Multi-asset income strategies are becoming more popular, but some may bake in more risk than expected. The key is designing complementary exposures.

Investors are increasingly looking for strategies that can deliver on specific goals—and income is high on that list. That makes sense for people focused on meeting day-to-day expenses, preparing for retirement spending or even diversifying a broader portfolio.

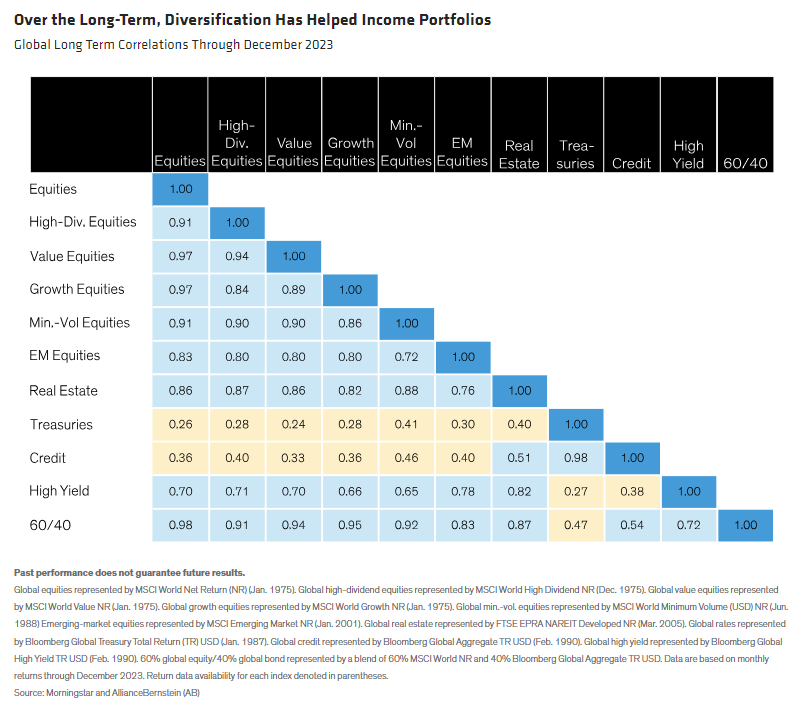

On the surface, building an income portfolio may seem straightforward. Just combine popular building blocks that have historically had lower correlations (Display), such as global Treasuries, which have posted a 0.26 correlation to global equities over the past 15 years or so. Other diversifying asset classes in the mix include dividend-focused stocks, high-yield bonds and real estate.

Market Dislocations Can Undermine Diversification

But those low correlations aren’t uniform over time. They rise and fall depending on market conditions, and they could increase—reducing diversification—at inopportune times.

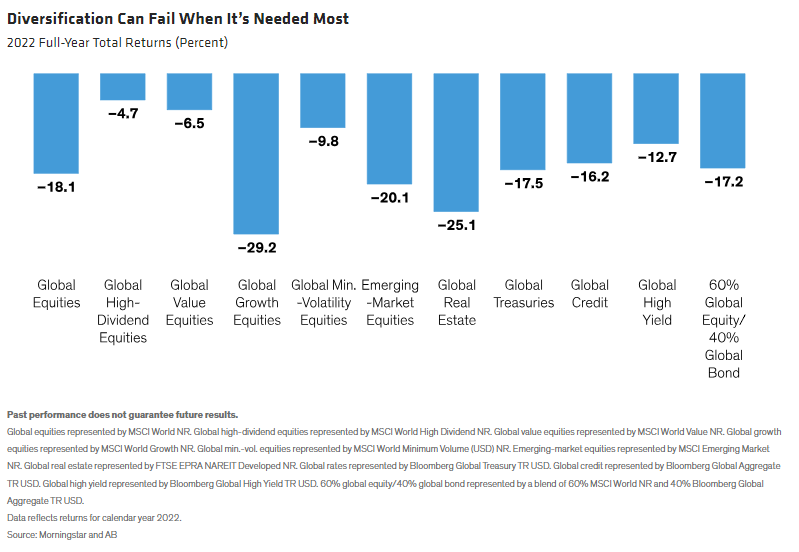

Market dislocations are seismic events that can do just that, causing diversification to fail just when it’s needed most. In the process, flaws can be revealed in the design of many income-seeking strategies. For example, in the disruptive market environment of 2022 (Display), global stocks and global treasuries—hallmarks of diversification—both fell by roughly 18%.

We think income-focused portfolios can be improved by taking the principle of complementary exposures a step further, with a more sophisticated approach to allocating risk.

Taming Unintended Equity Beta Exposure

Controlling equity beta is one way to buttress multi-asset income strategies. Many portfolios have sizable high-yield bond allocations, which makes sense given their history as strong income generators. But high yield also possesses equity beta—it tends to be more responsive to equity-market returns than are other parts of the bond market.

Investors can refine other portfolio design features to compensate, such as crafting a more defensive equity allocation. This can be done by integrating exposures to low-volatility and high-dividend equities, which have relatively lower equity betas to the broad stock market. This design feature can help balance pursuing income with upside market participation.

In 2022, for example, low-volatility stocks played much better defense in a punishing 2022 than did the broader stock market, with the MSCI World Minimum Volatility Index declining by 9.8% versus a sizable 19% loss for the broader Russell 1000 Index that year.

Enhancing Diversification by Style…and Beyond

Even these more value-oriented equity exposures can fall out of favor from time to time, so investors can take diversification a step further by integrating exposure to growth stocks in addition to broad cap-weighted equity exposure.

The objective of this enhanced combination is to ensure that a multi-asset income portfolio can effectively take part in the upside of strong growth-led markets. We saw such a growth-heavy rally in 2023, when the Russell 1000 Growth Index rose by nearly 43% versus 26.5% for the Russell 1000 and 26.3% for the S&P 500.

Asset classes beyond equities and high-yield bonds can play important roles, too. Real estate is driven by distinctive underlying fundamentals, making an allocation to that building block an effective counterbalance, while providing income. Exposures to segments of the bond market that are more interest-rate sensitive, such as global government bonds, can also help.

As long as capital markets exist, they’ll continue to face periods of turmoil, as they did in 2022, which was an extraordinarily difficult year with few places to hide. But even in those trying times, some asset classes held up better than others. While real estate fell by 25% and global equities by about 18%, value declined by 7.5% and low volatility by 9.8%. And that’s what managing downside risk is all about.

We think enhancing design can make a big difference in multi-asset income strategies over the long run and when markets are bumpy. Strategies focused too much on generating income and not enough on managing downside or upside participation could face a more challenging path. So, whether it’s tempering equity beta or adding asset classes with distinctive drivers, complementary should be the watchword.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© AllianceBernstein

More ETF Topics >