Mixed Signals: December's Jobs Report

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhile headline payroll growth was relatively strong in December, weaker details under the surface continue to paint a mixed labor market picture.

The headline was shiny, but the details were duller. The Bureau of Labor Statistics (BLS) jobs report for December, released on Friday, had something in it for both the economic bulls and bears. Nonfarm payrolls were up 216K in December, which was well north of the 170K economists' consensus estimate. There was some weather-related flattering, with 87K folks "not at work due to weather" vs. a recent December average of 101K (2019-2022).

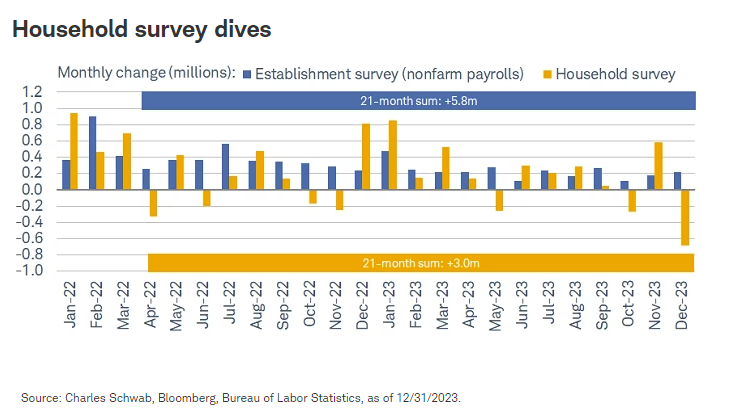

One immediate rub associated with the report was the 71K of downward revisions to the prior two months' readings. Another rub was overly optimistic "birth/death" (of businesses) assumptions, which added about 110K to the December payrolls release. A final rub was the massive 683K decline in household employment. As a reminder, the BLS conducts two surveys each month: the "establishment survey" from which the payrolls data comes, and the "household survey" from which the unemployment rate is calculated.

As shown below, there have been quite a few months since the spring of 2022 when the difference between the two surveys was quite dramatic. In fact, since April of 2022, the establishment survey tells a story of 5.8 million jobs having been created vs. the household survey's 3.0 million. For what it's worth, around important inflection points in the economy, the household survey tends to send the more accurate message about the health of the labor market.

In addition, multiple jobholders jumped to 8.57 million, which is up to 5.3% as a share of those employed; those readings are up from about 7.5 million (in early 2023) and about 4.8% (in mid-2023), respectively. In the household survey, the number of full-time workers fell by the most since April 2020; the only gains were in part-time employment (which were of course offset by the decline in full-time workers).

Resilience in non-cyclical sectors

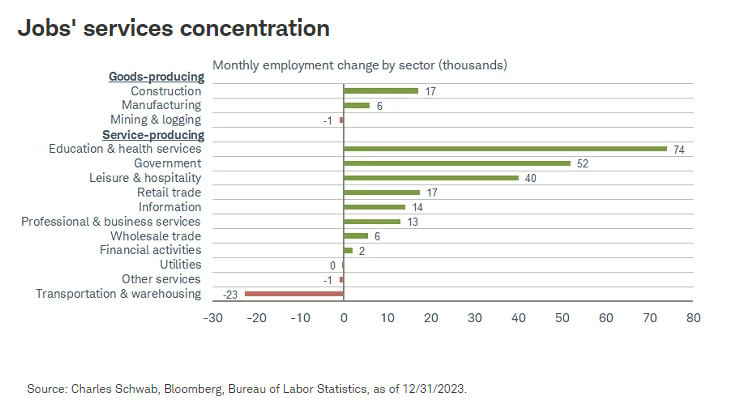

In terms of economic sector strength and weakness, as shown below, the largest job gains were among the education/health services ("eds and meds"), government, and leisure/hospitality sectors—all of which reside in the services side of the economy. There were more tepid gains—and even a small loss of jobs in mining/logging—within the goods side of the economy. This continues to reinforce our nuanced description of the unique pandemic-infected cycle: that of "rolling recessions/recoveries" vs. a traditional "all at once" type of recession/recovery cycle.

Not shown in the chart is the temporary help services sector, which is typically seen as a leading indicator for overall payrolls and has been cutting jobs for 11 consecutive months. In fact, the current magnitude of decline in temporary help services payrolls has never been seen outside of a recession.

Revisionist history

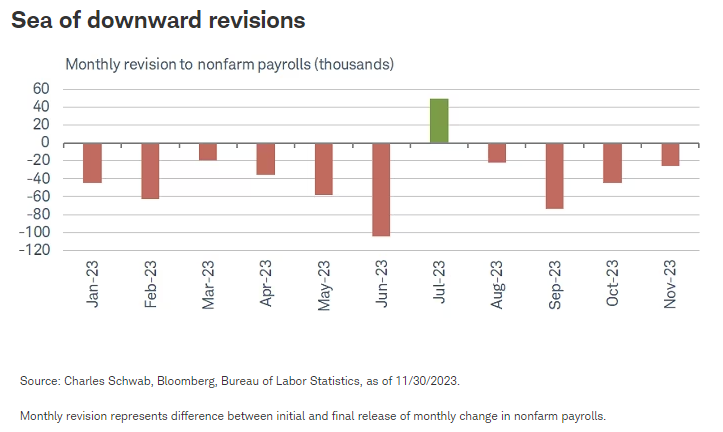

Specific to the downward revisions to the monthly change in nonfarm payrolls, through November of 2023, all but one month experienced downward revisions, as shown below.

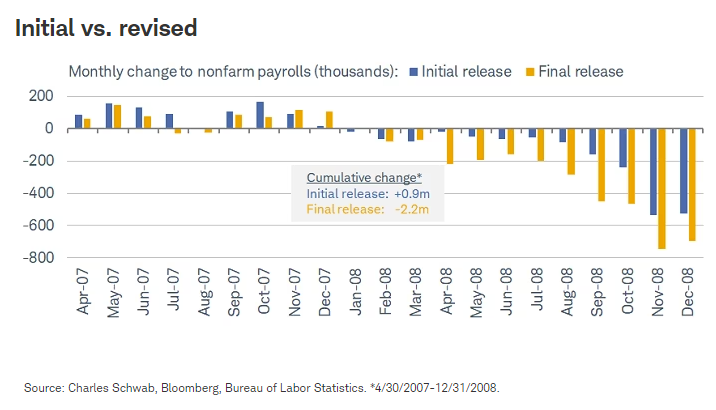

This brings up an important message about comparing current headline labor market data to historical information—particularly when assessing recession risk. If you were to pull up a long-term chart of payrolls, the data would reflect all of the revisions that came subsequent to initial releases. It's part of the reason why you should be skeptical about proclamations like, "there is no way a recession is possible with still-strong payrolls growth." Below is a case in point, covering the period leading into the global financial crisis (GFC).

The blue bars above represent the initial release of the establishment survey of payrolls, while the orange bars represent the actual readings once all subsequent revisions were in place. (As a reminder, the BLS does revisions for the prior two months each time they release the monthly jobs report; but in addition, they do annual "benchmark" revisions on top of the monthly revisions. The next benchmark revision will be in February.)

Prior to the start of the GFC-related recession in December 2007, seven out of the eight prior months' initial readings were ultimately revised lower. In other words, the perceived story at the time was of fairly healthy job growth, while the actual story was of a deceleration into recession territory. The initial story was an economy that had added one million jobs between April 2007 and December 2008, while the real (post-revisions) story was an economy that had shed more than two million jobs over that period. As you can also see, once the recession was underway, the revisions really kicked in on the downside.

Unemployment vs. underemployment

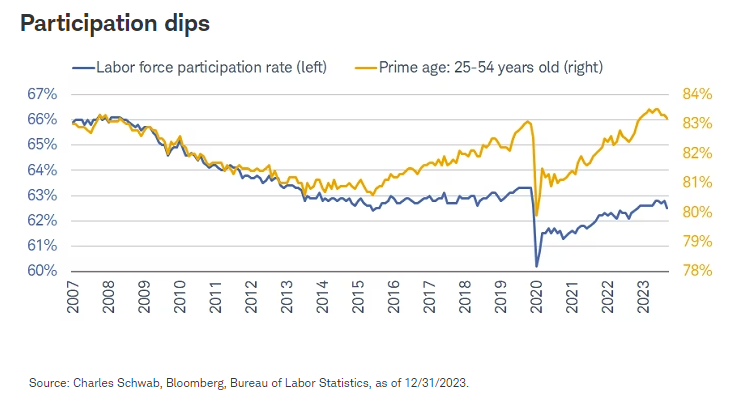

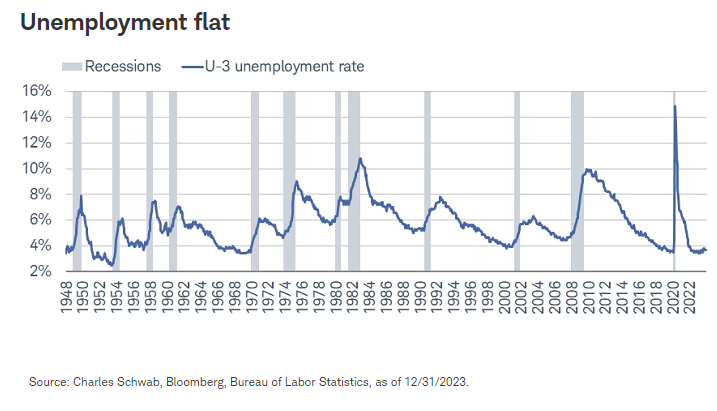

As mentioned, the household survey—which is a survey of people, not of companies—is used to calculate the unemployment rate, along with the labor force participation rate (LFPR). Courtesy of a meaningful decline in the LFPR, including a decline for prime age folks (both shown in the first chart below), the unemployment rate held steady at 3.7% (shown in the second chart below). The math behind no change in the unemployment rate is that the 676K decline in the size of the labor force was nearly as large as the 683K decline in household employment.

Unfortunately, the longer-term unemployment rate (percent unemployed for at least 27 weeks) ticked up to 19.7%, which is up from 17.5% in February 2023. In addition, the "underemployment rate" (the percent of employed people working part-time but would prefer full-time) rose to 7.1%, which is up from 6.6% in April 2023.

Here's another important reminder about the unemployment rate: It is one of the most lagging of all economic indicators, so heed the warning about focusing on it when assessing where the economy is in a cycle. As we often explain, a rising/high unemployment rate doesn't bring on recessions…recessions eventually cause the unemployment rate to rise. You can clearly see that above around the gray-shaded recession bars. It also works on the "back end" of a cycle: A falling unemployment rate doesn't bring on recoveries…recoveries eventually allow the unemployment rate to fall.

Stronger wage growth not supportive of rate cuts

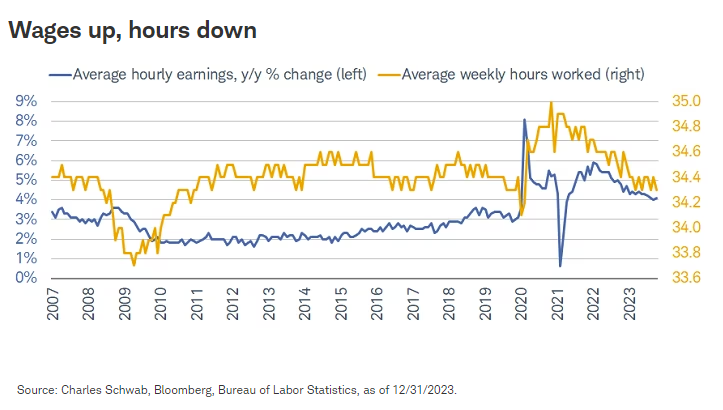

Another rub in Friday's release was the combination of an uptick in average hourly earnings and a downtick in average weekly hours worked, shown below. We're all for workers continuing to enjoy strong wage growth, but from the perspective of Federal Reserve policy, the data likely did not support rates being cut anytime soon. The good news is that real (inflation-adjusted) wage growth has kicked into higher gear courtesy of the deceleration in inflation. The trend of stronger-than-expected payrolls growth alongside weaker-than-expected hours worked suggests the labor market is still relatively tight, but that economic conditions warrant less demand for workers' hours.

Services employment starting to falter?

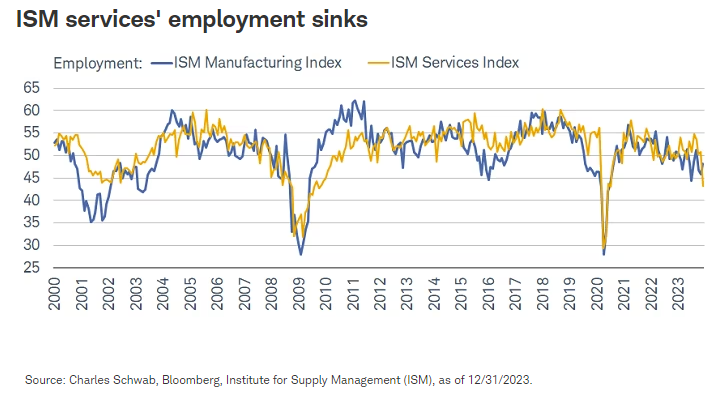

Separate from the jobs report on Friday, there were other employment-related tidbits inside the Institute for Supply Management (ISM) releases. The ISM does two surveys of company purchasing managers each month—one for manufacturing and one for non-manufacturing (services). Each survey has an employment component, and the release of the ISM Services employment data—shown below alongside ISM Manufacturing employment—was eye-popping. It represents a potential leading indicator of weaker services job growth to come given its plunge to the weakest reading since July 2020.

But here's a positive rub this time. When ISM releases their overall surveys, they generally only detail Manufacturing's employment component; leaving Services' employment component typically with little-to-no formal details. However, in the latest ISM report, they do mention that that the services sector continues to experience hiring difficulties; another sign of a still-tight labor market (although they did mention business services' layoffs).

That would be consistent with the waning confidence we've seen on the part of employees. Per the most recent Job Openings and Labor Turnover Survey (JOLTS) report from the BLS, the quits rate—which tracks how confident workers are in being able to leave their current job for another—fell in November to its lowest since September 2020. The pace of the quits rate's decline over the past year is on par with prior recessions, which suggests job-hopping is going out of (cyclical) style and workers are increasingly less confident in the health of the labor market.

In sum

The December jobs report adds uncertainty to the Fed's plans. Amid some ongoing hiring difficulties, but decelerating job growth, trying to assess a clear labor market narrative continues to be a challenge. Since the mid-1960s there has been an average of 23 months between the trough in the fed funds rate and the trough in the unemployment rate (with a range between 12 and 36 months). We will hit the 23-month point next month; while in this cycle, the unemployment rate troughed in the first half of 2023 at 3.4%.

The report may have added a few feet to the degree by which the market has gotten over its skis regarding rate cuts starting as soon as the March Federal Open Market Committee (FOMC) meeting. However, we do expect the Fed to begin cutting at some point this year, but perhaps not as soon as the market is expecting.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All