Research Affiliates

Growth Without Price Distortion

Every dollar in a growth equity index reflects two decisions: which companies to own and how much of each to hold. Indexes form intricate systematic rules to make the first decision. The second decision—position sizing—is usually determined by market-cap weighting.

Reading Between the Lines: NLP for Long-Horizon Factor Investing (Part 1 of 2)

When it comes to systematic investing, numbers tell only part of the story. Traditional quantitative models rely on prices, earnings, and balance sheet data, but words matter too.

Guided by Fundamentals: Navigating Emerging Markets with Value

Emerging markets offer important exposure to economic growth through rapid industrialization, natural resource endowments, and strong demographic dynamics.

Guided by Fundamentals: Navigating Emerging Markets with Value

As globalization gives way to reshoring and resurgent resource nationalism, emerging markets may offer fresh alpha opportunities through their ability to supply the raw materials required to fuel the AI boom.

The Momentum Trade That's Still on Sale

Right now, AAI’s two highest 10-year expected return forecasts are for large-cap value equity strategies outside the United States—Emerging Markets RAFI and Dev ex US Large RAFI. AAI’s expected return model anticipates valuations for equity strategies to mean revert and therefore tends to elevate out-of-favor regions and styles, predicting higher future returns for recently underperforming equity indices.

The Impact of AI on SaaS: A Risk Framework for Investors

Rapid development of AI technology poses a direct threat to the SaaS sector, but the risks are not necessarily terminal or universal and vary based on time horizon.

When Will AI Be Both Powerful and Profitable?

If the economic life of AI hardware is shorter than its accounting life, reinvestment needs are higher than reported depreciation suggests. What appears to be capital deepening by hyperscalers is largely capital churn.

Why Value, Quality, and Momentum Belong Together

Investing is an exercise in decision making under uncertainty. No single signal—no matter how intuitive or well supported by history—captures the full complexity of markets.

Should Trend Follow Carry: Lessons from Bonds, Gold, and 2022

Carry is an important return driver for multi-asset futures and forwards. Simple trend signals have benefited from trading in line with, not against, the carry of an asset.

Why Global Diversification Matters More Than It Has in Decades

U.S. equities had another strong year in 2025. Returns were impressive, headlines were dominated by large-cap growth, and investor confidence remained high. Yet a quieter and more important story unfolded beneath the surface. Non-U.S. equities meaningfully outpaced their U.S. counterparts.

Conglomerates and the Disappearing Diversification Discount

Whether these diversified firms can maintain their positions indefinitely is an open question, but market history suggests the competition always catches up.

2025’s Implications for the Future: “Some Like it Hot"?

In this article, we look both back and forward, first at the 2025 capital markets to analyze not just what happened but also how it fits in the historical context and what we believe it means for 2026 and beyond. We then pivot to our return expectations for major asset classes in the next decade.

Rising Expected Returns in the Land of the Rising Sun

In the last 10-plus years, investors have grown accustomed to Japanese financial assets lagging their global counterparts.

Trifecta: A Fundamental Revolution in Indexing

As index investing continues to evolve, it does not have to be towards ever-expanding complexity. Sometimes progress comes from asking simpler questions and answering them consistently.

A Review Through Q3 2025

As the final quarter of 2025 begins, it's a critical moment to look back at the preceding three quarters. Each year carries its own narrative, and 2025 was no exception. Markets trended downward early in the year owing to trade-talk-driven uncertainty, reaching a crescendo in volatility following the unexpected announcement of significant tariffs in April.

Why Hold Expensive Slow-Growing Stocks?

In their latest article, Why Hold Expensive Slow-Growing Stocks? An Alternative Framework for Value and Growth Indices, Chris Brightman, Campbell Harvey, Que Nguyen, and Omid Shakernia, argue that traditional style-box construction forces investors to hold stocks that are neither true “value” nor true “growth”—notably, expensive, slow-growing companies that have historically underperformed.

Stop the Losses!

Even thoughtfully managed strategies may underperform or suffer sharp losses. This can encourage poorly timed emotional decisions that exacerbate the decline. A systematic risk-management framework that employs stop losses can help minimize such behavioral biases.

Active Dreams, RAFI Delivers: Active vs. RAFI Performance in Broadening and Narrowing Markets

Since the recovery from the global financial crisis (GFC), the S&P 500 has delivered one of the strongest and longest bull markets in U.S. history, with 16.2% annualized returns.

Reinventing Cap-Weighted Indexing

There has not been a fundamental innovation in broad-market cap-weighted indexing in decades. Until now. With the Research Affiliates Cap-Weighted Index (RACWI), we introduce a fresh approach designed to fix a costly but little-known “bug” in cap-weighted indexing.

A Quiet Place? Markets Are Remarkably Hushed—Priced for Perfection and Poised for Turbulence.

In the 2018 thriller A Quiet Place, silence masks imminent danger. Today's equity markets offer a similarly deceptive peace.

Eastern European Equities: From Opportunity to Caution (Part Deux)

Last summer, we highlighted the investment potential in Eastern Europe.

False Choices, Real Costs: Structural Flaws in the Growth–Value Duality

Standard value and growth style indexes categorize stocks based on a composite signal that combines valuation (cheap vs. expensive) and growth (fast vs. slow) metrics.

Must Value Be Anti-Growth?

The RAFI™ Fundamental Index has a value tilt, but to characterize it as a value index would be an oversimplification that misses the important advantages that the fundamental index offers above standard “value” index approaches.

Expand Your Mind and Your Commodity Universe

For good reasons, many investors have a love-hate relationship with commodity investments. Operationally, the annoying K-1 form complicates tax filing, although thankfully the industry has started to launch “no K-1” funds.

The Fed’s Waiting Game: Why It’s Good News for Bond Investors

This is the first in a three-part series outlining why I believe bonds are set to outperform. Here, I focus on the Federal Reserve’s dual mandate, the June 2025 meeting, and why the Fed’s approach is positive for bond investors. Parts 2 and 3 will address valuation, politics, recession risk, and the secular horizon.

How Can “Smart Beta” Go Horribly Right?

Smart beta strategies have endured a prolonged stretch of disappointing results, falling short of investor expectations. This article explores the underlying causes of that performance and outlines why the conditions ahead could be more favorable.

Passive Aggressive: The Increasing Risks of Passive Dominance

Passive capitalization-weighted index funds now surpass active management in aggregate investor allocations.

Developed Ex-U.S. Equities: A Valuation Opportunity Hiding in Plain Sight

Despite strong year-to-date performance, developed ex-U.S. large-cap equities continue to trade at far more attractive valuations than their U.S. counterparts.

Stimulus Does Not Stimulate

Common sense and economic theory often collide. Take the stubborn belief that government stimulus spending and debt issuance reliably boost economic growth. It is a simple and seductive idea—when the economy falters, the government can step in, inject capital, and jumpstart growth.

Walking the Tightrope: Trend Following’s Tricky Tradeoffs

Trend-following strategies can offer attractive, positively skewed returns, with large positive outperformance often coinciding with large equity selloffs, thereby offering tail protection.

Gold $5,000?

While gold has offered some protection during stock market downturns by either rising or declining by less than equities, its current high price levels and historical patterns suggest that future returns may be limited.

Why Tariffs Won’t Solve Our Trade Problem

Simply stated, the U.S. doesn’t save and invest enough. As a result, we pay for too many of our imports by borrowing from our trading partners.

Small Caps, Big Opportunities: Investing Beyond Large-Cap Stocks

In an era when a select group of tech behemoths has dominated market returns, investors are growing increasingly wary of the concentration risk it poses.

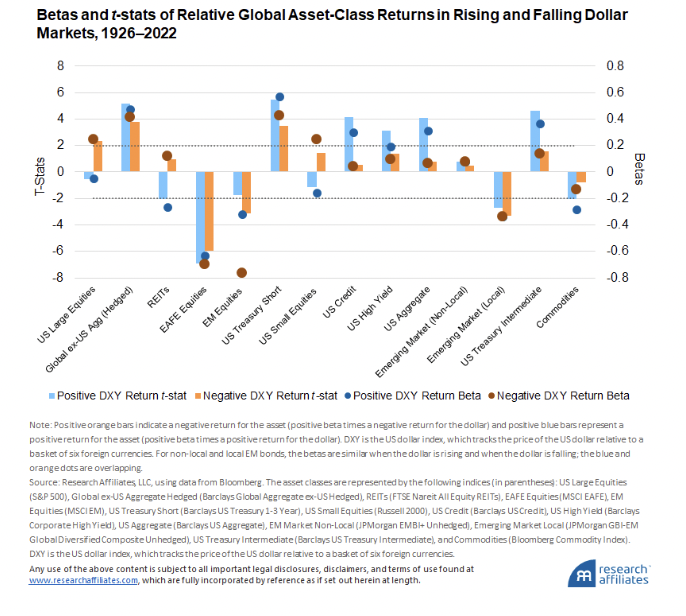

Carry Trade Destruction

Lost in the focus on the bludgeoning that tariff policy has had on equity markets, is the impact on global currencies. From the end of February through April 3rd, the U.S. Dollar is down 5.1% relative to other developed market currencies (DXY). In addition, we’ve also seen a violent unwinding of the popular currency carry trade.

The AI Boom vs. the Dot-Com Bubble: Have We Seen This Movie Before?

The parallels between the AI narrative driving the current market and the dot-com bubble of a quarter century ago raise important concerns for investors.

The EV Shakeout

The EV shakeout is underway. When the dust settles, only a few players will remain. Many more will be relegated to the scrapyard of failed ambitions.

Beta Paradox: Why REITs and EM Stocks May Beat/Outshine U.S. Large Caps

According to Research Affiliates’ Asset Allocation Interactive (AAI) online capital market expectations tool, U.S. large-cap equities are expected to yield 3.4% annually over the next 10 years compared to 9.1% for EM equities and 7% for REITs. This left many webinar participants wondering, How does this extra return square with these assets having similar betas?

Adventures of The OG Quant

Dean LeBaron’s name may not be familiar to many readers, especially those who only began their careers in the 21st century. But all of us should know who he is. Before there was even a term for it, Dean was the first truly successful quant.

Current Constituents CAPE

The article introduces CC CAPE, a modified version of Shiller CAPE, which corrects index biases for improved forecasting. While both measure market valuations for long-term return forecasting, the CAPE Spread helps gauge sentiment for medium-term predictions.

Trump 2.0: The Deregulation Agenda – No New Rules?

Deregulation is among President Donald Trump’s most enduring policy themes. In his 2016 campaign, he called for widespread deregulation and made it a central plank in both his economic and energy platforms.

Asset Allocation Interactive at 10 Years: The Good, the Not Too Bad, and the Ugly

Ten years ago, Research Affiliates launched the Asset Allocation Interactive online tool, making our CMEs freely available to the public. With one full cycle complete, we can see what has worked well and where we can improve.

Capitalization-Weighted Indexes, RAFI, “Smart Beta,” and Factors (JPM Series)

Index funds emerged in the early 1970s and were designed to match rather than beat the market. For decades, they were associated with the capitalization-weighted (CW) market indexes that defined their investment approach.

The Efficient Market Hypothesis vs. Roaring Kitty (JPM Series)

Much of modern finance falls into one of two camps, neoclassical finance and behavioral finance. The former posits efficient markets, the latter posits the opposite.

Past, Present, and Future of Modern Finance (JPM Series)

Accumulating inconsistencies in the prevailing paradigm then trigger a crisis, leading to the emergence of new theories and ideas, resulting in a paradigm shift where the old framework is rapidly replaced by a new one.

Watch Out for Expensive EM Markets

The latest AI-driven euphoria, led by big tech names that include NVIDIA, has dominated investment sentiment in the post-COVID era. Of course, many investors know that this has driven the U.S. equity market to an all-time high, stretching valuations to an extreme level (U.S. CAPE is at the 98th percentile of historical observations!).

The Shifting Sands of Alternative Risk Premia Strategies

The 2022 broad market downturn across major asset classes came as a nasty surprise to investors. Historically, such an event is very rare, and no one was expecting to see almost all asset classes down for the year. Yet, even though it might seem as if diversification was of no help in 2022, the story changes if we look beyond the major headline asset classes.

Change Required: Immigration Reform is an Economic Necessity

News of that day included rioting in northern England, apparently in response to misinformation spread online claiming the person who stabbed to death three children and injured eight others in Southport was a Muslim immigrant.

Elections and the Stock Market: Polarization Trumps Politics

How an election affects stock market performance depends more on how close and contentious it is than on whether the winner is Republican or Democrat, liberal or conservative.

Nixed: The Upside of Getting Dumped

No one enjoys getting dumped. This holds true in finance and investing as much as it does in romantic relationships. When companies are dumped from the major indexes, their managers and shareholders may feel jilted and their stock may flounder post-breakup.

Time to Reconsider Europe

Following Russia's invasion of Ukraine in the early months of 2022, and the subsequent sanctions imposed by the U.S., some investors were forced to liquidate their Russian investments. Many investors, uncertain about the potential scope of the coming war, also took the opportunity to liquidate their investments in all of Eastern Europe.

Are You a Climate Investor or Growth Investor?

First-generation low carbon equity benchmark indices were developed almost a decade ago with the goals of mitigating climate risk and preparing for the transition to a low carbon economy.

A Stealth Tax on Prosperity

While governments responsibly issue debt to fund public investment and dampen the business cycle, the US federal government has borrowed at an increasingly prolificate pace over recent decades.

Learn from Last Tech Bubble to Embrace GenAI Mania

These are only some of the exciting new applications on everyone’s lips at business gatherings these days, where the conversation often veers to artificial intelligence, which has become the latest “new new thing.”

Alternative to a Manic AI Market: RAFI vs Equal-Weight

Over recent decades, the hot tech trends (from search to cellphones to social media to the digital economy and now to AI) have been a predominantly American story.

The Only Free Lunch in Investing

Nobel laureate Harry Markowitz famously asserted that diversification is the only free lunch in investing. His insight was simple yet profound: by diversifying across assets, investors can achieve higher returns without necessarily increasing risk.

Active Value Investing: Avoiding Value Traps

After a decade in the wilderness, value investing roared back to life in 2022, led by long-forsaken sectors such as energy, industrials and even certain retailers. Many portfolios had either intentionally or unintentionally migrated heavily towards “growth at any price” exposures and were caught wrong-footed that year.

The Fed's Wait, Wait, Wait, Then Drip, Drip, Drip Strategy. Can We Achieve a Soft Landing?

It is certainly a confusing economic environment. Jobs growth is strong yet there are constant reports of high-profile company layoffs. The yield curve is inverted suggesting a recession yet the stock market is at a record high.

Know the Strike Zone and Keep Swinging!

As the calendar closed on 2023, investors were once again treated to magnificent returns in their stock and bond portfolio.

Harnessing Volatility Targeting in Multi-Asset Portfolios

Following a period of relatively calm asset markets from 2013-2019, in which the CBOE Volatility Index (VIX) averaged just below 15, volatility in asset markets has returned1 and investors have been looking for ways to protect themselves.

The Current Fiscal Path is Unsustainable. Will We Do the Right Thing?

“The current fiscal path is unsustainable”. This stark warning comes from the US Treasury Department’s Bureau of the Fiscal Service’s fiscal year-end projections1. Based on current appropriations and tax law, these projections display steadily rising federal spending and flat tax receipts, as a percentage of GDP.

Long Periods of Boredom

Trench warfare in the early 20th century has been described as long periods of boredom punctuated by moments of terror.

From Abundance to Austerity: Why the Next Decade Won’t Be Like the Last

Higher interest rates and inflation are likely to usher in a decade of policy restraint, limited liquidity and macro volatility, pressuring equities and motivating investors to reconsider tactical asset allocation and embrace real assets.

What “Smart Beta” Means to Us

As with most new expressions, “smart beta” is in the process of seeking an established meaning. It is fast becoming one of the most overused, ill-defined, and controversial terms in the modern financial lexicon.

How Can “Smart Beta” Go Horribly Wrong?

In smart beta, we find that factor returns—net of changes in valuation levels—are much lower than recent performance suggests. In fact, many of the most popular new factors (some 458 at last count) have succeeded solely because they have become more expensive.

We are All Quants. The New Era of Systematic Investing

With artificial intelligence, systematic investing is entering a new era of disciplined decision-making. Yet, firms face many snags. Rigorous implementation requires collaboration among skillful investment, technology, and quantitative capabilities.

Rocking with RAFI: International Evidence

With negligible incremental risk, a RAFI Global Index hypothetically outperformed a Cap-Weighted Global Index by 40 bps per annum and a Cap-Weighted Global Value Index by 2.2% from 2007 to 2022—a 16-year period covering the long value rout and its aftermath.

Long‑Term Return Expectations, Near‑Term Outlook, and the Inverted Yield Curve

Research Affiliates explain why their long-term return forecasts have risen across asset classes and the implications of their near-term outlook for U.S. recession.

Inflation: Don’t Pop the Champagne (Yet)

While inflation dipping below 3% has been welcome news for investors, it’s still early to claim that inflation has been reined in. Our simple analysis shows that inflation rising in the latter half of 2023 would not be surprising.

Odds of a Hard Landing Are Increasing

The Fed’s refusal to pause rates through the first five months of 2023 raises the odds of a hard landing. The magnitude of the yield-curve inversion has increased the risk inherent in the US banking and financial systems. The impending recession is unnecessary and self-inflicted.

Tesla - Has the Time of Reckoning Come?

Tesla’s shares fell by more than 14% on Tuesday, after plunging by 65% in 2022.

History Lessons: How “Transitory” Is Inflation?

The US Federal Reserve Bank’s expectations for the speed of reverting to 2% inflation levels remains dangerously optimistic.

Where’s the Beef?

In the 1980s there was a famous TV ad for Wendy’s with the tagline “Where’s the beef?”.

Quantifying the Impact of Direct Indexing

We apply five levels of customization to four developed-market equity strategies to quantify the impact of customization (or direct indexing).

Carbon Intensity for Climate Mitigation: Clearing Up “Scaling” Confusion

Investors can choose one of two popular scaling methods for carbon emissions comparisons across companies. Our analysis guides investors in making this important decision.

No Excuses: Plan Now for Recession

Now is the time to engage in risk management to retain your competitive advantage once the economy emerges from the slowdown.

Rising Risk of Stagflation

Trillions of dollars of deficit spending financed by money creation over the past two years caused today’s soaring inflation.

Duration Management for the Next 40 Years

Traditional long-only fixed income managers had one of the worst quarters on record in Q1 2022 as higher interest rates left “bottom up” portfolios overweight duration.

ESG Is a Preference, Not a Strategy

A portfolio’s return is driven by its investment strategy—a set of decisions that governs allocation and timing of capital among the portfolio’s positions.

Inflation Is Here! What Now?

Inflation is rising rapidly, not an unexpected outcome given governments’ pandemic policy response of ballooning deficits and soaring government debt.

Did I Miss the Value Turn?

The value rebound that started in September 2020 gave up nearly half its gains by mid-May 2021 as the recovery faltered with the onslaught of the highly contagious Delta variant. But vaccination has proven highly effective, and as the unvaccinated around the world become vaccinated, the prospect of a reinvigorated economy is good. Is now a second chance to rebalance into value stocks?

Predicting Equity Returns with Inflation

Rather than predicting what will happen to inflation in the future—a particularly arduous and humbling task—we ask a simple question: What can past inflation dynamics tell us about the equity market’s future returns?

Revisiting Tesla’s Addition to the S&P 500: What’s the Cost, Before and After?

We have observed that additions and deletions to the S&P 500 Index follow a dependable pattern: additions underperform and deletions overperform over the subsequent 12-month period.

The Fall of the Titans!

The performance of a market-cap-weighted index is driven by a handful of stocks with the largest capitalizations, but these stocks do not remain at the top for long. A smart beta multi-factor strategy is a good solution for investors concerned about the concentration risk of a passive market-cap tracker.

Factor Timing: Keep It Simple

Factor timing is the ability to add value to an investment strategy by altering the exposure to various factors through time.

Big Market Delusion: Electric Vehicles

The “big market delusion” is when all firms in an evolving industry rise together, although as competitors ultimately some will win and some will lose.

As Duration Dies, Equities Rise

We compare the current value of bonds versus stocks within the context of the equity risk premium. We couple this analysis with an evaluation of possible Fed policy direction. Our conclusion is that risk assets, such as US equities and corporate bonds, are poised to benefit as are gold and other commodities due to tumbling real yields and dollar weakening.

How COVID-19 Vaccines and Brexit Create the Trade of the 2020s

In late 2020, a new kid emerged on the bargain-of-the-decade block. UK stocks, and notably UK value, reached very cheap levels relative to value stocks in other developed economies. Today, UK value remains at remarkably low valuations relative to most of its fundamentals.

Reports of Value's Death May Be Greatly Exaggerated

Rob Arnott: “There hasn’t been a better time to be a value investor at any other time in my career. I look back at the tech bubble and I never thought I would see valuations stretched the way they were then. We're back to that, and then some." We invite you to revisit “Reports of Value’s Death Have Been Greatly Exaggerated” now published in the Financial Analysts Journal.

Surprise! Factor Betas Don’t Deliver Factor Alphas

By buying or overweighting characteristics-based factor exposure and selling or underweighting beta-based factor exposure, investors can position their portfolios to reap the rewards of factor investing while bearing less risk.

Beware the Shocks in the Road

Massive growth in central bank balance sheets via quantitative easing, debt monetization, and firing of “big bazooka” stimulus packages brings renewed focus to potential shocks in the business cycle. An awareness of the macroeconomic “shocks” and their impact on asset prices should be incorporated in investors’ tactical asset-allocation decisions.

Is Diversification Dead?

Over the last dozen years, investors holding the classic US 60/40 portfolio were substantially better off than their diversified peers, yet now is not the time to abandon diversification and diversifying asset classes. We believe it is imprudent to trust that escalation in valuations will continue unabated into the next decade...

Bitcoin: Magic Internet Money

The sage advice to “know what you are investing in” is being dangerously overlooked by both novice and seasoned investors when it comes to bitcoin. A former bitcoin miner explains why the price of BTC is nearly certainly a bubble and likely manipulated. Investors should proceed with extreme caution.

Tesla, the Largest-Cap Stock Ever to Enter S&P 500: A Buy Signal or a Bubble?

On December 21, Tesla will be the largest company ever to enter the S&P 500 Index. Tesla’s skyhigh valuation, which meets our real-time definition of a bubble, conforms to the observation that market-cap-weighted indices buy high and sell low—the antithesis of prudent investing.

Book Value Is an Incomplete Measure of Firm Size

Adding intangible assets to book value provides a more robust measure of firm capital. But, just as a home buyer considers a host of variables when evaluating the price of a new house, we prefer to use multiple metrics, not book value alone, to get the most complete picture possible of a firm’s valuation.

The Risks to a Robust Recovery

Cam Harvey outlines seven risks that have the potential to derail the economic path forward. He believes in the possibility of a robust recovery, but prudence dictates going through the exercise of listing the risks to the recovery and assessing their economic and financial implications.

Is ESG a Factor?

Applying the definition of factor robustness that was established by our Research Affiliates colleagues in a 2016 award-winning paper, we determine ESG is not a factor. Nevertheless, the importance of ESG as an investing strategy is undeniable. We explore how greater clarity around defining ESG can quicken the pace of ESG integration in equity portfolios.

A Quick Survey of "Broken" Asset Classes

Pundits, prognosticators, and even investment boards often make misleading declarations that an asset class is broken, that its prospects for earning investors a reasonable future return are very dim. These proclamations can lead to investors’ abandoning these assets to chase recent winners.

The COVID-19 Crash and the Abandonment of the Pensioner

Between mid-February and late March 2020, we saw a “take no prisoners” market crash. Anything with a whiff of perceived risk crashed, in direct proportion to its perceived risk. The only assets that soared—because of tumbling interest rates—were long Treasury bonds, and with them, the net present value of pension obligations.

Reports of Value's Death May Be Greatly Exaggerated

The Fama–French value factor, and value investing in general, has suffered an extraordinarily long 13.3 years of underperformance relative to the growth investing style. The current drawdown has been by far the longest as well as the largest since July 1963. Arnott, Harvey, Kalesnik, and Linnainmaa examine the potential causes of value’s underperformance and provide estimates of value’s performance relative to growth’s performance under different revaluation scenarios over the next decade.

FOMO vs. Fundamentals

Unlike most macro investors who are event-driven, RBA has always strictly followed fundamentals. Our models and indicators have been time-tested in multiple cycles over the past 30 years, and a deliberate and disciplined approach has so far served us well in the current unprecedented environment.

Too Soon? Pandemic Policy Response Raises Risk of Inflation

The Fed’s $5 trillion bazooka, helicopter drops of cash, and a tripling of deficits over the next two years imply a future bout of high and volatile inflation unless fiscal policy nimbly pivots to help prevent the toxic side effect of a spike in inflation. Is that expectation realistic?

As Markets Burn

Major adjustments in capital markets around the globe have changed our long-term expected return forecasts for the 100+ assets we model. Before the corona crash we forecast long-term real returns for US equities to be only 1% a year. Now new, lower valuations suggest higher returns.

Leading in Uncertain Times

In times of uncertainty, good leaders lean into crisis and are able to fully engage, motivate, and inspire their team. The serious and stressful challenge of the COVID-19 crisis demands that leaders embrace flexibility, curiosity, and openness to diverse perspectives.

The Distinction between a Company and Its Stock Price

We at Research Affiliates recently conducted our first virtual All Hands meeting after finding ourselves working from home in the wake of the COVID-19 crisis. As CIO, I responded to questions about our investment strategy. Katy Sherrerd, CEO, and Jeff Wilson, Head of Distribution, asked me to elaborate more broadly on my response to one of the questions submitted by email the day prior.

With Volatility Comes Opportunity

Uncertainty continues to dominate global securities markets and heightened volatility is the result. Feifei Li, partner and head of equities, asks Rob Arnott, the founder and chairman of Research Affiliates, about the implications of increased volatility on investment strategies and where investors can find the best opportunities.

This Too Shall Pass

Rob Arnott shares his perspective on the ongoing market crisis in a Q&A with Jonathan Treussard. He suggests the time to buy is when investors are at “peak fear.” In the weeks ahead, that point will come and bargains will make themselves self-evident to the disciplined investor. The window of opportunity will be short, but highly rewarding over the longer term.

Oh My! What’s This Stuff Really Worth?

What impact will coronavirus and market volatility have on your portfolio?

Reports of Value's Death May Be Greatly Exaggerated

The current drawdown has been by far the longest as well as the second largest since July 1963, eclipsed only by the tech bubble from 1997 to 2000. Arnott, Harvey, Kalesnik, and Linnainmaa examine the potential causes of value’s underperformance and provide estimates of value’s performance relative to growth’s performance under different revaluation scenarios over the next decade.

Forecasts or Nowcasts? What’s on the Horizon for the 2020s

Now is the season for forecasting as one decade turns into the next. Pundits and market prognosticators too often treat nowcasts as true market forecasts, which can be very dangerous for investors’ financial health. Our forecasts for the decade ahead rely on empirically driven quantitative models.

Plausible Performance: Have Smart Beta Return Claims Jumped the Shark?

To get the attention of smart beta investors in a crowded marketplace, some smart beta providers are laying claim to performance that appears implausible. So what is plausible? We look at historical live performance to answer this important question.

Standing Alone Against the Crowd: Abandon Value? Now?!?

Key Points

- In a prolonged anti-value momentum-driven rally, it’s easy and natural to forget the long-term value proposition of a rebalancing discipline.

- The evidence and intuition underlying a contrarian value investing discipline has proven merit in cycle after cycle across history.

- By steadily rebalancing against the market’s most extravagant bets, RAFI strategies are positioned to recoup accumulated shortfall at the cycle’s turn, delivering meaningful long-term value-add.

- The continued outperformance of today’s most dominant companies is unlikely to be sustainable in the long run.

The Advisor’s Case for Smart Beta Direct Indexing

Smart beta direct indexing is an increasingly accessible implementation route that accommodates tax-loss harvesting and customizations based on client preferences and circumstances.

Bubble, Bubble, Toil and Trouble

Looking back over the last 15 months, the authors assess their success at identifying asset bubbles and anti-bubbles in April 2018. The scorecard is in their favor. More importantly, however, they review how their definitions of a bubble and an anti-bubble continue to provide useful insights for where investors can find value in today’s global markets.

Dismiss MMT at Your Peril

Modern Monetary Theory (MMT) informs today’s progressive policy agenda, even though many prominent economists consider it flawed, nonsense, or just plain wrong.

The Inverted Yield Curve

Cam Harvey speaks to the currently inverted yield curve as an indicator of a slowing economy, further expounding on his Conversations of January 2019.

Strike the Right Balance in Multi-Factor Strategy Design

One thing is for sure, investing means buying and selling, and these two activities aren’t free. Regardless of how promising the strategy looks on paper, its benefits will be reduced to some degree through its implementation. A worthy goal, therefore, is to limit the toll implementation takes on a strategy’s execution.

The Flattening Yield Curve

Cam Harvey looks at the yield curve today through the lens of his 1986 pioneering work on yield-curve inversions and their foreshadowing of economic downturns.

The Challenges of Diversity Investing

The business case for diversity is compelling, but the investment case for diversity is less clear-cut. We suggest, therefore, that investors who seek to promote diversity and its business benefits combine diversity with known drivers of excess returns.

The Biggest Failure in Investment Management: How Smart Beta Can Make It Better or Worse

The biggest failure in investment management—the gap between the returns realized by the investor and the returns earned by the strategy or fund the investor owns—typically remains in the shadows with the glare of the spotlights focused on alpha. Smart beta is no exception. We propose two ways to reframe the client performance review that we believe will result in better long-term outcomes.

Ignored Risks of Factor Investing

Factor investing, an investment approach which targets specific stock characteristics such as value or momentum, is becoming a stronghold of investor portfolios.

Alternative Risk Premia: Valuable Benefits for Traditional Portfolios

An alternative risk premia strategy that relies on robust factors within a liquid, transparent, and disciplined framework has the potential to improve the long-term return prospects of traditional portfolios and to reduce their downside risk.

Rebalance or Rush Hour?

Embracing a disciplined approach to rebalancing can lead to better long-term investment outcomes. Overcoming the natural tendency to wait-and-see before repositioning our portfolios can be a difficult, but worthy, goal for investors to pursue. Advisors can help investors surmount this and other behavioral hurdles by adopting a systematic rebalancing approach that effectively institutionalizes contrarian investment behavior.

Where Is the Global Economy Going?

Evidence shows that the yield-curve slope and equity returns provide signals of similar direction in the economy, allowing investors to nowcast with relative confidence. Today, those signals indicate that several developed markets—in particular, Japan, Germany, and the United States—are ominously close to entering a correction phase.

Pundits Predicting Panic in Emerging Markets

A rational analysis of the emerging markets affirms our belief that now is the time to buy, not sell. The panic being peddled by pundits today is simply not justified.

Buy High and Sell Low with Index Funds!

Traditional index funds match market performance and have negligible trading costs with low tracking error—or do they? Not actually—they routinely buy after high price appreciation and sell after high price depreciation. They also have significant trading costs from adding and deleting stocks. We show how index providers can construct better-performing indices that are less prone to performance chasing and have lower turnover.

Is Your Alpha Big Enough to Cover Its Taxes? A Quarter-Century Retrospective

Investors and their advisors must be alert to managing both pre-tax and after-tax alpha in order for investors to realize the highest possible return from their taxable portfolios. Increasingly, the opportunities to accomplish both goals are within reach of investors through, for example, tax-advantaged smart beta strategies and tax-efficient vehicles such as ETFs.

Food for Thought: Integrating vs. Mixing

Although a naïve comparison appears to favor the integrating approach to multi-factor strategy construction, after taking into account both quantitative and qualitative considerations, many investors—those seeking transparency, diversification, minimal governance oversight, and low fees—may find mixing is a more sensible choice.

Yes. It's a Bubble. So What?

With sky-high valuations in the US stock market, and what we believe is a tech bubble that has dangerous implications for other areas of the market, we suggest four actions investors can take now to avoid the inevitable bursting of the bubble, and which will likely benefit their portfolios’ long-term performance potential.

Unlocking the Performance Potential in ESG Investing

By combining a tilt toward companies that display financial discipline and that embrace corporate diversity with the return engine of a fundamentally weighted portfolio, we believe investors in environmental, social, and governance (ESG)–related strategies have the opportunity to earn superior long-term risk-adjusted returns.

Performance Measurement: How to Do It If We Must

Assessing our portfolios’ performance is a necessary activity, but by being aware that measurement over shorter time horizons is dominated by noise, we can better resist the natural human instinct to “do something”—typically selling the underperforming investment at exactly the wrong time—if near-term performance falls below expectations.

When Value Goes Global

When the value trade goes global, investors are poised to benefit. Evidence from the international equity, bond, currency, and commodity markets indicates that the value premium is a global phenomenon that can offer important portfolio diversification. However, the devil is in the details: we argue that the successful implementation of global value strategies critically depends on an economically motivated design.

Craftsmanship in Smart Beta

While somewhat at odds with today’s big-data, warp-speed approach to life and work, thoughtful craftsmanship—the product design and implementation elements that are tangible, measurable, and impactful—can create positive, persistent results in portfolio performance.

CAPE Fear: Why CAPE Naysayers Are Wrong

Beware the consequences of assuming that elevated CAPE ratios are here to stay, but if they are the "new normal," low future returns are likely to be the "new normal" as well.

Part 3 Building Portfolios: Diversification without the Heartburn

Part 3 Building Portfolios: Diversification without the Heartburn The wisdom of diversifying investor portfolios across a wide range of asset classes is indisputable. But diversifying client portfolios beyond mainstream stocks and bonds comes with challenges, starting with clients’ unfamiliarity with diversifying asset classes and a propensity for clients to regret diversifying when results disappoint.

The Bubble That Never Came (and Other Misconceptions about Treasury Bonds)

A 10-year US Treasury note yielding just little above 2% does feel expensive. Yet we should not be misled by appearances. Our research shows that, contrary to common wisdom, Treasury bonds are only moderately overvalued. All in all, bonds are not as unattractive as a simple historical comparison of their yields may suggest.

Can Momentum Investing Be Saved?

Momentum is one of the most compelling factors in theoretical long–short paper portfolios, but live results of momentum strategies fall short of theoretical returns. Thoughtful implementation, a careful sell discipline, and an avoidance of stocks with stale momentum can narrow the gap between paper and live results.

Part 2 Risk: Preparing Clients for an Uncertain Journey

If we think of expected return as the likeliest long-term “destination” of our investment portfolio, we can then think of risk as the uncertainty in the “journey” to that destination. Advisors serve their clients well by helping them understand the many paths that journey can take, and by establishing a plan of action (or inaction!) for when shortfalls inevitably occur.

Ignoring Starting Yields—Nabbing This “Usual Suspect” in Poor Investment Outcomes

Starting conditions matter. Today’s investment yields impact future realized returns. But many still rely on past returns to estimate future returns. Our online Asset Allocation Interactive tool gives you the information you need to look ahead, not just back.

Live from Newport Beach. It's Smart Beta!

Our headquarters in Newport Beach is only 50 miles from the Hollywood studios, although the drive can take up to two hours in rush-hour traffic. But far more than traffic separates the studios’ world from ours.

A Smart Beta for Sustainable Growth

We demonstrate a smart beta that produces positive excess returns from sustainably faster growth in EPS. This simple, systematic strategy represents a significant improvement from today’s growth indices that fail to produce faster growth in EPS and have provided negative excess returns.

Are You Underweight FANMAG? Chillax!

The first half of 2017 is shaping up to be unequivocally brutal for value-oriented rebalancing strategies. Wired to avoid pain, we humans know it’s very tempting to ask whether a model or philosophy is broken, especially the moment it dashes expectations.

CAPE Fatigue

When investors rely on any particular model all the time—and CAPE is often that model—fatigue inevitably sets in. We believe that a better approach for meeting future spending needs is to blend portfolios based on different models of return expectations.

Public Policy, Profits, and Populism

The Trump bump reveals market expectations of continuing public policies prioritizing stability, inhibiting creative destruction, depressing yields and wage growth, and inflating a profits bubble. If instead, the Administration delivers reforms that allow creative destruction, invigorate growth and raise returns to capital and wages, then the lofty profits of corporate incumbents will be at risk.

Presidential Politics and Stock Returns: Is the Relation Real or Spurious?

An analysis of five international stock markets indicates that published findings of a correlation between US stock returns and the political party in the White House are spurious, highlighting the importance of caution in interpreting historical investment data.

Why Factor Tilts Are Not Smart "Smart Beta"

Our analysis of three first-generation smart beta strategies shows factor-replicated portfolios are ineffective substitutes for their smart beta counterparts, exhibiting poorer performance, high turnover, and low capacity.

The Incredible Shrinking Factor Return

In 2016, Research Affiliates published a series of articles challenging the “smart beta” revolution. We pointed out that, while there is merit in many factor tilt and smart beta strategies, performance chasing in these strategies—buying the popular outperforming strategies whose relative valuations are at extremely high levels—can be just as dangerous as performance chasing in other realms of asset management.

Quest for the Holy Grail: The Fair Value of the Equity Market

Macroeconomic volatility is a useful tool for contrarian investors who are seeking fair value in an equity market characterized by continually rising valuations.

Forecasting Factor and Smart Beta Returns (Hint: History Is Worse than Useless)

In a series of articles we published in 2016, we show that relative valuations predict subsequent returns for both factors and smart beta strategies in exactly the same way price matters in stock selection and asset allocation.

A Smoother Path to Outperformance with Multi-Factor Smart Beta Investing

| You can outperform the market with substantially lower relative risk by diversifying across simple smart beta strategies based on a half dozen robust factors. Dynamically rebalancing these factor-based smart betas significantly improves returns. |

How Not to Get Fired with Smart Beta Investing

It may not be my money, but it is my job. — Charles Ellis in Investment Policy: How to Win the Loser's Game

Systematic Global Macro

A quarter-century before Brexit came “Black Wednesday.” On Wednesday evening, September 16, 1992, the British government announced its exit from the European Exchange Rate Mechanism, prompting a dramatic devaluation of the British pound. Renowned hedge fund manager George Soros’ legendary bet against the pound in 1992 and his $1 billion profit on Black Wednesday defines for many the swashbuckling style of a global macro trader.

The Emerging Markets Hat Trick: Time to Throw Your Hat In?

In their latest piece, Rob Arnott and Brandon Kunz of Research Affiliates take a look at how the rare combination of exceptional valuation levels, depressed currencies, and powerful price and economic momentum should encourage long-term investors to “throw their hats” into the emerging markets rink.

Record Low Costs to Trade!

Mean reversion is as applicable to trading costs as it is to valuation. Today’s costs to trade are at 56-year historical lows; they are due to rise soon. Now is the time to position your portfolio ahead of expected higher costs to trade and lower equity prices.

Take the 5% Challenge! (or The “Lloyd Christmas” Lesson)

Now’s the time to get real. Now’s the time, in a world of paltry bond yields and meager dividends, to make an honest assessment of your portfolio’s long-term expected return.