With peak inflation firmly in the rearview mirror, the attention of the Federal Reserve and market watchers has shifted to some degree toward the labor market side of the Fed's dual mandate. Detailed below, June's Bureau of Labor Statistics (BLS) jobs report likely did little to sway the Fed away from another 0.25% rate hike at the July Federal Open Market Committee (FOMC) meeting; even if there was some welcome relief that the BLS report did not corroborate the very hot (+497k) Automatic Data Processing (ADP) jobs report earlier last week. In the aftermath of the release of Friday's BLS report, the probability of a July rate hike had jumped to nearly 95% per the Chicago Mercantile Exchange (CME's) Fed Watch Tool (uses 30-day fed funds futures pricing data).

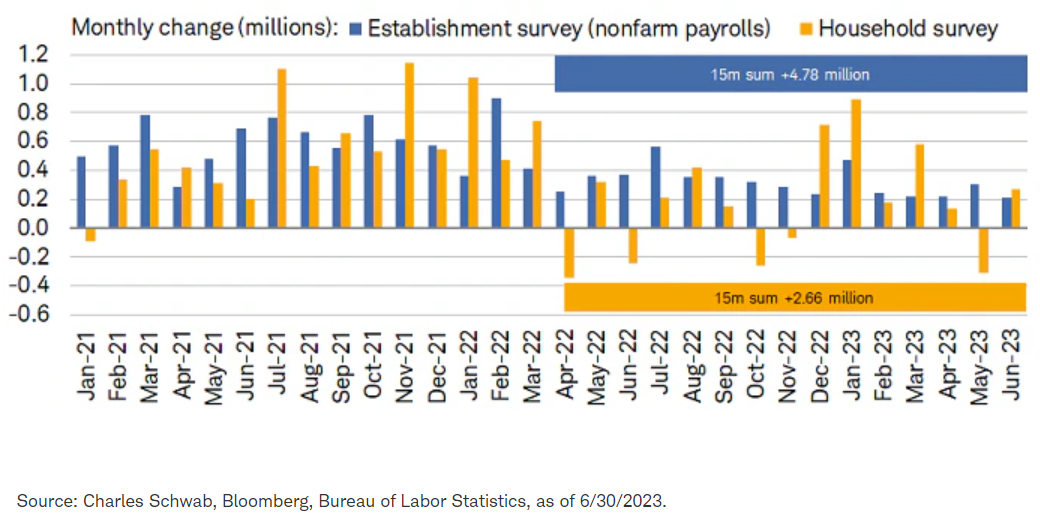

Establishment vs. household surveys

The BLS's establishment survey (which counts jobs) of nonfarm payrolls for June came in at 209k, which was the first below-consensus report in more than a year. In addition, there was 110k' worth of downward revisions for the prior two months, taking the three-month average down to 247k from 283k reported in May. The BLS's household survey (which counts people), from which the unemployment rate is calculated, showed employment increasing by 273k after declining by 310k in May. The household survey tends to lead the establishment survey in advance of recessions, so its stall below the April high is noteworthy. The comparison between the two is shown below. As shown via the summary bars below, over the past 15 months, household employment has contracted in five of those months, with the overall gain more than two million below the gain associated with the establishment survey of payrolls.

The survey says

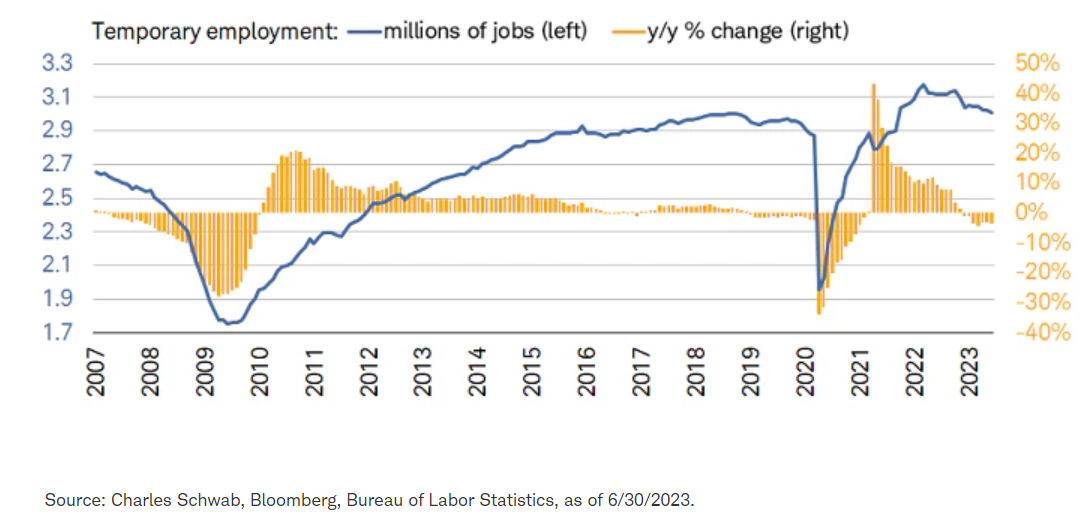

Private sector (excluding government) job growth slowed to 149k, which was the smallest gain since November 2020. Temporary employment was weak—down 13k in June, which is -3.4% year-over-year. Like the household survey measure of employment, temporary employment has historically lead payroll employment in advance of recessions, as shown below.

Temporary contraction?

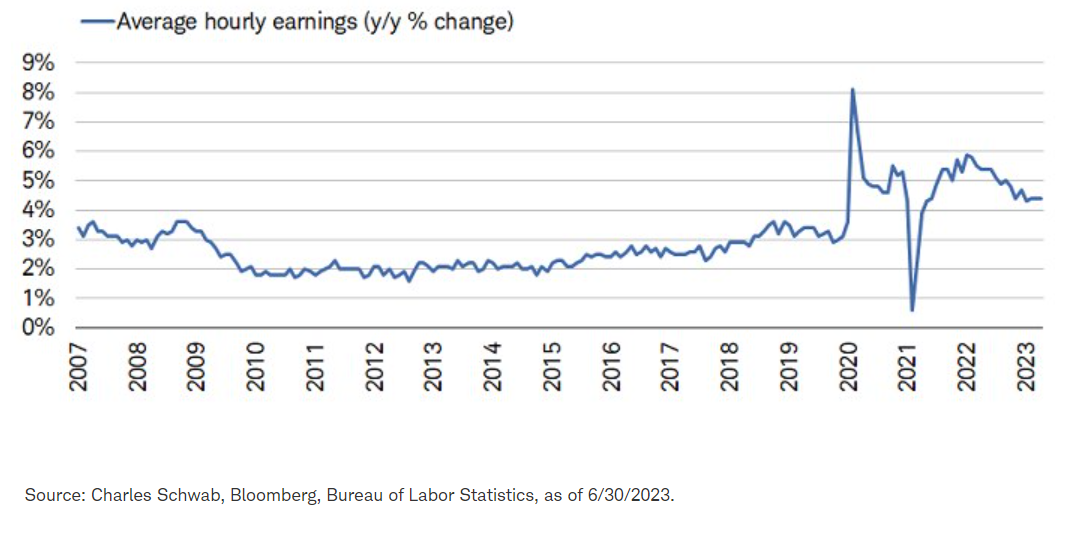

Sticky wage growth

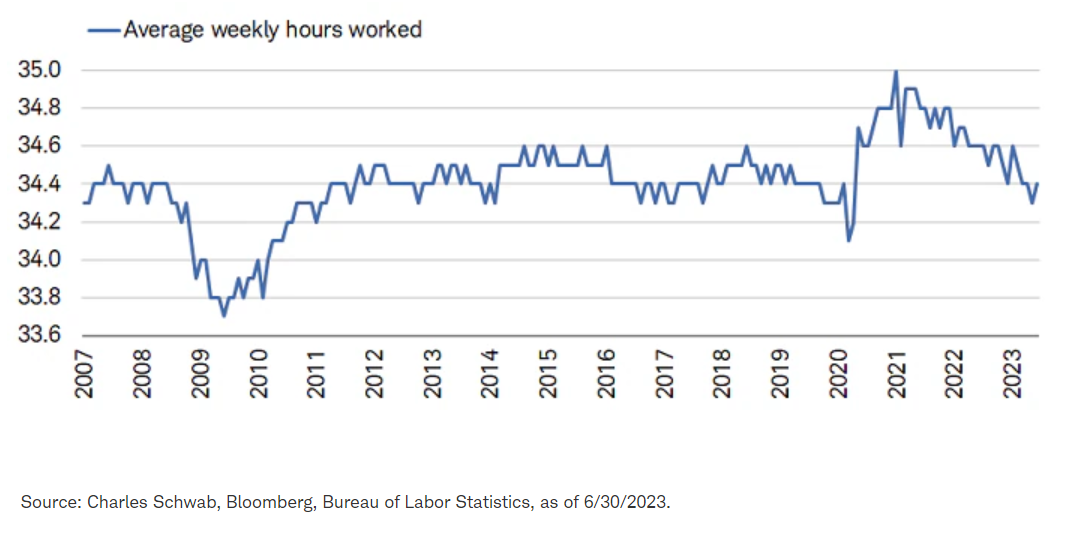

The culprit behind the lift in July's rate hike probability was probably slightly hotter-than-expected wage growth. Average hourly earnings increased 0.4% month-over-month and 4.4% year-over-year, the latter of which is shown in the first chart below. Alongside still-sticky wage growth was an uptick in hours worked in June, shown in the second chart below. The thorn in the side of the Fed is the combination of solid wage growth and an unemployment rate only slightly above its all-time low. The blunt instrument of monetary policy can only tackle the demand side of inflation; and with labor demand up more than the increase in the labor force, it suggests the Fed's job is not done.

Sticky high wage growth

Working a little more?

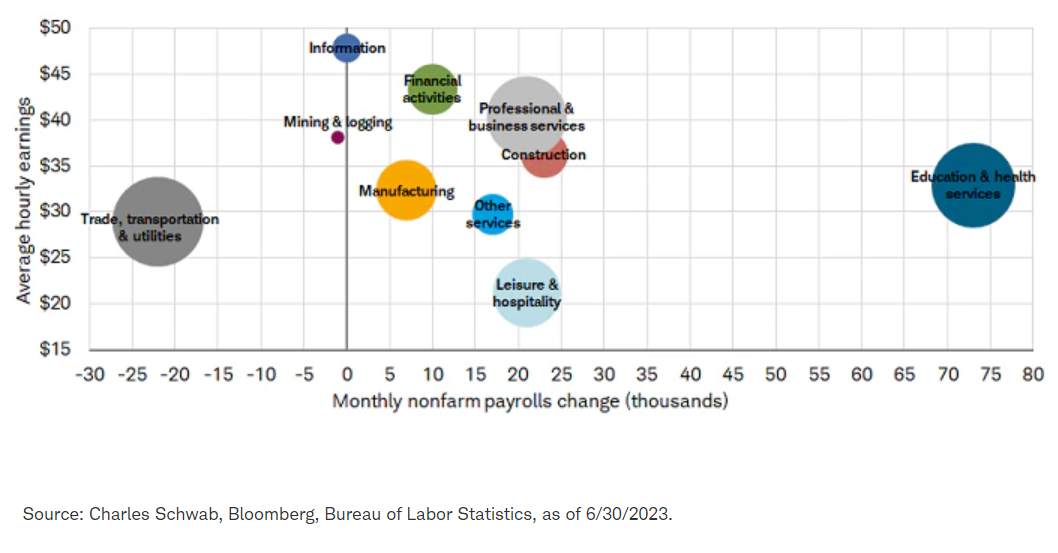

Payrolls' deteriorating breadth

The chart below looks at payrolls by sector, with the horizontal axis showing the one-month change and the vertical axis showing average hourly earnings. The diameter of each circle is tied to each sector's weight within the economy in terms of overall payrolls. As shown, the largest payroll gains—specifically within education and health services—were in the middle-wage region. Related to recessions historically, payrolls' breadth tends to narrow in advance, which is now occurring. The employment diffusion index has been in a gradual descent and hit 58% in June. That is down from 61.2% in May and well below the cycle high of 85% in early-2022. Of note is that payroll growth is noticeably slower in the pandemic-benefitted sectors, with those sectors hurt most by the shutdown phase of the pandemic still adding headcount.

Educated and healthy

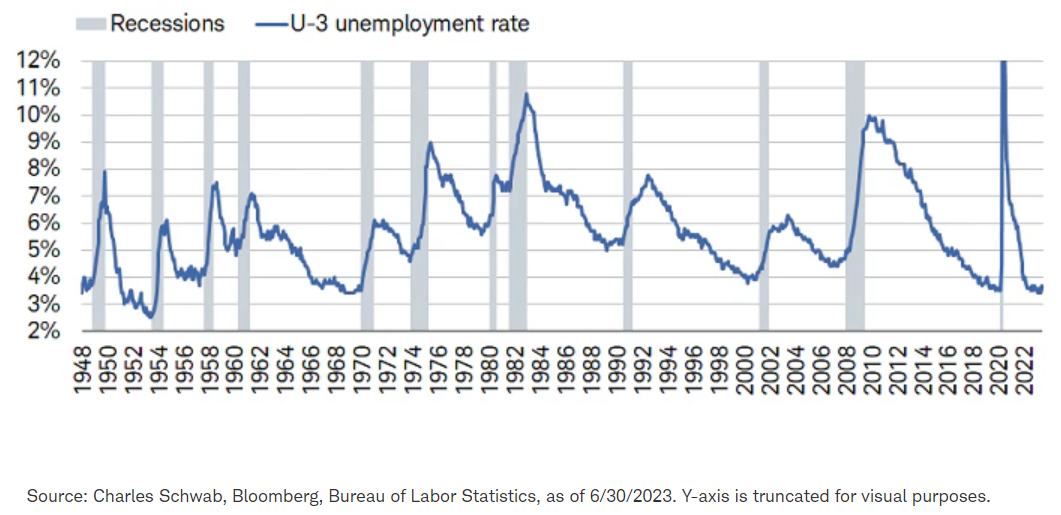

Stubbornly low unemployment rate

The headline unemployment rate, shown below, ticked lower by 0.1% to 3.6% via the number of unemployed falling by 140k and the labor force increasing by 133k. As shown in the chart, as a lagging indicator, the headline (U-3) unemployment rate has historically always been near its cycle low when the economy entered a recession. It highlights the fact that—against conventional wisdom—a rising unemployment rate doesn't bring on a recession…recessions bring on a rise in the unemployment rate. On the other hand, the U-6 unemployment rate, which includes people working "part-time for economic reasons" rose 0.2% to 6.9%, which is the highest in nearly a year.

Low but lagging

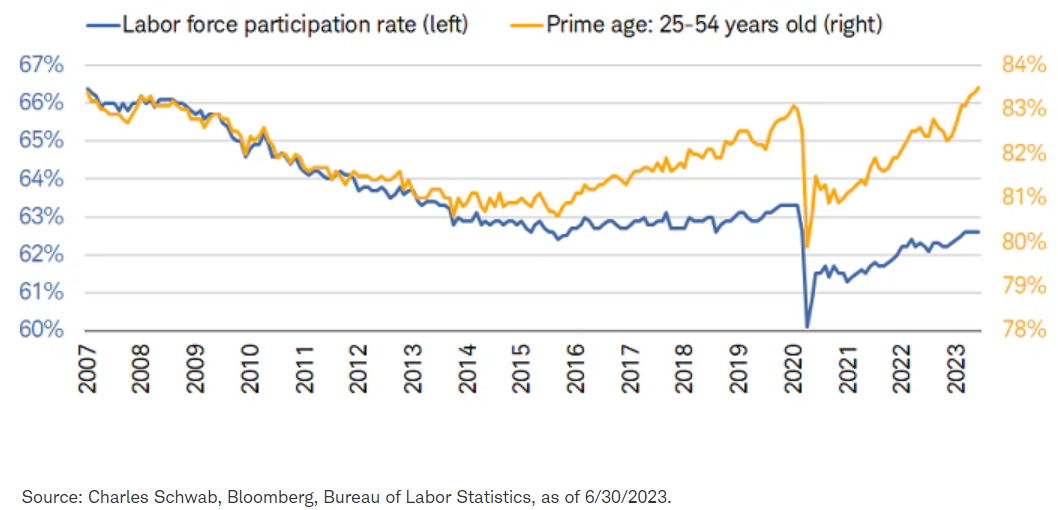

As touched on above, and as shown in the chart below, the overall labor force participation rate (LFPR) was flat at 62.6%, but the prime-age LFPR hit a new cycle high of 83.5%, which was the highest in more than 20 years. We believe the labor force has further room to grow given a positive long-term outlook for capital spending—in particular, associated with trends around onshoring and/or supply chain diversification.

In their prime

In the lead

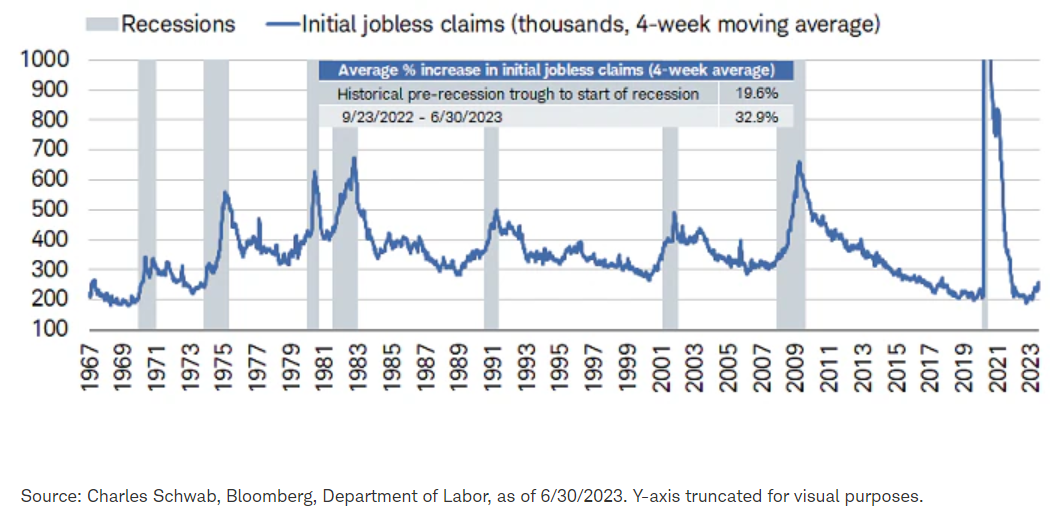

The aforementioned lagging nature of the unemployment rate means a focus on leading labor market indicators remains key. One of those is initial unemployment claims—one of the 10 components of the Leading Economic Index from The Conference Board. Shown in the summary table within the chart of the four-week moving average of claims, the nearly 33% lift off this cycle's deep trough is already well above the 20% average increase associated with past recessions; although below the high end of the 4% to 40% range associated with that historical average. In addition, there are now 46 states with rising continuing (ongoing) unemployment claims, which is a level that has historically occurred only in recessions.

Claims' ascent

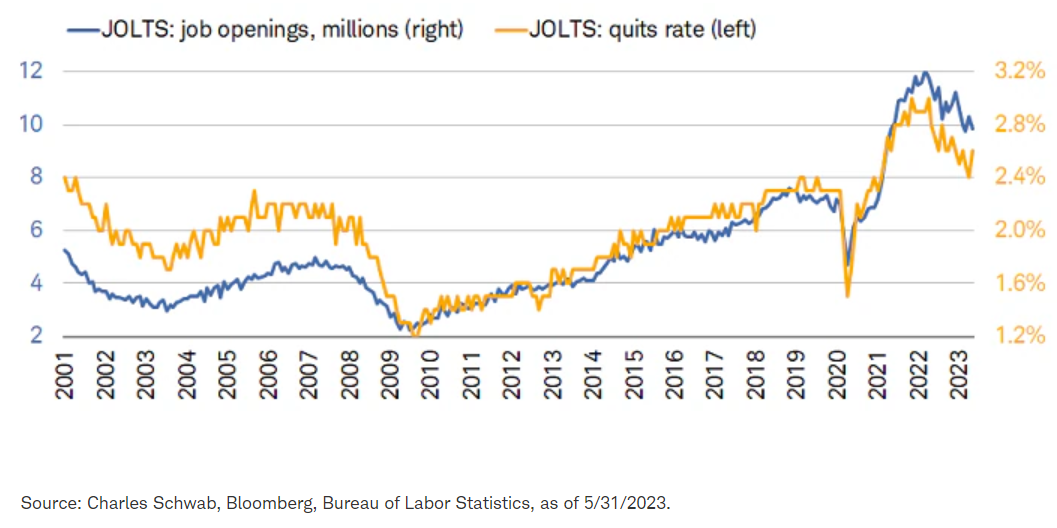

There are also labor market indicators that lead the leading indicator that is unemployment claims. Via the Job Openings and Labor Turnover Survey (JOLTS), job openings have been generally trending down, but remain historically high, shown in the blue line below. The Fed has expressly noted the need to see this continue to move lower. Unfortunately for the Fed, the associated "quits rate" (the percentage of workers voluntarily quitting their jobs) ticked higher in May, shown in the orange line below. The JOLTS data lags the jobs report data by one month.

Quits up, but openings down

In sum

Although the June jobs report offered solace to both economic bulls and bears, it likely didn't sway the Fed from its bias to hike rates at least one more time. The signaling—from the Fed and economic/inflation data to come—between the July and September FOMC meetings is yet to come. Fed- and market-watchers should maintain a keen focus on both sides of the Fed's dual mandate—inflation and employment—as the relationship between the two will drive monetary policy expectations over the remainder of this year. We continue to anticipate a generally disinflationary trend (with possible volatility). However, the Fed may have more work to do to convince markets that their pledge to stay "higher for longer" (particularly the "for longer" part) is firm.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Investing involves risk including loss of principal.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

Employment diffusion index measures the percent of industries with employment increasing plus one-half of the industries with unchanged employment, where 50 percent indicates an equal balance between industries with increasing and decreasing employment.

The Charles Schwab Corporation provides a full range of brokerage, banking and financial advisory services through its operating subsidiaries. Its broker-dealer subsidiary, Charles Schwab & Co., Inc. (Member SIPC), offers investment services and products, including Schwab brokerage accounts. Its banking subsidiary, Charles Schwab Bank, SSB (member FDIC and an Equal Housing Lender), provides deposit and lending services and products. Access to Electronic Services may be limited or unavailable during periods of peak demand, market volatility, systems upgrade, maintenance, or for other reasons.

This site is designed for U.S. residents. Non-U.S. residents are subject to country-specific restrictions. Learn more about our services for non-U.S. residents

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Charles Schwab

Read more commentaries by Charles Schwab