U.S. Outlook: How Many More Times, Fed?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDon't fight the Fed. The well-known, but sometimes not-heeded, expression was originally coined by my first boss and mentor, the late-great Marty Zweig. Jerome Powell, the current chair of the Federal Reserve, has been doing (or trying to do) yeoman's work getting "the market" to fully digest what the Fed feels is necessary to bring inflation down meaningfully and sustainably. Powell, among other Fed officials, has seemingly shifted his attention from the rear-view mirror to the windshield. Inflation is a lagging indicator, but the impact of monetary policy changes is in the future (with long and variable lags).

This outlook—which is longer than usual (sorry!)—was published a couple of weeks prior to the December meeting of the Federal Open Market Committee (FOMC)—with current expectations showing a higher likelihood the Fed will raise the fed funds rate by 50 basis points, but a small chance of another 75-basis-point hike. That would bring the year-end rate to either a range of 4.25% to 4.5%, or 4.5% to 4.75%. However, importantly, the combined impact of what has been record aggressiveness in terms of rate hikes and the ongoing reduction of the Fed's balance sheet (QT, or quantitative tightening), means the effective tightening is greater than if only the rate side were taken into consideration.

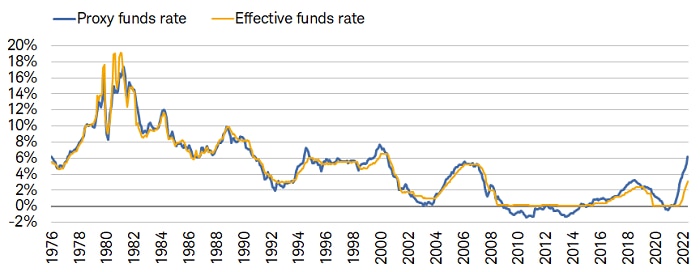

Proxy rate

As per recent research by the Federal Reserve Bank of San Francisco, when the FOMC "uses additional tools, such as forward guidance or changes in the balance sheet, these policy actions affect financial conditions, which the proxy rate translates into an analogous level of the federal funds rate." The Proxy Rate, shown below, "can be interpreted as indicating what federal funds rate would typically be associated with prevailing financial market conditions if these conditions were driven solely by the funds rate."

Proxy rate > effective rate

Source: Charles Schwab, Federal Reserve Bank of San Francisco, as of 10/31/2022.

The proxy rate can be interpreted as indicating what federal funds rate would typically be associated with prevailing financial market conditions if these conditions were driven solely by the funds rate. The effective funds rate is the interest rate depository institutions charge each other for overnight loans of funds.

Given the tightening already in play, with the proxy rate north of 6%, there is a risk of a Fed overshoot. That would be the scenario that could bring rate cuts sooner rather than later. But it would likely only occur with a more significant deterioration in the labor market and/or the broader economy. The Fed is unlikely to pivot to rate cuts simply due to inflation continuing to recede. Perhaps the best way to think about next year is this: more pain near-term could result in an easier Fed in the latter part of the year; but less pain near-term likely results in tighter-for-longer monetary policy. Getting the best of both worlds does not appear to be in the cards.

Not the 1970s

As an aside, we have regularly pointed out that although inflation hit a 41-year high in mid-2022, this is not a repeat of the persistent stagflation era of the 1970s. Among other numerous differences, during the lead-in to that era, government outlays had fueled a two-decade acceleration in M2 money supply. In this cycle, there was only a short one-year surge in federal outlays and M2 growth. The Fed understands the distinctions; however, they have been clear in expressing a desire to avoid the fits and starts of monetary policy that characterized the era of the 1970s—which in turn fueled fits and starts of inflation. That ultimately led to Fed Chair Paul Volcker to have to "pull a Paul Volcker" and tighten to such a degree as to bring on back-to-back recessions in the early 1980s.

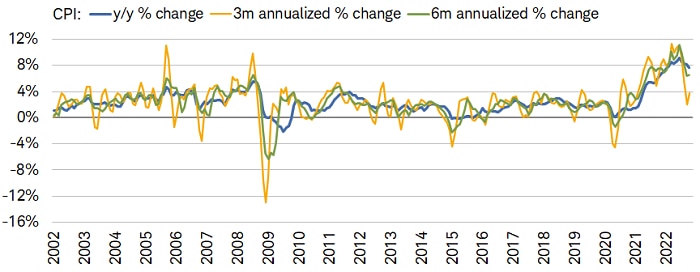

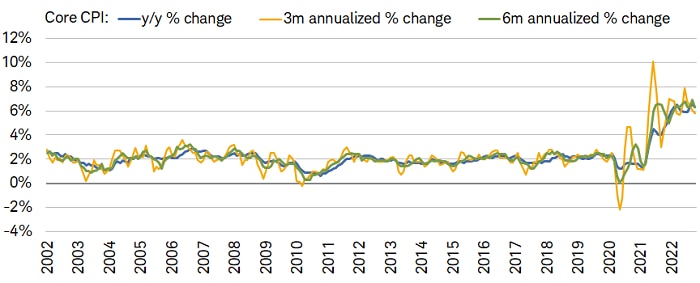

Inflation and financial conditions at odds?

Using both three- and six-month annualized changes, shown below, it's clear that the trend of inflation is heading lower for both the headline and core Consumer Price Indexes (CPI). Even the sticky shelter component of the CPI should begin to roll over—perhaps as early as the first quarter of 2023—due to the fact that many real-time rental indexes (like those from Zillow, Real Page, etc.) have already decisively moved lower.

Promising trends in CPI

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 10/31/2022.

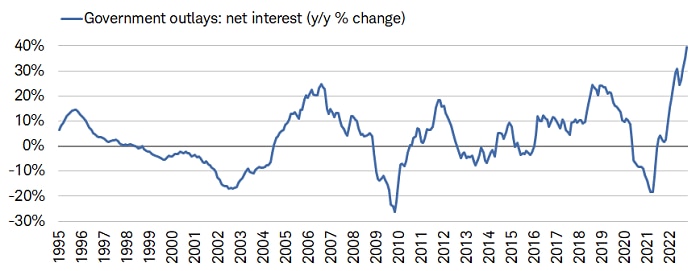

We are fond of pointing out that when it comes to economic/inflation data (especially as it relates to stock market behavior), "better or worse typically matters more than good or bad." However, in the case of inflation and interest rates, levels pose ongoing risks for the economy in 2023, especially via the connection point of housing, but also as it relates to rising federal debt servicing costs. As shown below, U.S. government outlays on net interest expense have surged over the past year. Whereas concerns about the sustainability of government debt took a back seat for a while to COVID and inflation concerns, we expect this will become a larger part of the conversation in 2023.

Government's debt burden

Source: Charles Schwab, Bloomberg, as of 10/31/2022.

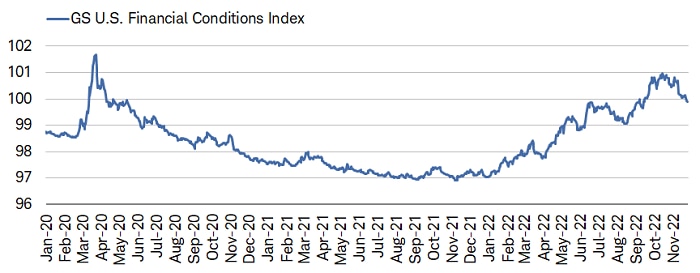

More Fed calls?

In the meantime, a near-term rub for the Fed has been the loosening of financial conditions, shown below—decidedly not what the Fed wants to see while trying to bring inflation down toward the 2% target. What we may continue to see, at least in the early part of 2023, is the emergence of what we've been labeling the "Fed call." As a reminder, there was historically the assumption of a "Fed put," given the several times the Fed stepped in either via jawboning (specific dovish language in speeches or press conferences), or via an actual shift to looser policy, due to riots in the financial markets.

It's different this time. The Fed has been distinguishing between financial market volatility and financial system instability, with only the latter likely to trigger a shift in policy. In fact, for now, a weaker equity market helping to tighten financial conditions (not to mention rein in speculative excess) is a feature of Fed policy, not a bug. Assuming a continuation of the year-end rally that began in mid-October, the Fed may be forced to push back on related enthusiasm (a "Fed call") if financial conditions continue to loosen. This is precisely what happened last August when Powell had to "talk down" the stock market's enthusiasm around a perceived coming pivot by the Fed.

More tightness needed?

Source: Charles Schwab, Bloomberg, as of 11/25/2022.

Goldman Sachs (GS) Financial Conditions Index (FCI) is defined as a weighted average of riskless interest rates, the exchange rate, equity valuations, and credit spreads, with weights that correspond to the direct impact of each variable on GDP.

Threading the needle

The benign case is that the Fed can successfully bring inflation down to (or near) its target of 2%, without causing a significant deterioration in the unemployment rate and/or the economy more broadly. Given that the real fed funds rate remains in negative territory, courtesy of every traditional measure of inflation being above it, the Fed likely has more work to do—at least in 2023's first half.

A recent post from the National Bureau of Economic Research (NBER)—the official arbiters of U.S. recessions—noted this: "If the behavior of either [the unemployment rate and the job vacancy rate] proves less benign, then reducing inflation [to target] is likely to require higher unemployment than the Fed anticipates." Within the same analysis, the NBER estimates that the unemployment rate would have to move up to 7.5% to return inflation to target. Reality may be something in between the current sub-4% rate and the NBER's estimate.

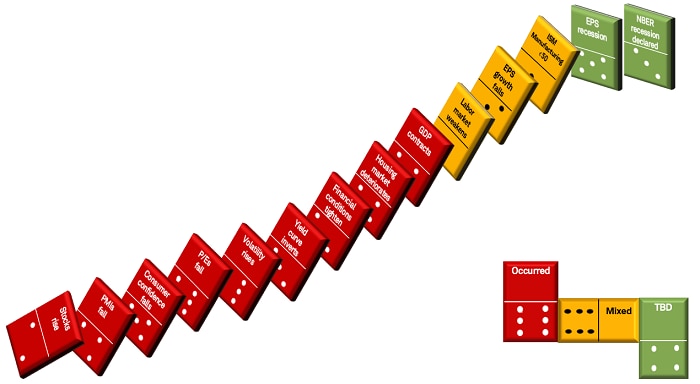

What say you, dominoes?

It is crucial to exercise caution when comparing any two economic cycles in hopes of identifying specificity around the timing of turning points. While each cycle's end throughout history has been unique and marked by a particular event(s)—i.e., the tech bust in 2000, the Global Financial Crisis from 2008-2009, and the pandemic in 2020—there are consistent signals to be found within leading economic indicators. The visual below identifies the economic "dominoes" that tend to fall after the Fed embarks on a tightening campaign. For the current cycle, the red dominoes are events that have already occurred, the yellow are mixed, and the green have yet to happen.

Not a fun game of dominoes

Source: Charles Schwab. For illustrative purposes only.

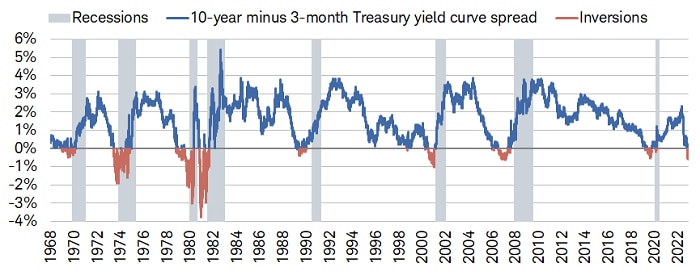

In a way, this represents the uniqueness of the current cycle: one characterized by rolling recessions. Certain segments of the economy entered firm recessionary territory in 2022—most notably, housing, several goods-oriented segments of the economy, consumer confidence, and CEO confidence. Other well-watched indicators point firmly toward recession in 2023, like the inversion of the yield curve, shown below.

Inversions lead recessions

Source: Charles Schwab, Bloomberg, as of 11/25/2022.

There are obviously other indicators—notably associated with the services side of the economy and labor conditions—that have not (yet) suffered the same fate, and still point to growth. However, we have recently pointed out several cracks under the surface of the labor market—and will touch on that in later paragraphs—but for now, it is likely strong enough to suggest the economy is still growing.

Recessionary signals abound

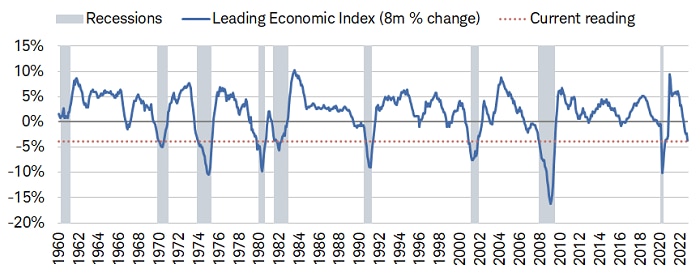

A coming (or already in progress) recession shouldn't come as a surprise given the Leading Economic Index (LEI) from The Conference Board has had an eight-month change consistent with every recession going back to 1960, as shown below. Given the narrowing in positive breadth of the LEI's subcomponents, we see further downside for the index into at least the first half of 2023. Momentum reversals have been swift in the past, but nothing about today's backdrop is suggestive of a near-term trough in leading indicators.

Race to the bottom

Source: Charles Schwab, Bloomberg, The Conference Board, as of 10/31/2022.

The NBER's declarations of recessions have always happened after they had already started; and were that to occur in 2023, it could further dent confidence. Job growth was central to the economy's ability to withstand numerous headwinds in 2022. Yes, a tighter labor market and stronger nominal wage growth have helped support higher inflation, but strong nominal incomes have also given consumers some breathing room as the economy has weakened. For now, that has arrested the spillover from leading indicators like housing to coincident indicators like payrolls.

Unfortunately, consumers have also drawn down a significant amount of their savings and have hit the borrowing window to an increasing degree (even among the higher-income tiers). In fact, per Ned Davis Research, other than households in the top income quintile, the share of outstanding consumer credit exceeds the share of demand deposits. Delinquency risk is rising, and if the labor market weakens noticeably and banks continue to tighten lending standards, consumers' moods and spending habits are likely to shift to a decidedly more cautious stance.

Subsurface labor market weakness set to float to the top

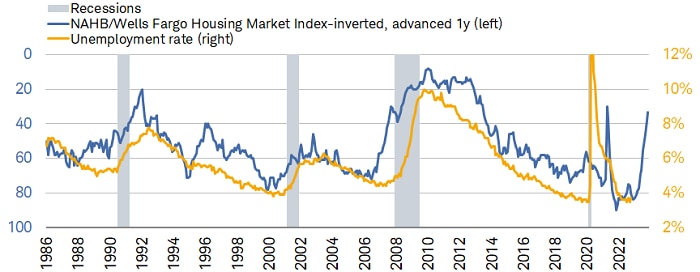

Unfortunately, there are several barriers to the labor market's upward trajectory. As shown below, one of the most reliable and consistent leading economic indicators—homebuilder sentiment—has fallen sharply this year (the series is inverted, so a move up is bad). The spike in mortgage rates and a supply-starved housing market have sent builders' moods into recession territory. That is typically the first housing—let alone economic—domino to fall. We can see that when comparing its level one year out to the unemployment rate today.

Ho-hum homebuilders

Source: Charles Schwab, Bloomberg. National Association of Home Builders (NAHB), as of 11/25/2022.

Unemployment rate as of 10/31/2022. Right y-axis is truncated for visual purposes.

History shows that weakness in housing sentiment has led moves in unemployment (both to the downside and upside) quite well. Does that guarantee that the unemployment rate will be near 9% a year from now? No; but it shouldn't be lost on investors that housing's track record of leading the economy is strong. In fact, the Fed is expecting (pushing for?) a move up in the unemployment rate. For now, the majority of labor pain has been witnessed in companies' weaker demand for employees, including fewer job openings and more hiring freezes. However, we expect more deterioration in headline labor market indicators in 2023, including payrolls and the unemployment rate—signaled by the surge in layoff announcements.

The Fed would ideally like to crush job openings and the rate at which employees quit, without triggering a recession, but we believe that's a very narrow opening in the needle they're trying to thread. We think it will only be a matter of time until the following cracks in the labor market widen:

- The divergence between the household and nonfarm payroll surveys—with the former showing 150k jobs created over the past seven months vs. the latter's 2.45m

- The increase in multiple jobholders—512k over the past year, which is near the upper range historically

- The large cut to both hours worked and outlooks for the length of the average workweek—leading to much lower average weekly pay

- The record addition of payrolls coming from the birth and death of businesses—455,000 (on a non-seasonally adjusted basis) as of October.

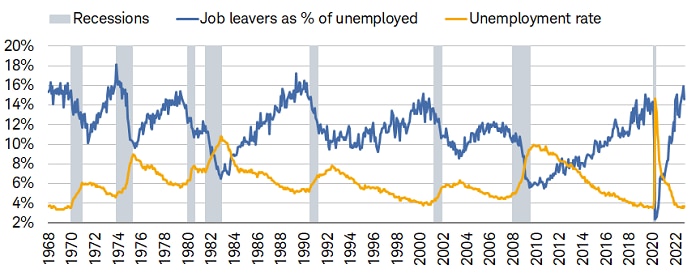

Not only is there a dearth of fundamental supports for the economy to escape a recession, but history isn't on the side of the Fed when it comes to soft landings. Economic bulls today will often point to the mid-1990s as successful, given the Fed hiked rates by 300 basis points from 1994-1995 and the economy averted a recession. In fact, during that hiking campaign, the unemployment rate moved down by nearly an entire percentage point.

However, as shown below, the key differences today are multifold: the quits rate among employees is higher and the unemployment rate is lower; the Fed has embraced a series of larger rate hikes this time around; and inflation is much higher. For now, workers still feel confident in their ability to leave their current job and/or find a new one, and companies have thus far been mostly reluctant to get rid of workers (save for tech and other related sectors that have started to lay people off).

However, we think an eventual move down in the percentage of job leavers will be consistent with a recessionary move up in the unemployment rate. Not only is history supportive of that, but the Fed is telling us in its own forecast for unemployment that a recession is expected. The central bank's latest expectation of 4.4% in 2023 would be a 0.7% increase from the current rate. In the long-term history of the unemployment rate, the average increase from its pre-recession trough to its level at the start of a recession is just 0.3%.

Quits high, unemployment low (for now)

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics (BLS), as of 10/31/2022.

The long road ahead for labor

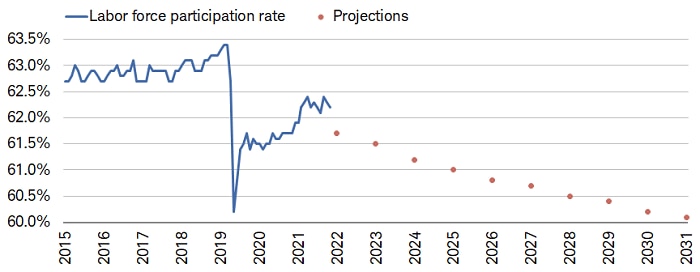

One of the main hopes and goals of the Fed has been to see an increase in labor force participation as the economy continues to both emerge from the pandemic and adapt to its long-term effects. To be sure, the increase from the COVID low has been impressive and welcome, but most of that was simply because many workers rejoined the workforce as it became safer to do so.

It is becoming increasingly clear, though, that labor force participation is bumping up against a demographics ceiling. As shown below, projections from the Bureau of Labor Statistics (BLS) show the labor force participation rate falling to nearly 60% by the early 2030s—not only would that be a marked downshift from current levels, it would bring it to below the trough during the depths of the pandemic.

Labor force participation with less participants

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics (BLS), as of 10/31/2022.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The latest Household Pulse Survey from the U.S. Census Bureau estimates that around 12 million Americans are not in the labor force for reasons pertaining to COVID (nearly a quarter of that can be traced to long COVID). With very little historical data on labor effects from a global pandemic (not to mention that the last one was nearly a century ago), it's nearly impossible to gauge how many of those workers can or will come back into the workforce.

At least in the near term, the likelihood for reentry is low. If remote work is desired—given little or no ability to interact face-to-face with customers—one likely has to look to the goods sector over services. Yet, goods-oriented companies are facing the strongest headwinds today, including weaker goods demand, still-high inventories, and bloated payrolls. Goods inflation has fallen swiftly this year, which doesn't bode well for forward profit margins or labor within the sector. As such, workers with long COVID may find themselves increasingly shut out from employment opportunities, putting downward pressure on overall labor force growth.

Add to that a weakening demographic profile in the United States (and many areas around the globe), and the outlook is one of increasingly scarce labor. Thus, what has been a secular landscape dominated by capital—aided by the ample liquidity environment since the Global Financial Crisis—could be morphing into a secular landscape of rising labor dominance. Other likely secular shifts underway are: from globalization to regionalization (distinct from deglobalization); demand shocks giving way to increasing supply shocks (especially re: energy/commodities); and relative peace to more geopolitical volatility.

Stocks re: coming pause

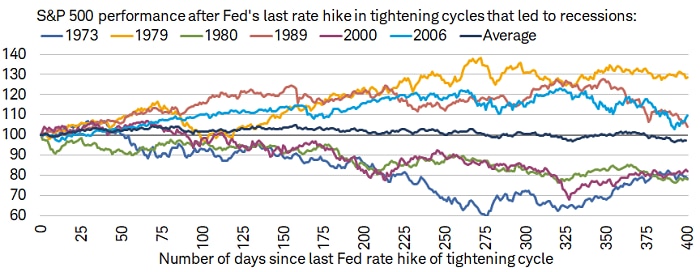

In terms of near-term Fed policy, looking at history, there is wide variability in terms of stock market performance following the final rate hike in a cycle, shown below. As such, be careful extrapolating the average experience (as has been said, analysis of averages leads to average analysis). Highlighting the fits-and-starts nature of the late-1970s/early-1980s cycle, the best market performance came after the final rate hike in 1979; but of course, that was followed by a brutal double-dip recession and the worst market performance following the final rate hike in 1980.

In general, the year in which stocks did well after the final hike were marked by a strong labor market, while poorer performance was associated with a subsequent contraction in payrolls. As such, the labor market is likely key to market performance once the Fed pauses. All else being equal, we expect volatility and bouts of weakness to persist heading into 2023 alongside a weakening in the labor market, but a sunnier environment as the pages of the calendar turn toward the second half.

After final rate hike

Source: Charles Schwab, Bloomberg.

Data indexed to 100. An index number is a figure reflecting price or quantity compared with a base value. The base value always has an index number of 100. The index number is then expressed as 100 times the ratio to the base value. Past performance is no guarantee of future results.

Our expectation of more near-term volatility to come is supported by likely worsening trends in corporate earnings and the labor market. It may seem counterintuitive, but weakness in both areas would be welcome sooner rather than later, as it would bring the Fed closer to checking the box of increasing slack in the labor market—ultimately helping put downward pressure on inflation. If that occurred alongside a stabilization and/or turn higher in leading indicators, that would set up the economy for better days later in the year.

On earnings and valuation

Excluding the Energy sector, S&P 500 earnings growth is expected to be negative in 2022's fourth quarter, which would be the third consecutive quarter with negative year-over-year earnings. We think there is further downside in 2023, not least because high inflation has supported nominal revenue growth (along with hiring), while lower inflation would put cracks in those supports. Sales growth has been significantly stronger than earnings growth, suggesting profit-margin pressure is building heading into 2023. Expect that to be a bigger story in 2023.

The current consensus estimate for 2023 S&P 500 earnings is for growth of nearly 5%. Although that has been trimmed from nearly 10% last spring, we think there is ample risk of lower estimates—especially for the first half of 2023. In the lead-in to recessions, analysts tend to be slow to reduce forward estimates; we are expecting increasing downgrades, especially once fourth quarter 2022 earnings season gets underway in January 2023.

We expect at least a quarter or two of negative year-over-year earnings, even including the Energy sector, before a stabilization is possible. But we also expect the hit to earnings to be rolling in nature at the sector level—in keeping with the rolling recession ongoing in the economy.

Stocks re: earnings/inflation

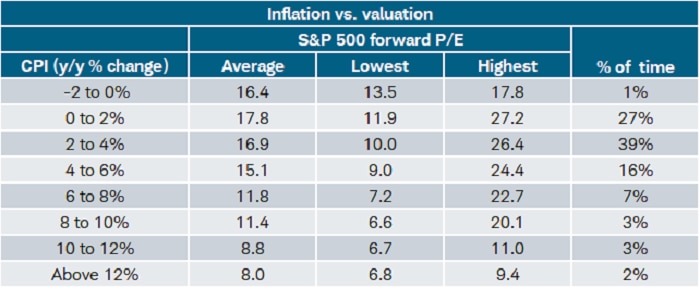

Stocks have historically tended to bottom before earnings troughs—even though they tend to struggle during the estimate decline phase—especially if unemployment claims are rising, which we expect in early 2023. Keep an eye on PMIs and housing (as well as the U.S. dollar), as stabilization there would likely mean stabilization in forward earnings estimates. Declining estimates should continue to put upward pressure on P/E ratios, in stark contrast to 2022, when P/Es were under downward pressure from inflation. As shown below, as inflation recedes further in 2023, it would alleviate some of the downward pressure on multiples.

Inflation's impact on valuation

Source: Charles Schwab, Bloomberg, Standard & Poor's. 1958-10/31/2022. Numbers may not add up to 100% due to rounding.

Here is an interesting analysis to ponder as you consider the trajectory of inflation and how the stock market might perform. SentimenTrader went back to 1914, using the Dow Jones Industrial Average (which has a longer history than the S&P 500), and did a growth-of-a-dollar comparison based on the range of inflation. They divided the CPI into three zones: two "bad" zones of inflation above 4% or deflation of lower than -3%, and one "moderate" zone of the CPI between -3% and +4%.

Even though past performance is no guarantee of future results, the cumulative growth of $1 invested in the Dow if the previous month ended with the CPI in the moderate zone has been more than 150,000%. On the other hand, the cumulative growth of $1 invested in the Dow if the previous month ended with the CPI in either of the bad zones has been -63% (with most of the damage occurring during the severe deflation in the 1930s). Fun stuff.

Getting clearer

Something important came into clearer focus in 2022, which should continue to be a force in play in 2023: the return of the risk-free rate and perhaps the demise of the era of malinvestment and speculative excess. Fundamentals are reconnecting to prices, with important implications for investors.

As was the case in 2022, we continue to recommend more of a factor-based investment process than a sector- or style-index-based process. At least until the economy begins to stabilize, we are recommending that stock-picking-oriented investors focus on quality-based factors, including balance sheet liquidity, positive earnings revisions/surprises, strong free cash flow, dividend growers and lower volatility. There may be a time in 2023 to move down the "quality spectrum" to take advantage of an upturn in growth, but that would likely be later in the year. In the meantime, as the market continues to try to time a shift in policy by the Fed, factor volatility could remain elevated.

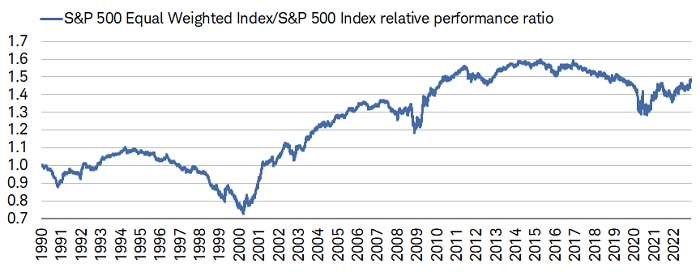

We also think the outperformance of equal weight relative to capitalization weight, shown below via the S&P 500, should persist at least in 2023's first half. It's even possible that we are setting up for a longer span, akin to what occurred in the aftermath of the bursting of the dotcom bubble in 2000.

Equal punching above its weight

Source: Charles Schwab, Bloomberg, as of 11/25/2022.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance does not guarantee future results.

Speculation wrung out?

The liquidity tide has clearly gone out, and as Warren Buffett once said, it's when you find the "naked swimmers." Sam Bankman-Fried's FTX has become one of this cycle's naked swimmers; but the contagion, for now, has been contained. Although we expect more ripple effects, they are likely to be contained to ripples, not massive waves, given the limited exposure by the traditional banking system. That said, the fallout could make access to capital increasingly more challenging in 2023, especially for the capital-constrained.

That said, watching the FTX debacle brings back the memory of Charles Kindleberger's famous book, Manias, Panics, and Crashes: A History of Financial Crises, which had this memorable line: "The propensity to swindle grows parallel with the propensity to speculate during a boom; the implosion of an asset price bubble always leads to the discovery of frauds and swindles." The so-called "crypto winter" coupled with the bear market in stocks in 2022 did a lot to dent investor confidence.

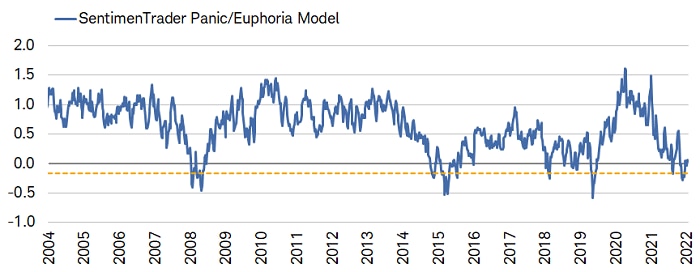

From euphoria to panic

The move up from extreme panic seen in SentimenTrader's Panic/Euphoria Model bodes well for stocks, assuming a time horizon stretched beyond the near-term. As shown below, since 2004, stocks were up 100% of the time following a move up from an extreme low (see table for details). The reversal is consistent with what recently occurred in the equity put/call ratio and other sentiment indicators, most of which point to ongoing volatility near-term, but a better outlook assuming a one-year (or so) horizon.

Less panic, but no euphoria

Source: Charles Schwab, SentimenTrader, as of 11/25/2022.

This model is based on the Citi Panic / Euphoria model that is published in Barron's magazine. It does not reflect those published values, rather it is our interpretation of the model inputs and construction, and differs modestly from the published figures. The inputs are the same, however its performance as a contrary indicator is improved over the published values. It is composed of the following primary inputs: NYSE short interest, margin debt, Nasdaq vs NYSE volume, Investor's Intelligence survey, AAII survey, retail money market funds, put/call ratios, commodities prices, and retail gasoline prices. The higher the model, the more investors are in a euphoric mood, with lower expected stock returns going forward. Low values, particularly below zero, suggest that investors have panicked and higher forward returns are expected. Yellow dotted line represents -0.17 threshold. Past performance is no guarantee of future results.

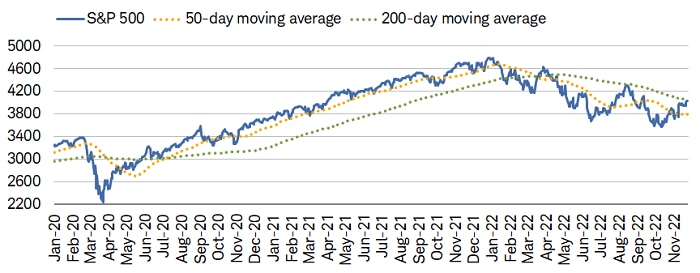

Keep an eye on…

As Thanksgiving tryptophan was kicking in, the S&P 500 was staging its third meaningful run at its 200-day moving average, shown below. Unfortunately, it failed at that average last August, but the outlook for a positive breach is improving. In particular, as shown in the table below, based on the full history of the S&P 500, the annualized gain for the S&P 500 was significantly higher when the 50-day moving average moved above the 200-day moving average. There is a ways to go before that can occur in the current cycle, but a positive breach would be a positive sign for the market.

Moving averages moving

Source: Charles Schwab, Bloomberg, ©Copyright 2022 Ned Davis Research, Inc.

Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/, as of 11/25/2022. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

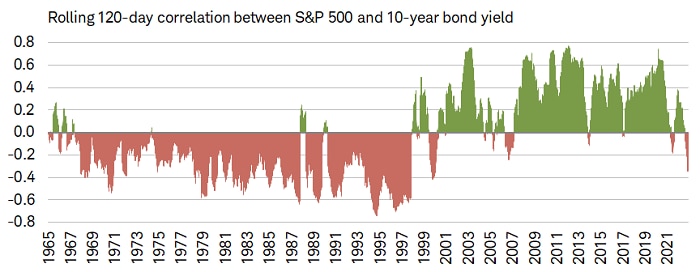

Finally, keep an eye on the relationship between bond yields and stock prices. As shown below, for about three decades between the late-1960s and late-1990s, there was nearly always an inverse relationship. That era was defined by an "inflationary backdrop" such that when bond yields were rising, it was typically because of rising inflation risk—negative, in general, for stocks. Conversely, in the subsequent two decades starting around 2000, the correlation was mostly positive. It was an era defined by the "great moderation" (in inflation/rates), such that when bond yields were rising, it was typically because of improving growth, not a budding inflation problem—positive, in general, for stocks.

Secular yields/stocks correlation

Source: Charles Schwab, Bloomberg, as of 11/25/2022.

Correlation is a statistical measure of how two investments have historically moved in relation to each other, and ranges from -1 to +1. A correlation of 1 indicates a perfect positive correlation, while a correlation of -1 indicates a perfect negative correlation. A correlation of zero means the assets are not correlated. Past performance is no guarantee of future results.

As shown above, a sustainable negative correlation could suggest that we're in a more inflationary secular era (even if inflation continues to move down cyclically). But it would also mean that as inflation recedes, the backdrop for stocks improves.

In sum: worse before better

Key to the outlook for the early part of 2023 is the Fed's stated goal of bringing down aggregate demand to meet supply with restrictive policy (for longer) that will slow the economy and bring inflation down sustainably. Key to when the Fed's job is seen as largely done will likely be stabilization in areas like housing, purchasing managers indexes (PMIs) and consumer/CEO confidence. The Fed has telegraphed an eventual step-down and pause in rate hikes, which is likely within 2023's first half. But they're also telegraphing the likelihood of the fed funds rate remaining at the "terminal rate" for an extended period. In other words, there may be more bumps in the road near-term given inflation is still noticeable (albeit in the rearview mirror), but the longer-term outlook via the windshield has improved.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All