Total Concentration: Mega Caps Reign

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe concentration of gains up the cap spectrum isn't itself a precursor to weakness; it's the lack of participation from the "average stock" that warrants some caution.

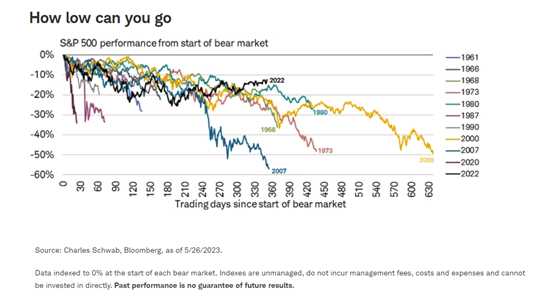

An ever-popular question these days is whether the October 12th, 2022, low for the S&P 500 was "the" low—and thus, if the bear market is over. The short answer is no one knows, and that may be the case for some time.

To add more color to the debate, the chart below shows the maximum percentage declines for all S&P 500 bear markets since the 1960s. If the bear market did indeed end back in October, it would have lasted for 195 trading days, which is about average when considering the entire sample size. If the bear market is still ongoing (meaning, the October low is to be broken through), this bear is getting longer in the tooth, now being more than a year old.

That length isn't unprecedented, however. Sticking with the possibility that the bear market isn't yet over puts it in the company of bears that started in 2007 and 1968 (and beyond that, 1973, 1980, and 2000). The worst-case scenario would be something akin to the bear that started in 2000, which was clearly the most frustrating drawdown (in terms of timing, not magnitude) in the collection below.

"The market" vs. the market

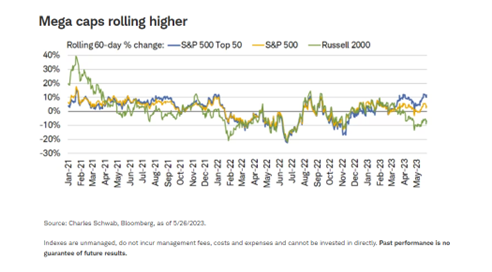

One of the discomforting (and widely advertised) aspects of the market's advance this year has been the concentration of gains up the cap spectrum. Leadership among the mega-cap names—and the sectors in which they are housed (Information Technology, Consumer Discretionary, and Communication Services)—has strengthened while the "average stock" hasn't moved much at all.

As shown below, there is quite a wide performance gap between the 50 largest names in the S&P 500, the overall S&P 500, and the Russell 2000. Looking at the two extremes, over the past 60 trading days, the 50 largest names are up by 11.7%, while the Russell 2000 is down by 6.7%. It's an important distinction to make, especially given the excitement over the so-called resilient nature of "the market" this year. If "the market" is a handful of mega-cap names, then performance looks great; if it's the rest of the crew, the story looks different.

The underperformance down the cap spectrum is worrisome for a couple of reasons. First, back in 2021, small caps and the "average stock" were under a lot more pressure than the headline indexes showed. A series of rolling corrections and bear markets under the surface ultimately preceded what turned out to be a full-blown bear in 2022. Second, with the economy now fully reopened, the absence of any strong performance from key cyclical segments of the market (i.e., small caps) would be worrisome.

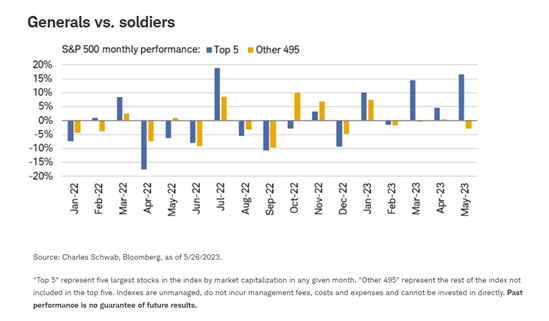

Shown below, narrowing the scope further, the five largest names in the S&P 500 have decisively outperformed their peers (the other 495) this year (most notably in March and May). We're not of the thought that the mega-cap outperformance in and of itself is a precursor to imminent market doom, but at some point, the lack of participation from the rest of the market should be noted as a likely sign of coming deterioration.

A weak start

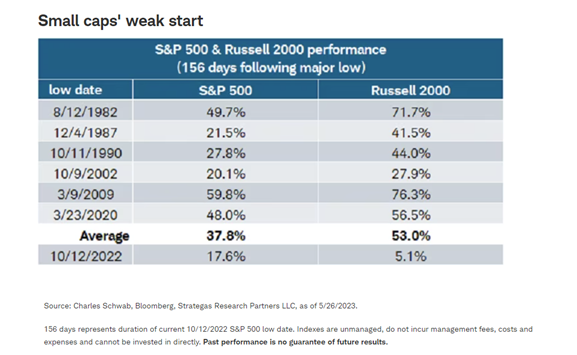

As mentioned at the beginning of this report, if one were to assume we're still in a bear market, it's getting long in the tooth. Embracing the opposite assumption—that we're in a new bull market—means the October low is not to be revisited, given we'd be in a new bull cycle. If that's the case, this would be one of (if not the) most underwhelming starts to a new bull market in history.

One way of seeing that is via the performance of small caps (proxied by Russell 2000). As shown in the table below, going back to the inception of the Russell 2000, small caps have always tended to do well when the market was this far beyond a major market low (decline of 20% or more), given they're closely tied to the economy. The current gain since October clearly stands out in a not-so-good way.

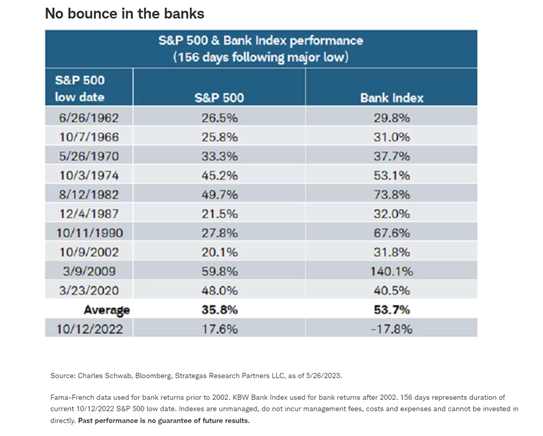

The same goes for another key, cyclical part of the market—the banks. As shown in the table below, going back to the 1960s, banks have always tended to have strong performance gains after a major market low, regardless of whether they outperformed the S&P 500. Through Friday's close, the KBW Bank Index is down by 17.8%.

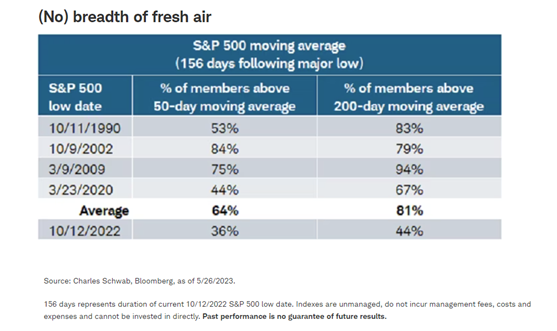

Rounding out our table analysis and shown below, the market's breadth looks quite weak today in comparison to prior bull market beginnings. Breadth data is quite limited, so we can only look at the four major bear markets that preceded the one in 2022, but nonetheless, it's in much weaker territory this time around. Through Friday's close, the share of S&P 500 members trading above their 50- and 200-day moving averages was 36% and 44%, respectively. That compares to respective averages of 64% and 81% for the 156 days after the conclusions of the prior four bear markets.

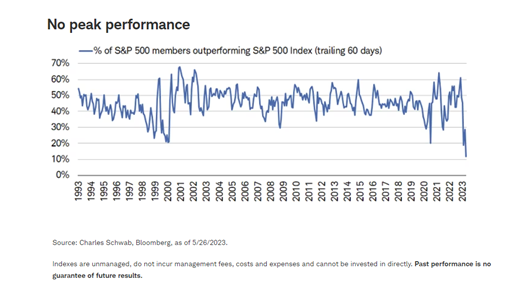

Finally, another sign of the market's weak breadth is that only 12% of S&P 500 stocks are outperforming the overall index on a 60-day trailing basis. As shown below, that's an all-time low going back to 1993 (and notably, lower than it was in March 2000 at the peak of the tech bubble). The seven largest stocks in the S&P 500 are all up over the last three months with an average gain of 29.3%, while the seven smallest stocks are all lower and down by an average of 33.3%.

In sum

Market performance has become top-heavy again, with investors biased toward the largest technology and tech-related stocks. Only 36% of the S&P 500 stocks are trading above their 50-day moving averages, and only 44% are trading above their 200-day moving averages. As Michael Caine once said about a duck: calm on the surface but paddling like the dickens underneath.

The concentration on the mega caps kicked into high gear at the beginning of the current banking crisis in early March, with the added kicker of enthusiasm around artificial intelligence (AI). Our advice is to be wary of concentration risk in your own portfolios and use periodic rebalancing to keep individual positions and market segments from ballooning in relative size. Mean reversion is inevitable at some point, although trying to pinpoint the timing can be an exercise in futility.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve.

Investing involves risk including loss of principal.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Small-cap funds are subject to greater volatility than those in other asset categories.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Diversification and rebalancing of a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when a non-retirement account is rebalanced, taxable events may be created that may affect your tax liability.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

Fama-French data was developed by Kenneth Ronald French, a professor of finance at Dartmouth College, and Eugene Francis Fama, a professor of finance at the University of Chicago. They are best known for their joint work in asset pricing and together, they created the Fama-French three-factor model (http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html).

KBW Bank Index is a modified cap-weighted index consisting of 24 exchange-listed National Market System stocks, representing national money center banks and leading regional institutions.

A message from Advisor Perspectives and VettaFi: To learn more about this or other topics, please check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All