Corporate America—or at least as represented by the S&P 500—is delivering a quietly strong earnings season. With about 30% of S&P 500 companies having reported, results have broadly topped expectations. What's being revealed is that profit margins remain resilient, revenues continue to grow, and "beat rates" are running ahead of historical norms. Far from signaling a faltering economy, this quarter's earnings per share (EPS) so far suggest an economic expansion that's only cooling at the edges, not cracking at its core. In fact, perhaps most interesting is that none of the companies having reported so far are directly in the artificial intelligence (AI) space, suggesting that it's not the only economic driver.

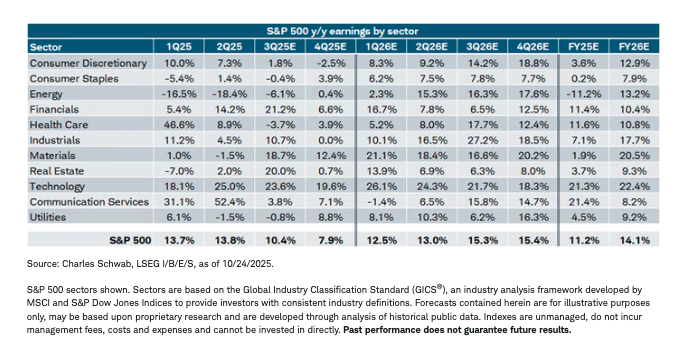

Using data from LSEG I/B/E/S, below is the comprehensive table for the S&P 500, including forward EPS estimates into next year. It covers aggregate data/estimates (bottom row), as well as for each of the 11 S&P 500 sectors.

The S&P 500's third quarter "blended" growth rate, which blends existing reports with estimates for remaining reports, is running at more than 10%, down from the pace of growth in the first half, but better than where estimates were at the start of reporting season. So far, the beat rate is 87%, which compares to the 30-year average of 67% and a prior four quarter average of 77%. In aggregate, S&P 500 companies have reported earnings 8% above estimates, which compares to the 30-year average of 4% and a prior four quarter average of 7%.

Most sectors are running at above-average beat rates, notwithstanding negative expected EPS growth for the Energy, Health Care, Utilities and Consumer Staples sectors. Perhaps no surprise, but the Tech sector's estimated growth sits atop the leaderboard—not just for the third quarter, but every quarter through next year's first half.

Defining earnings "hooks"

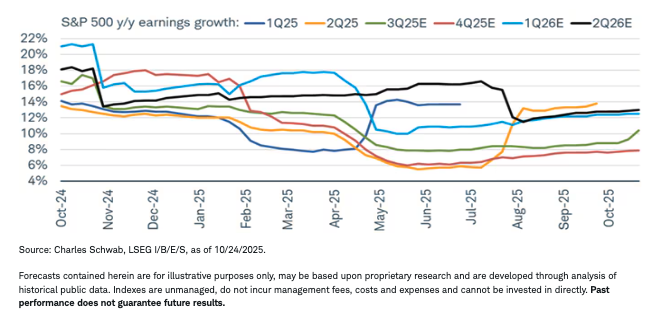

Per the chart below, EPS estimates for third-quarter (green) growth have been upwardly revised—not just since earnings season began, but since this past summer. Estimates for the fourth quarter (red) have also been trending higher since then. This is in stark contrast to the first half of the year (navy and yellow), during which estimates only hooked higher once earnings reports were already underway. One thing of note in this visual: the primary reason why 2026's first- (turquoise) and second- (black) quarter EPS growth rates hooked down this year was due to much better-than-expected first and second quarter 2025 growth rates (the base effects meant that next year's year-over-year growth were set to be lower).

Earnings "hooks"

Two narratives stand out as to earnings' resilience. First, margins are sturdier than feared with the blended net profit margin near 13% vs. its five-year average of 12%. Assuming no significant diminution of margins, it will mark the sixth consecutive quarter north of the five-year average. That durability—despite tariff instability and higher input costs—is pivotal for sustaining double-digit forward earnings growth.

Second, sector specifics matter. Semiconductors remain the single largest lift inside the Tech sector. Financials are reporting broad double-digit EPS growth across all five of the sector's industries. Even Utilities have gotten into the "beats" game, flattered by outsized contributions from AI/data center-related stocks. At the other end of the spectrum, in Health Care, downgrades and weaker EPS prints at several large constituents have pulled the sector's earnings lower.

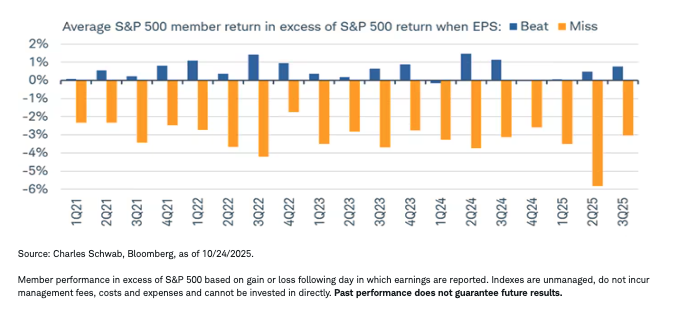

Beats rewarded, misses not

From a performance perspective, earnings season has been a solid underpinning for the market. As shown in the chart below, for companies beating EPS estimates, their average gain—relative to the S&P 500—that day is 0.76%. For those missing estimates, the average relative loss is -3.03%. Both readings are muted relative to history, but the trend over the past year has been one in which the beats have been rewarded at an increasingly better rate.

Beats increasingly rewarded

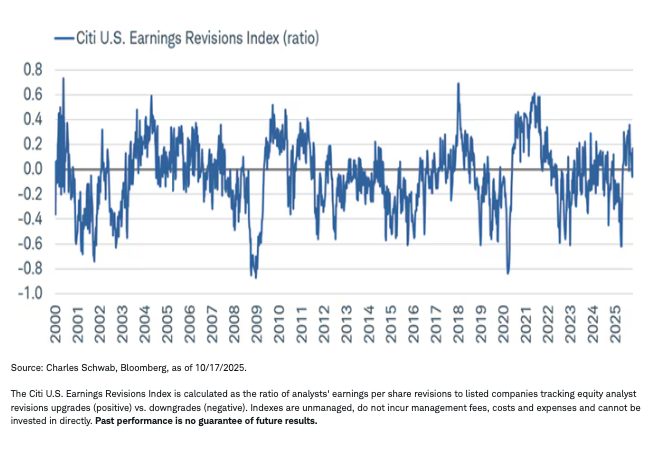

Not coincidentally, that has occurred as revisions have strengthened. Shown below is the U.S. Earnings Revisions Index from Citi; and for most of the second half of this year, it has been in positive territory. After taking a sharp, recessionary-like move lower earlier this year—when EPS estimates were in free fall to account for "Liberation Day" tariffs—the index has had an equally forceful rebound. Worth noting, however, is that this is not a leading indicator for market performance. The index was near all-time highs by late 2021, yet the S&P 500 experienced a bear market in 2022.

Earnings revisions remain healthy

In sum

Third-quarter earnings season is shaping up as another testament to U.S. corporate resilience. Tech's leadership continues to reflect multi-year AI and electrification investment waves. Industry-level growth suggests capital spending related to compute, data centers, and grid/power remains a tailwind even as broader manufacturing is mixed. Consumer-facing bellwethers and cyclical pockets are surprising positively, consistent with steady nominal demand. The drags from Energy and Health Care are not macro-systemic, while overall margins confirm late-cycle stability, not contraction. Above-trend margins and decent top-line growth argue that pricing power and cost discipline remain intact enough to offset wage and input cost pressures.

The S&P 500's double-digit expected EPS growth and unusually high beat rates underscore a still-healthy demand backdrop and disciplined cost control. To date, earnings reports are painting a picture of an economy that's bending a little under government and monetary policy uncertainty, but far from breaking. If forthcoming mega-cap and AI hyper-scalers reports don't upend the pattern, the earnings floor for 2025 looks firmer than the consensus feared a couple of months ago.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

This material is intended for general informational and educational purposes only. This should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decisions.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results.

Investing involves risk, including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, municipal securities including state specific municipal securities, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Diversification and asset allocation strategies do not ensure a profit and do not protect against losses in declining markets.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

Investment and Insurance Products: Not a Deposit • Not FDIC Insured • Not Insured by any Federal Government Agency • No Bank Guarantee • May Lose Value

The Charles Schwab Corporation provides a full range of brokerage, banking and financial advisory services through its operating subsidiaries. Its broker-dealer subsidiary, Charles Schwab & Co. Inc. (Member SIPC), and its affiliates offer investment services and products. Its banking subsidiary, Charles Schwab Bank, SSB (member FDIC and an Equal Housing Lender), provides deposit and lending services and products.

This site is designed for U.S. residents. Non-U.S. residents are subject to country-specific restrictions. Learn more about our services for non-U.S. residents, Charles Schwab Hong Kong clients, Charles Schwab U.K. clients.

© 2025 Charles Schwab & Co., Inc. All rights reserved. Member SIPC. Unauthorized access is prohibited. Usage will be monitored.

© Charles Schwab

Read more commentaries by Charles Schwab