Focus on the second quarter has been particularly acute of late, not least due to expectations of a continued slowdown in both gross domestic product (GDP) and corporate earnings growth. As of July 19th, the Atlanta Fed is estimating that GDP declined by 1.6% (quarter-over-quarter at an annualized rate) in the second quarter. That would mark the second consecutive quarterly decline (as a reminder, that is not the definition of a recession), which hasn't happened since the pandemic-induced recession in early 2020.

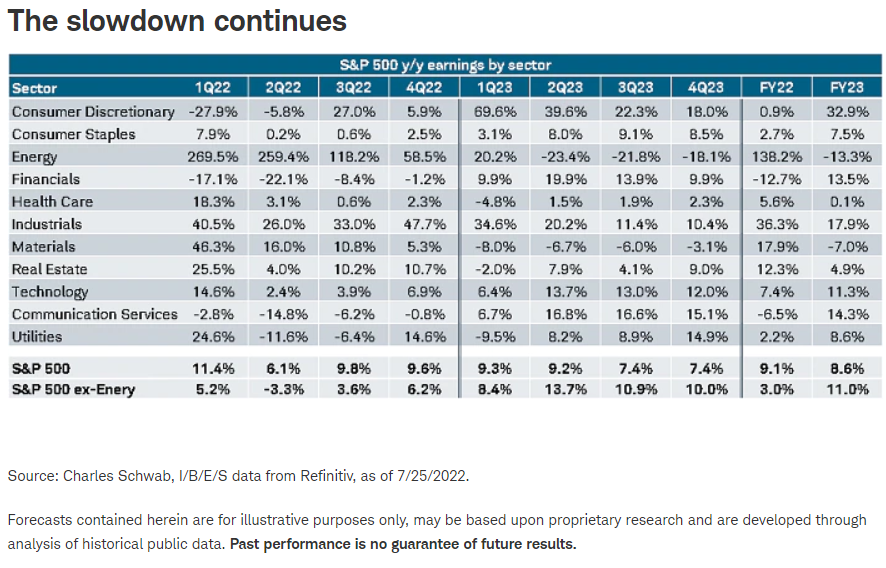

Per Refinitiv, the "blended" year-over-year growth rate for second-quarter S&P 500 earnings is 6.1% (blended refers to the combination of actual earnings for companies that have already reported, and consensus estimates for companies yet to report). Excluding the Energy sector, earnings are expected to decline by 3.3%, the first contraction in ex-Energy growth since the third quarter of 2020. Of the 107 companies that have reported, 74.8% have reported above analyst estimates, which compares to a long-term average of 66% and the prior four quarters' average of 81%.

At the sector level, results have thus far been mixed and, as you can see in the table below, underscore a slowdown. Sectors such as Consumer Discretionary, Financials, and Communication Services are expected to see another decline in growth, and rates for traditional defensives like Consumer Staples, Health Care, and Utilities have come down sharply.

As we've noted for the better part of the past year, the best days for earnings growth are certainly behind us. Sky-high double-digit growth rates were unsustainable (earnings growth reached a peak of 96% in the second quarter of 2021), and the bar was set quite low for a good portion of the rebound coming out of the worst phases of the pandemic.

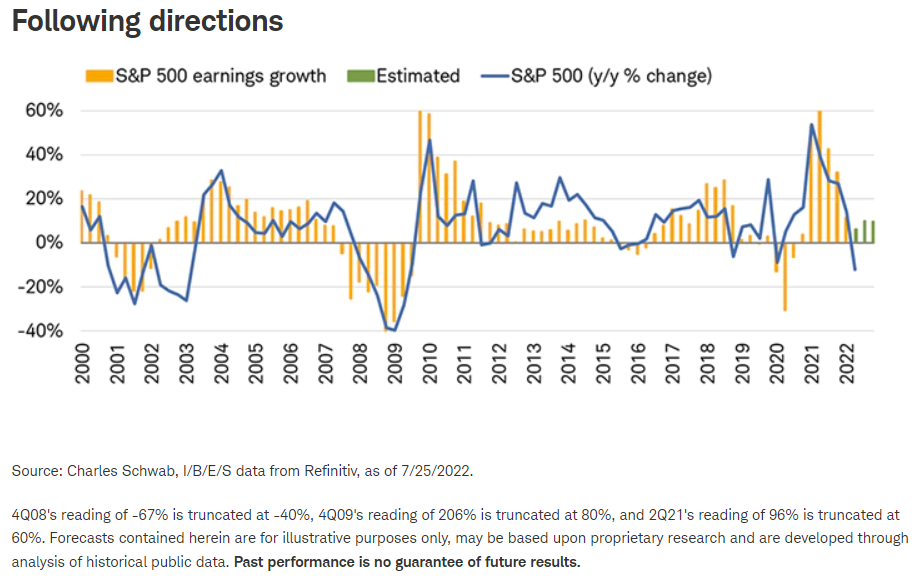

Not only have analysts now kept the bar too high, but the macro environment has shifted unfavorably for the market, helping send major indexes into bear territory this year. As you can see in the chart below, year-over-year changes in price and earnings growth have tracked closely over the past two decades. While the market's plunge into negative terrain doesn't suggest overall earnings growth must go negative, we still think there are risks to the downside. Plus, as mentioned, the growth rate excluding the Energy sector (which is expected to see triple-digit percentage profit gains) is in the red.

Following directions

In keeping with the trend over the past year-and-a-half, investors have been rewarding companies that are beating estimates, while punishing those that have missed. As shown in the chart below, the average S&P 500 member has outperformed the broader index by 0.5% when beating analysts' expectations, while the average decline for a miss has amounted to -2.3%.

The beat/miss trend thus far shows that the market has grown less excited (in comparison to the first quarter) about companies outpacing estimates. While we still have a considerable portion of the reporting season ahead of us, price action for now suggests that attention will continue to shift to the strength of companies' outlooks as opposed to how well they performed in the second quarter. In other words, forward-looking guidance and revisions have taken over as drivers of market action, especially with heightened fears of a looming recession.

The math of long revision(s)

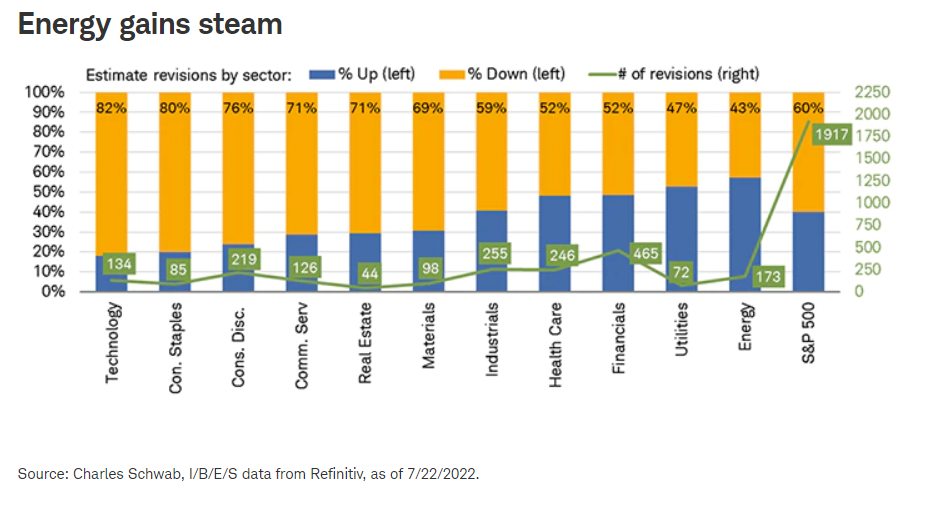

Among the reasons for expectations of a less-than-rosy backdrop for earnings growth is the significant downshift in positive earnings revisions. As shown in the chart below, the share of S&P 500 members with positive three-month revisions has fallen by a significant degree over the past year (from nearly 70% to just above 30%). Higher input costs, the sharp increase in interest rates, and waning consumer demand have weighed on the number of upgrades; unfortunately, that historically portends weakness for both the market and corporate earnings. To be sure, the percentage of positive revisions hasn't fallen to prior recessionary troughs, but the speed of the decline has been notable and bears watching if downward momentum persists.

Zooming in on individual sector revisions for the current quarter, perhaps unsurprisingly, Energy is leading in upgrades while Tech commands the largest share of downgrades. Energy's strength comes courtesy of the rise in oil prices and lingering (though fading) positive impact from the broader reopening of the economy. For growth-dominated Tech and its peers (Communication Services and Consumer Discretionary), upgrades have faded—not least because of the sharp hit those sectors are facing from higher rates and the unwinding of the stay-at-home trade.

It's worth noting that the Consumer Staples sector is near the bottom of the revisions leaderboard. Traditionally considered a defensive play in bear markets, it has come under immense pressure as higher costs and compressed profit margins have weighed on companies' outlooks. Increasingly sour forward guidance bears watching as the reporting season continues, especially because the sector's forward price-to-earnings (P/E) ratio has surpassed the S&P 500's forward P/E by nearly the widest margin in history. It might be a defensive play, but it comes at a price.

Goldilocks (for now) and the three bears

For virtually the entire year to date, the S&P 500's decline has been driven by multiple contraction. P/E ratios have been crushed, led by growth-oriented sectors that were incredibly expensive at the beginning of the year. It's a textbook move when considering the environment of hotter inflation and an aggressively hawkish Federal Reserve (Fed). With valuations now having corrected sharply, attention has shifted to what lies ahead for the E in the P/E.

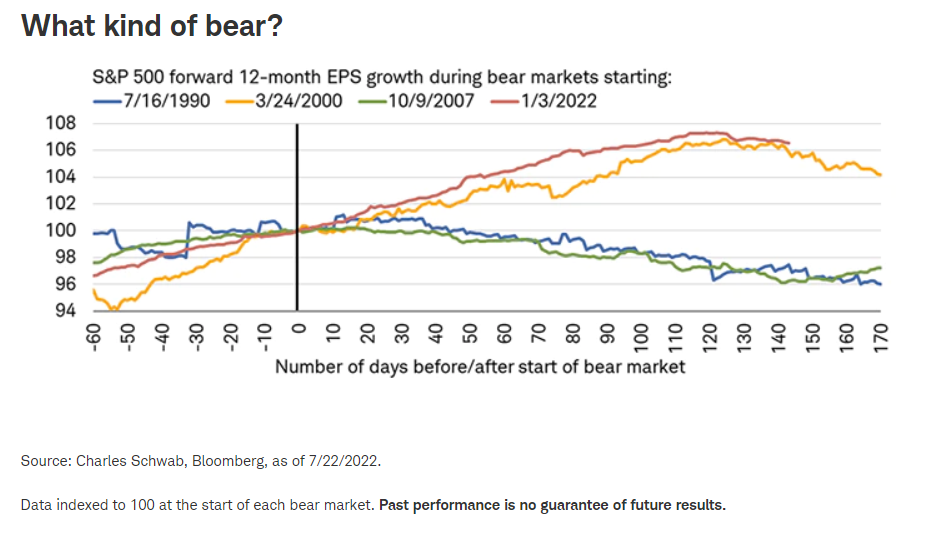

Our forward earnings data begins in 1990, which allows us to measure the trajectory of estimates in the past three bear markets—that is, those that came before the COVID bear, which was far too swift and sharp to use as a fair comparison. As shown in the chart below, the current earnings path is strikingly similar to the one seen in the early-2000s dotcom bust. Though the market peaked in March 2000, it wasn't until September of that year that forward earnings growth peaked (it didn't bottom until January 2002). Forward earnings growth corrected much faster after the market's peak during the Global Financial Crisis (GFC) and 1990 recession.

Any study of prior bear markets and recessions always warrants the disclaimer that the sample size with which we are working is incredibly small—not to mention the fact that each downturn has its own unique set of flavors. Indeed, the recessions in 1990 and 2001 were nearly identical in duration; yet the S&P 500's maximum drawdown in 1990 was -20%, while it fell by -49% at its worst point in 2002. Conversely, the maximum drawdown during the GFC was -57%, and the severity of the recession was of a completely different (and disastrous) scale in terms of duration and depth.

One leg down, one to go?

Earnings season will heat up quickly this week but results thus far suggest growth in the second quarter will look underwhelming in relative and absolute terms. Though forward earnings estimates have started to crest, we are likely still in the early phases of the downgrade cycle. Stocks' weakness thus far may have priced in some of the declines in second-quarter profits, but what matters more is how much companies see their bottom lines getting hit later this year—a risk that may be the driver of the next bout of weakness for stocks.

The unwinding of the stay-at-home bubble, coupled with a still-hot 40-year high in inflation and the Fed's aggressive rate hikes, has exacerbated the economy's deceleration this year. Growth in profit margins has been arrested, and with demand now stalling (or outright contracting) in certain sectors, hiring freezes and layoffs have gained steam. If demand falls at a faster rate and inflation takes longer to subside, earnings will undoubtedly be at further risk.

As a broader downshift in growth expectations has come to fruition, high-quality segments of the market have maintained their standing as consistent havens. We think their leadership will persist, and thus continue to encourage stock-picking-oriented investors to focus on factors such as positive earnings revisions, low volatility, and strong free cash flow. Strong, countertrend rallies may look tempting, but the inability of key leading economic indicators to turn higher warrants a healthy dose of patience and prudence.

© Charles Schwab

Read more commentaries by Charles Schwab

Following directions

Following directions