The stock market could use some mouthwash. Breadth in the S&P 500 remains fresher than either the NASDAQ or Russell 2000, but it’s also been deteriorating. Generally, market breadth indicators highlight the percentage of stocks in an index trading above moving averages; or the number of stocks rising relative to the number that are falling—often incorporating volume statistics as well. An analogy often used to explain why breadth matters comes from the battlefield. When the generals are on the front line; but the soldiers are lagging behind, the force is less powerful than when the soldiers are on the front line alongside the generals.

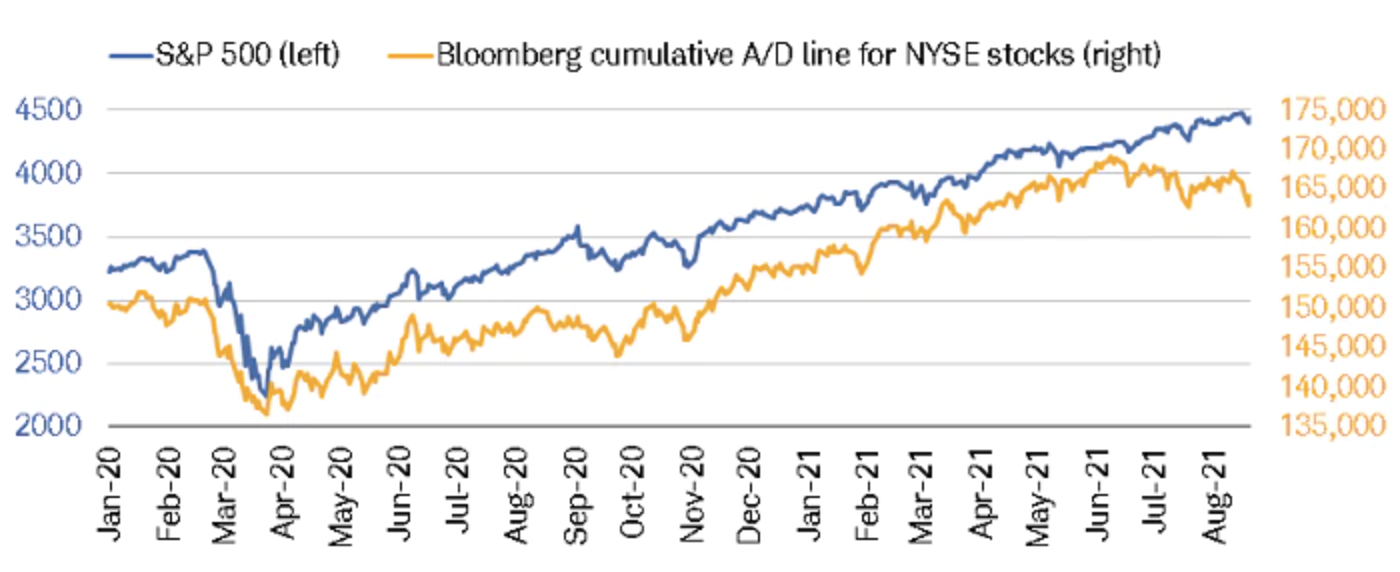

Let’s start with a very broad look at breadth. As shown in the chart below, although the S&P 500 traded at an all-time high as recently as last week, the cumulative advance/decline (A/D) line for the broader NYSE universe peaked on June 11 this year. The divergence between the two looks similar to early-September last year—the point at which it was mostly the “big 5” stocks within the S&P 500 (the “generals”) that had powered the S&P 500 to its September 2, 2020 high.

NYSE A/D Struggling

Source: Charles Schwab, Bloomberg, as of 8/20/2021. Cumulative advance/decline (A/D) line is the cumulative sum of the daily difference between the number of stocks on the New York Stock Exchange (NYSE) advancing and declining in a single day.

Spotlight on major averages

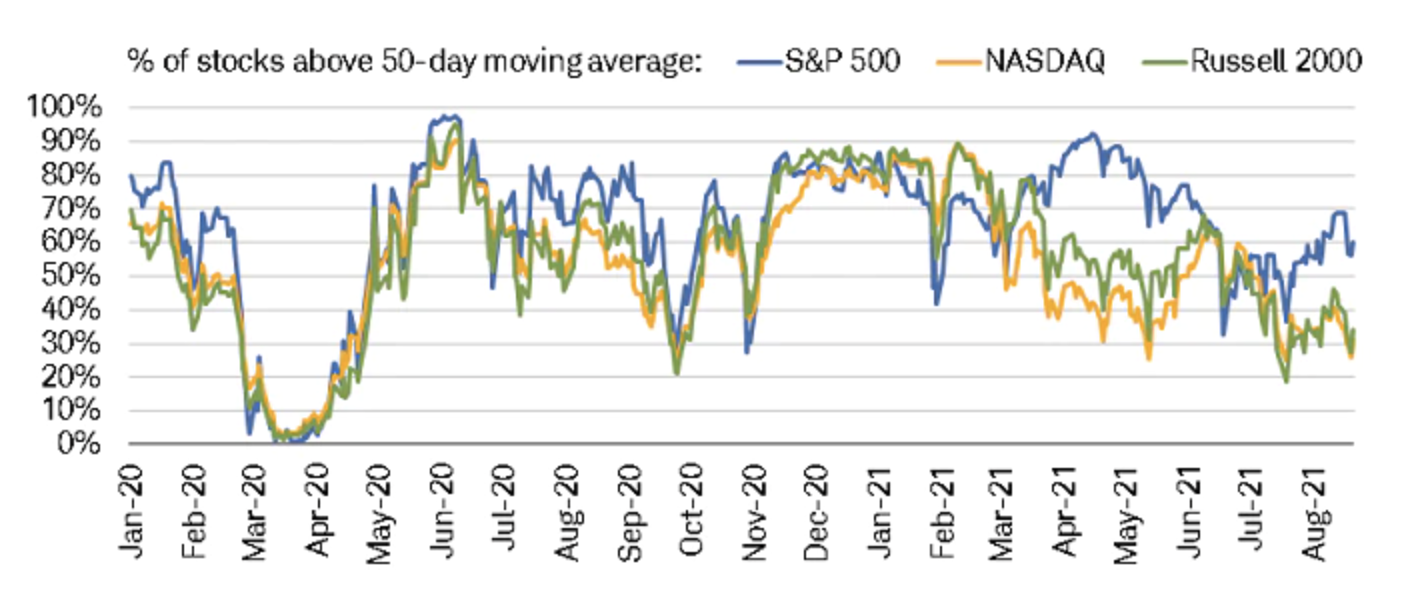

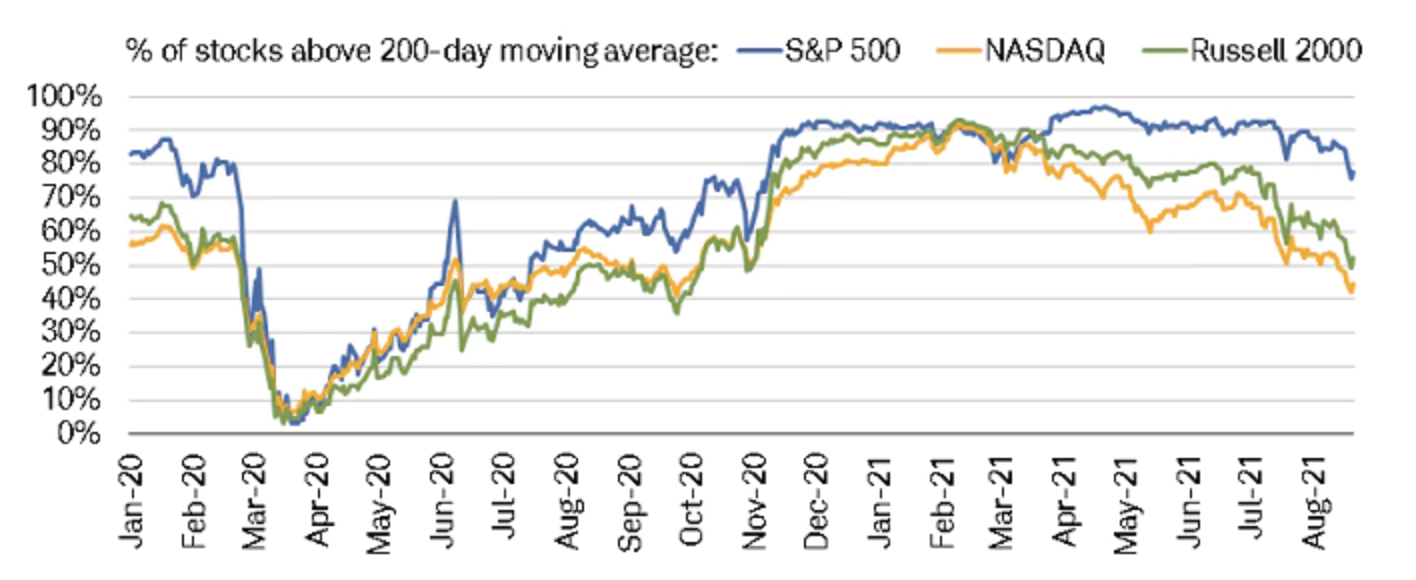

As shown in the first chart below, the percentage of S&P 500 stocks trading above their 50-day moving averages peaked in April, troughed in June, improved until recently, but has come under pressure again. The same can’t be said for the NASDAQ and Russell 2000, which both peaked in early February, since which time they’ve generally been descending. Relative to their 200-day moving averages (DMA), all three indexes have been generally trending lower since April, as shown in the second chart below.

50-DMA Breadth

Source: Charles Schwab, Bloomberg, as of 8/20/2021. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

200-DMA Breadth

Source: Charles Schwab, Bloomberg, as of 8/20/2021. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

In the case of the NASDAQ, new lows have exceeded new highs recently—even though the index hit an all-time high as recently as August 5 this year. This is strikingly different than the massive breadth thrust for the NASDAQ from last November through this past February.

Sector breadth/volatility

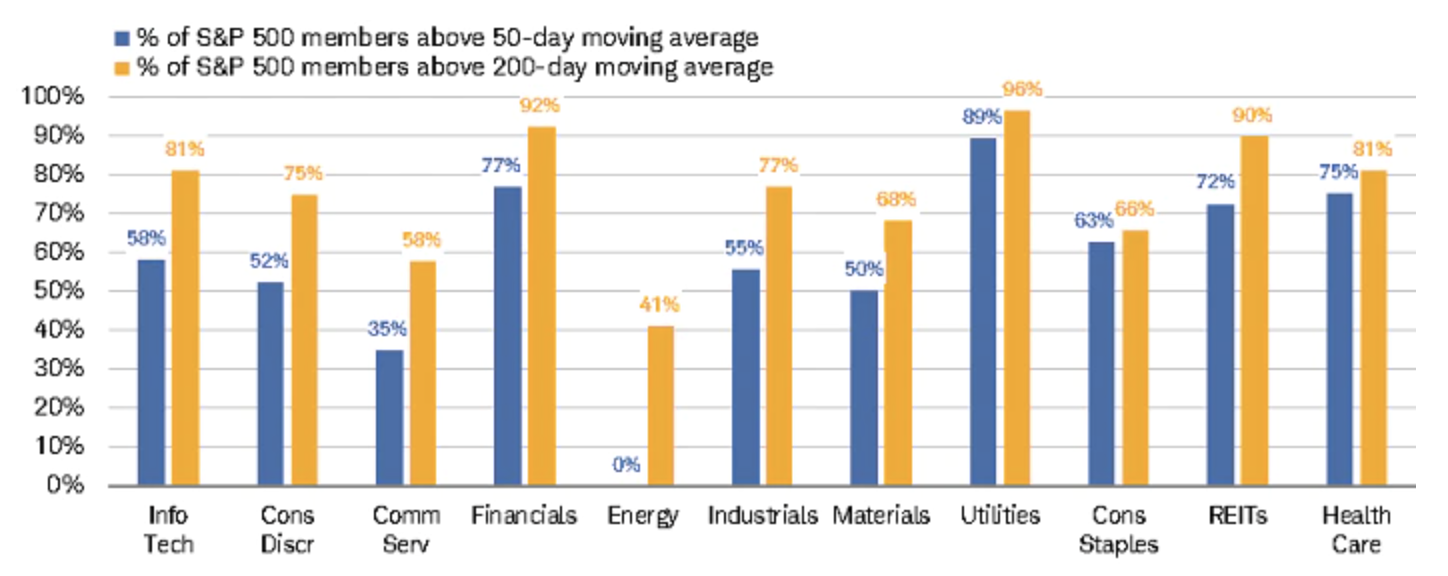

At the sector level, as shown below, Energy’s breadth stinks the most; while given the market’s recent bias toward classic defensive areas, Utilities have the freshest breadth (followed by Financials).

Sector Moving Average Breadth

Source: Charles Schwab, Bloomberg, as of 8/20/2021. Past performance does not guarantee future results.

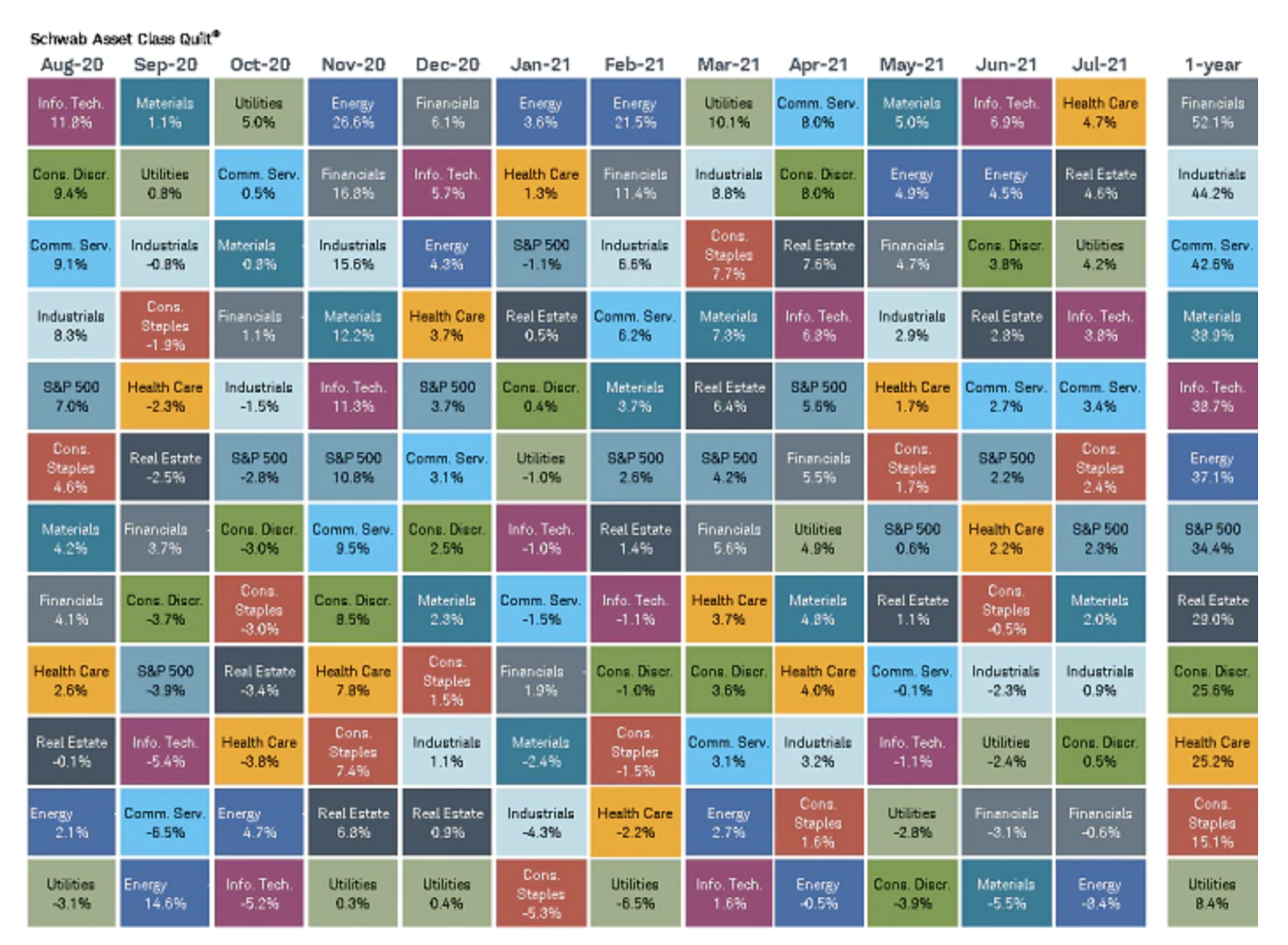

The bias recently toward traditional defensives likely reflects growing concerns about COVID’s Delta variant’s impact on economic growth; but also the peak in the growth rate for both the economy and earnings, as well as fading fiscal and monetary stimulus. All year, we have been highlighting fairly rampant sector-based volatility, shown in our sector “quilt” chart below—which ranks each S&P 500 sector from best-to-worst on a monthly basis. This volatility, which we expect will persist, is one reason why we have only one “outperform” rating on the S&P 500’s 11 sectors—Healthcare. To read more on our sector ratings, see HERE

Monthly Sector Rankings

Source: Charles Schwab, Bloomberg, as of 7/31/2021. Sector performance is represented by price returns of the following 11 GICS sector indices: Consumer Discretionary Sector, Consumer Staples Sector, Energy Sector, Financials Sector, Health Care Sector, Industrials Sector, Information Technology Sector, Materials Sector, Real Estate Sector, Communication Services Sector, and Utilities Sector. Returns of the broad market are represented by the S&P500. Returns assume reinvestment of dividends, interest, and capital gains. Indices are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

Calm before storm?

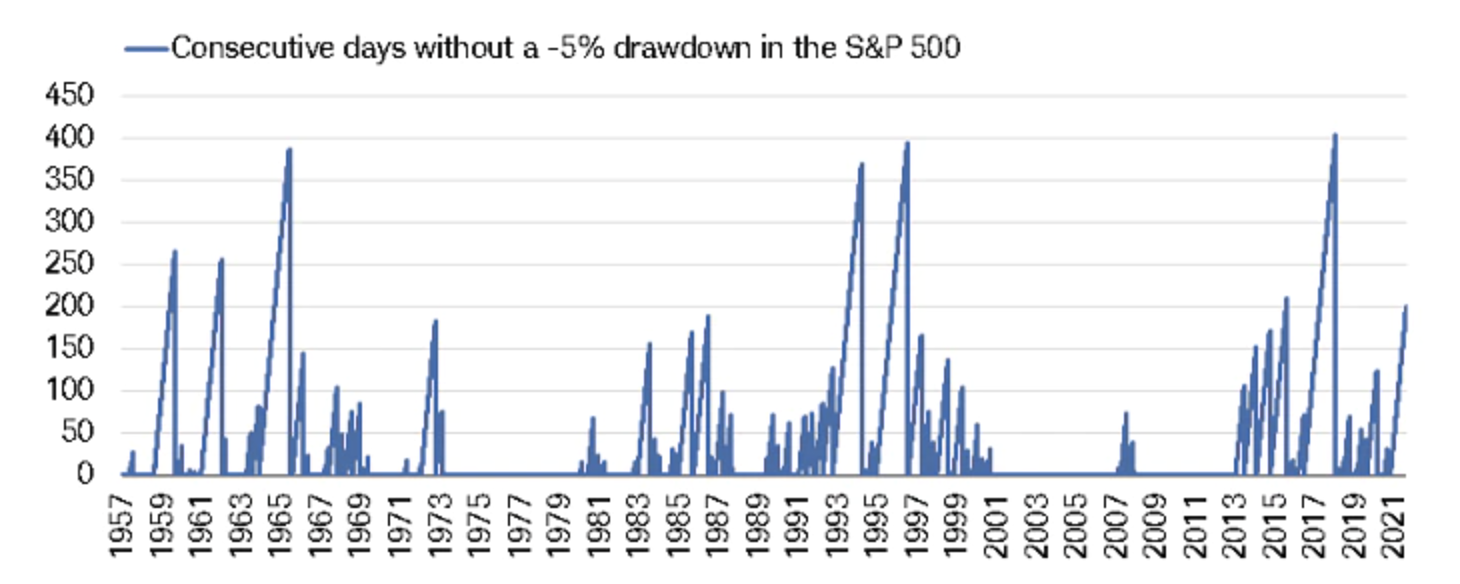

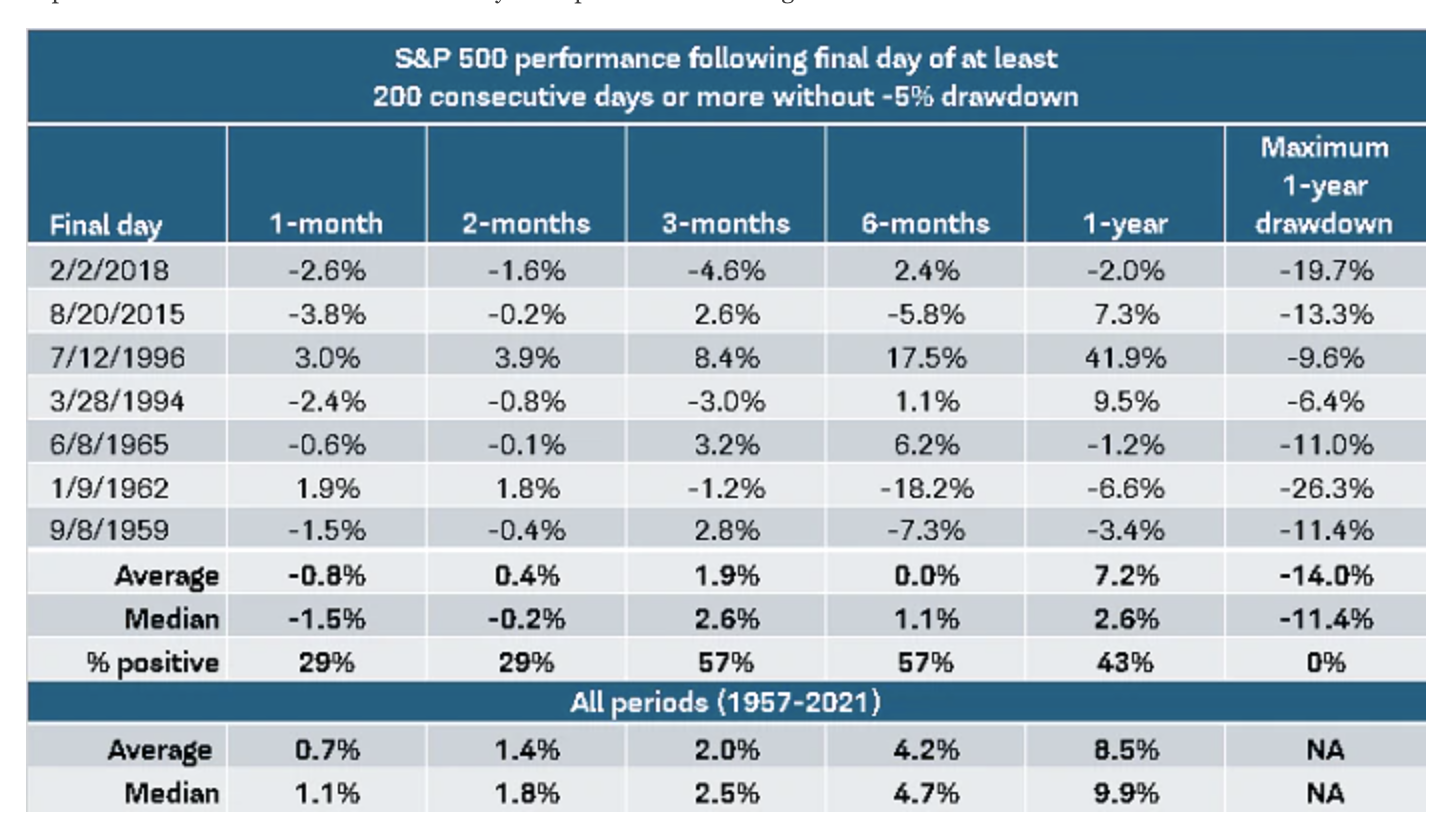

Notwithstanding the aforementioned risks associated with deteriorating breadth, the S&P 500 has gone 200 days without at least a 5% drawdown, as shown in the first chart below. The stretch is not yet near prior peaks—the three most significant having occurred in 1965, 1994 and 1996—but historically-high, nonetheless. The maximum drawdown this year so far has been -4.2%. Since the S&P 500’s inception in 1928, there have been three calendar years with a maximum drawdown even less than that: 1995 (-2.5%), 2017 (-2.8%) and 1964 (-3.5%). It begs the question whether the market is “overdue” for a pullback, so the table below the chart may help answer that question by looking at the S&P 500’s “modern” history (the index moved to 500 stocks in 1957).

Long Span Without Pullback

Source: Charles Schwab, Bloomberg, as of 8/20/2021. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Source: Charles Schwab, Bloomberg, as of 8/20/2021. Historically there have been seven instances of the scenario as illustrated in the above table. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

As shown above, although the sample size is not significant, prior 200+ day stretches without at least a 5% drawdown ended with mixed-to-fairly weak subsequent performance shorter-term. Over the subsequent one-to-two months, returns were positive less than 30% of the time; with both average and median returns below the all-period average and median. Longer-term, the results were mixed, but mostly weaker than the all-period average/median returns. As shown in the final column, over the subsequent one-year period, the maximum drawdowns ranged from -11% to -26%.

Spec drawdowns

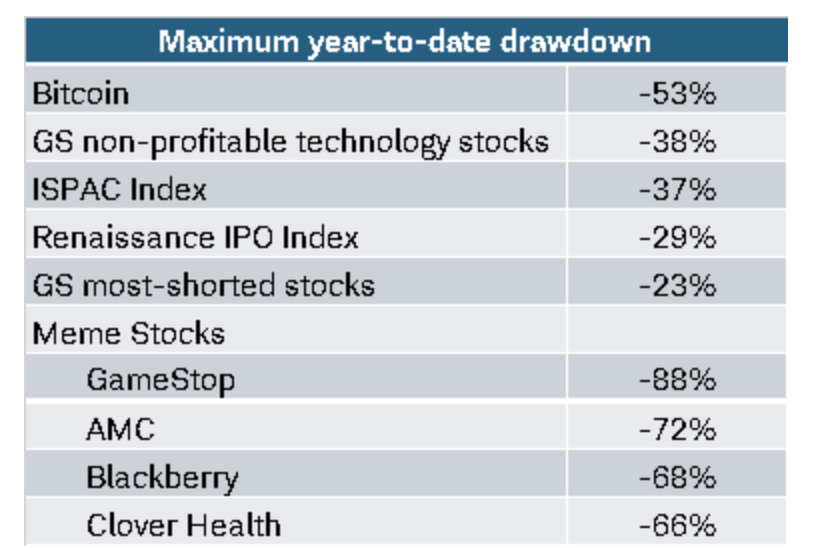

Increasingly, I’ve been asked by clients during our many virtual events about whether the U.S. stock market is in a bubble akin to 1999-2000. My answer has been a bit more nuanced than a simple yes or no. The tech bubble burst in spectacular fashion in March 2000, driven by absurd valuations and massive speculative excess. Presently, at least for the S&P 500, valuations are less-stretched courtesy of the epic rebound in earnings (the surge in the E has resulted in a significant move down in the P/E).

But there has been significant speculative excess in less-traditional pockets of the market. Since late-2017, I’ve been calling these pockets “micro bubbles.” These pockets have experienced drawdowns at some point this year that have been much more severe than the traditional indexes’ drawdowns. Here are some examples of market segments or securities with greater-than-bear market level maximum drawdowns at some point this year:

Source: Charles Schwab, Bloomberg, as of 8/20/2021. For illustrative purposes only. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results. Goldman Sachs (GS) non-profitable technology basket consists of non-profitable U.S.-listed companies in innovative industries. Technology is defined quite broadly to include new economy companies across GICS industry groupings. ISPAC Index is a passive rules-based index that tracks the performance of the newly listed Special Purpose Acquisitions Corporations (“SPACs”) ex- warrant and initial public offerings derived from SPACs since 8/1/2017. Renaissance IPO Index tracks US-listed newly public companies that are weighted by float, capped at 10%, and removed after two years. Goldman Sachs (GS) most-shorted basket contains the 50 highest short interest names in the Russell 3000; names have a market cap greater than $1 billion.

In sum

As summer winds down, we soon head into September—historically the worst month for stocks in terms of average performance. Aside from seasonality, there are several risks with which the market is confronting … including deteriorating breadth, fading monetary and fiscal stimulus, peak earnings/economic growth rates, and of course the Delta variant. Individually or collectively, though, they should not be taken as a “get out” message. For stock pickers out there, we would recommend a focus on quality via factor screening; both within growth and value indexes.

Important disciplines to heed in the current environment are diversification—both within and among asset classes—and periodic rebalancing. With regard to rebalancing, it’s one of the most beneficial disciplines in that it forces us to do what we know we’re supposed to do—add low, trim high. Notice I adjusted that from the classic “buy low, sell high” adage; which can infer an all-or-nothing strategy. Frankly, investors should never think of investing as either “get in” or “get out.” That is gambling on moments in time; while investing should always be a disciplined process over time.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Investing involves risk including loss of principal.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Diversification and rebalancing portfolio strategies cannot ensure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

©2021 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

(0821-1T7T)

© Charles Schwab

Read more commentaries by Charles Schwab