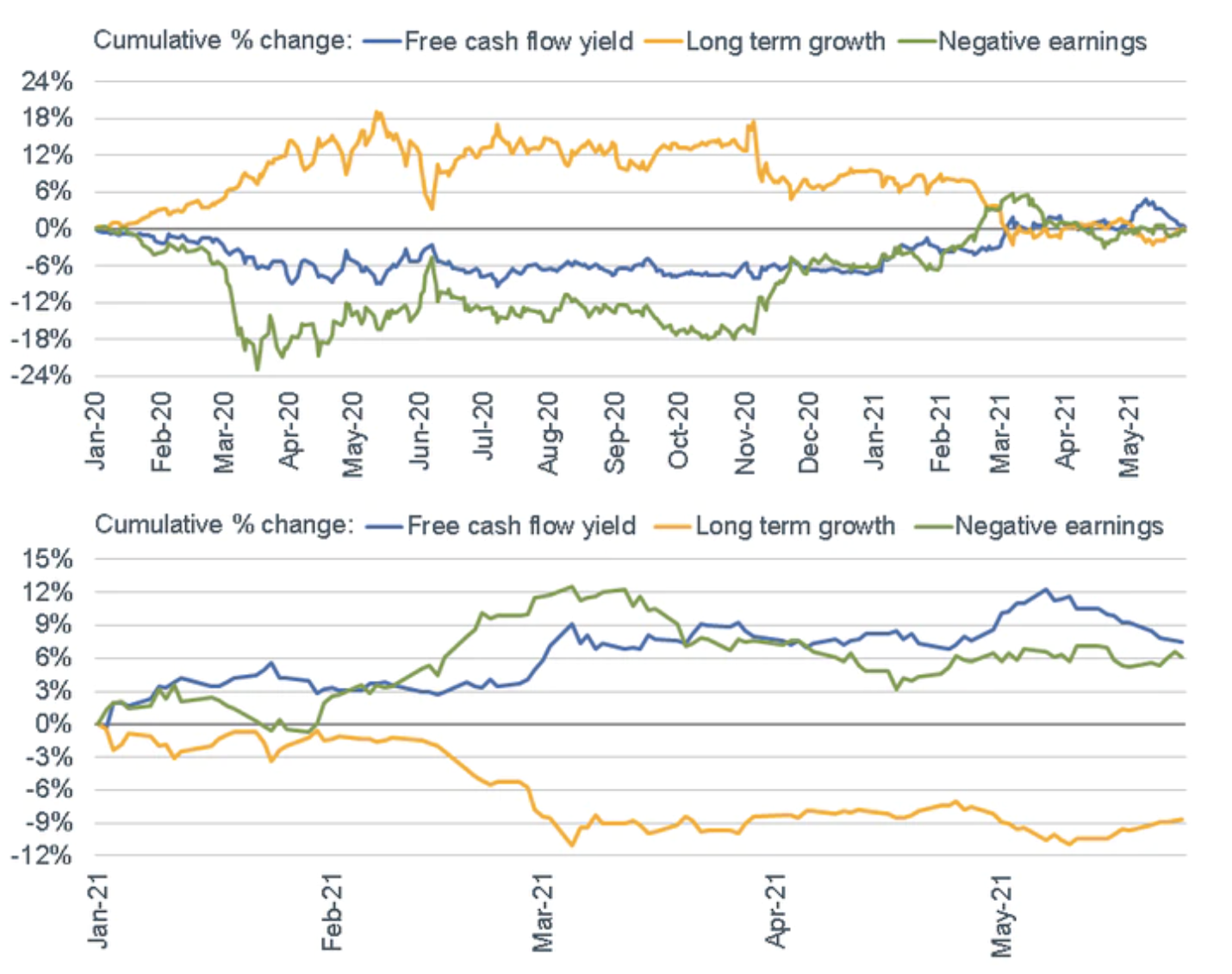

This year has been characterized by several shifts in leadership. As highlighted in the charts below; while growth factors dominated performance from the market’s low in March 2020 to early-November last year; this year has been a different story. Seen in the second, shorter time frame chart, traditional value factors—like free cash flow yield—as well as negative earnings (where “leverage” is greatest when growth surges), have significantly outperformed the long-term growth factor.

2020 Growth; 2021 Value

Source: Charles Schwab, Cornerstone Macro, as of 5/28/2021. Factors based on sector-neutral S&P 500. Free cash flow yield is defined as the last twelve months of free cash flow divided by the share price. Long-term growth is defined as mean estimated five-year earnings per share growth. Negative earnings is defined as last twelve months of net income less than 0. Past performance is no guarantee of future results.

By the way, stocks that screen well on traditional value factors have tended to be outperforming those that screen well on traditional growth factors across all 11 S&P 500 sectors. In fact, the spread of outperformance is greater among the three “growthiest” sectors: Technology, Communication Services and Consumer Discretionary. In other words, it’s paid to be value (factor)-oriented, even when looking within traditional growth sectors.

In sum

Looking ahead to the second half of 2021, we think there are some notable market risks associated with the combination of peak economic/earnings growth rates, higher inflation, Fed policy and some stretched sentiment conditions. Specific to Fed policy, the Fed has been trying to establish “hotter” inflation to counteract the negative effects of inflation having run “cold” for so long. This is a unique period relative to history; with the Fed actively pursuing higher inflation. Formally, the Fed has shifted its reaction function associated with both its mandates—inflation and employment—from being “outlook” based to “outcome” based. In essence, it means the Fed has gone from driving via the windshield to driving via the rear-view mirror. They might still get where they want to go; but there is the risk that markets decide they’re getting behind the inflation curve.

For the stock-pickers out there, we suggest a “hybrid” approach—with an eye toward sustainable growth, but at reasonable valuations—as well as quality factors, like balance sheet strength. For the asset allocators out there, we suggest this is a time for discipline; including around diversification (across and within asset classes) and periodic rebalancing. As a reminder, just as panic is not an investing strategy, neither is FOMO.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All