Value equities are still priced for significant outperformance, globally.

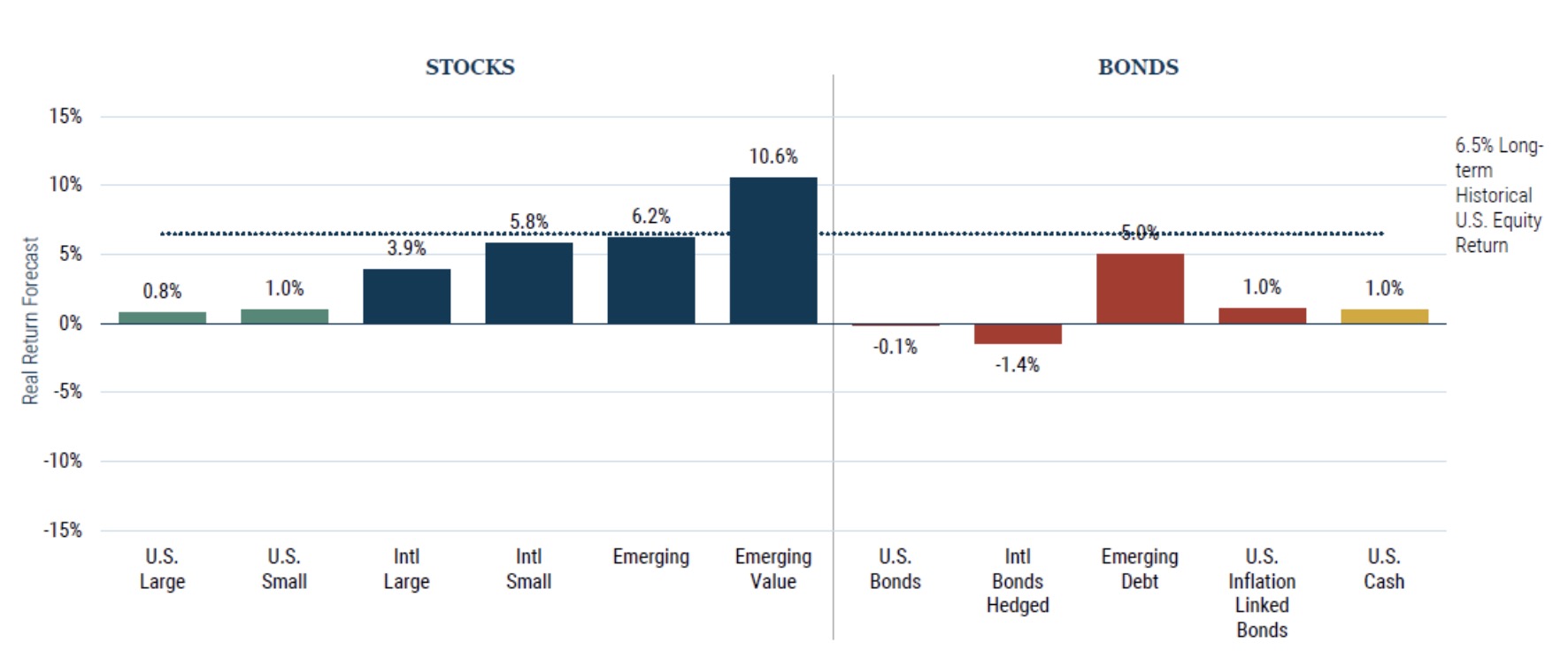

GMO has published a new 7-Year Asset Class Forecast.

Quality investing is an approach well suited to small cap equity.

In this piece, we update our valuation charts and commentary, with additional details on our methodology available upon request.

GMO 7-year asset class forecast: 3Q 2022.

In August 2020, as the global pandemic was straining emerging countries’ ability to make debt payments, we published a white paper – “Sovereign Contingent Bonds: How Emerging Countries Might Prepay for Debt Relief” – introducing the concept of “sovereign coco bonds,” a way for countries to structure bond agreements to allow for more flexible policy options in the face of a crisis.

The world seems an increasingly uncomfortable place for traditional stock and bond investments.

Rising rates hurt investors; claims on profits in the future are simply worth less if you discount them at a higher rate.

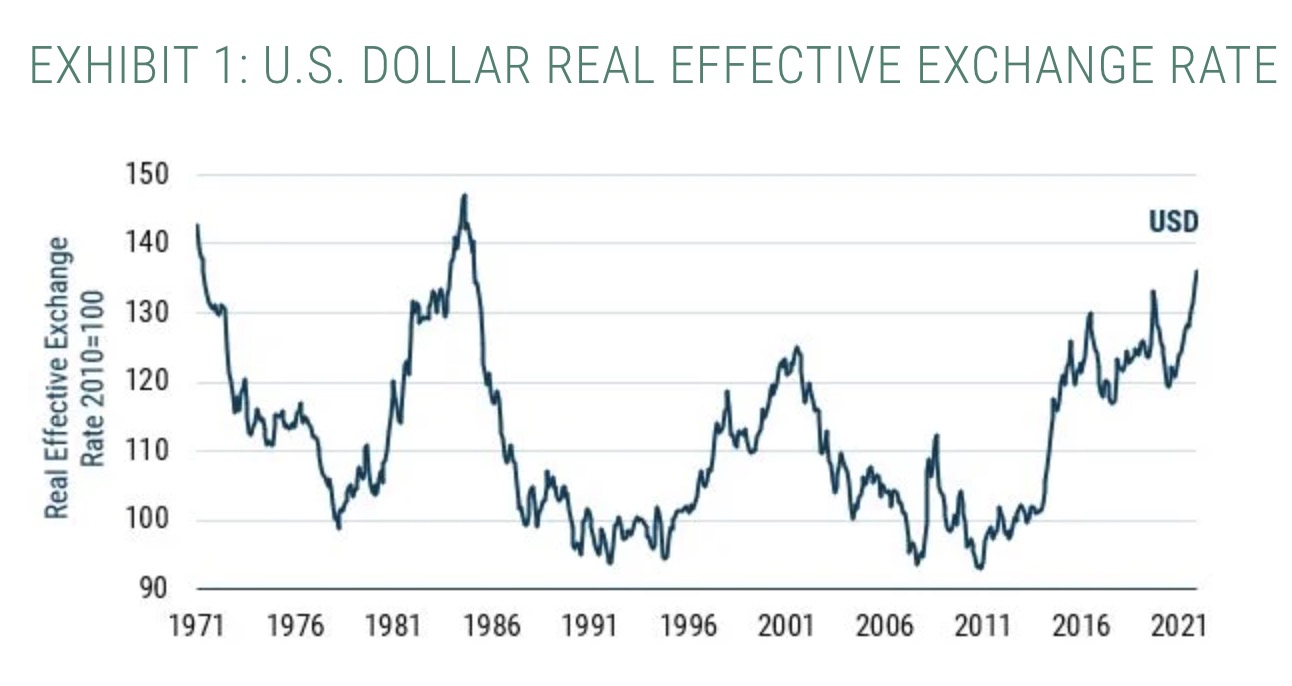

The U.S. dollar has been on a tear in recent months, bringing it to its highest valuation versus other major developed currencies in more than 35 years.

As one of us points out relentlessly, risk isn’t a number, rather it is a notion or a concept.

Only a few market events in an investor’s career really matter, and among the most important of all are superbubbles.

With the recent increases in interest rates, the carry trade has had a sudden resurgence in performance, which could make it a tempting strategy for investors.

Over our decades of involvement in emerging country debt markets, we’ve witnessed many ups and downs.

Rick Friedman from GMO’s Asset Allocation team offers the following comments about the updated forecasts.

As Robert Shiller has written, market participants are always in search of an explanatory narrative. J

The market has spent much of 2022 worrying about inflation and associated interest rate rises, and Growth stocks have certainly borne the brunt of this.

In a new piece, GMO’s Asset Allocation Team notes that even with the battering of growth stocks in 2022 there is still ample opportunity to benefit from betting on cheap value stocks versus expensive growth names.

The yield of the U.S. high yield (HY) market, currently at 8.4%, has risen by over 420 basis points since the start of the year.

Japan has been stuck in a low growth, low inflation (and at times, deflationary) environment.

We strongly believe that the traditional benchmark-led approach to investing in emerging market debt can be far from optimal.

What do Netflix, Peloton Interactive, Coinbase, and Palantir Technologies have in common?

Soaring commodity prices have helped drive inflation to 8.5%, by far the highest level in the last few decades.

Over the past decade it has seemed like Value investors have been very much left on the sidelines, bemoaning rampant speculation and valuations untethered from fundamental reality, while Growth investors have, quite frankly, been living it up in some style.

It’s not just interest rate changes that affect the markets, changes in the Fed balance sheet can also be a source of negative returns to equity and bond markets.

Putin's invasion reminds us that we live in a finite world in which resource prices tend to rise.

Navigating the career risk associated with bubbles (especially superbubbles) has always been tricky and is one of the biggest failings in the investment management industry.

As we turn over the page to a new year, there are plenty of decisions that investors will need to make.

All 2-sigma equity bubbles in developed countries have broken back to trend.

Most global equity managers today are underweight Japan.

This quarterly is a piece written by my Asset Allocation co-head John Thorndike. In it, he explains the rationale behind our strong preference for non-U.S. stocks despite the stellar performance the U.S. stock market has delivered over the last decade. The research behind the piece is an example of the bread and butter of our historical asset allocation analysis.

A new piece from the GMO Asset Allocation Team discusses value traps, growth traps and which are worse for investors.

GMO Asset Allocation team presents a chart of four major U.S. equity bubbles dating back to 1929, illustrating just how long it really takes for investors to climb back to historical levels of return.

GMO Asset Allocation Team examines the fact that although every bubble is unique, classic common threads also run through everyone.

We have a relatively sanguine view on the likelihood of inflation becoming ingrained in the system (much as it pains us to agree with the Fed). However, the dark arts of macroeconomics are notoriously tricky, and we have often talked of the need to build robust (as opposed to optimal) portfolios – effectively, portfolios that can withstand multiple outcomes.

After several strong quarters for value stocks, the last few months have seen a sharp reversal in favor of growth.

Inflation is often a poorly understood concept, with monotheistic explanations abounding.

The Value vs. Growth reversal, which started in earnest in the late Fall of 2020, generated exciting returns for many of our portfolios through May.

The GMO Asset Allocation Team has released its latest 7-Year Asset Class Forecasts through May 2021 (click to view online or see chart below).

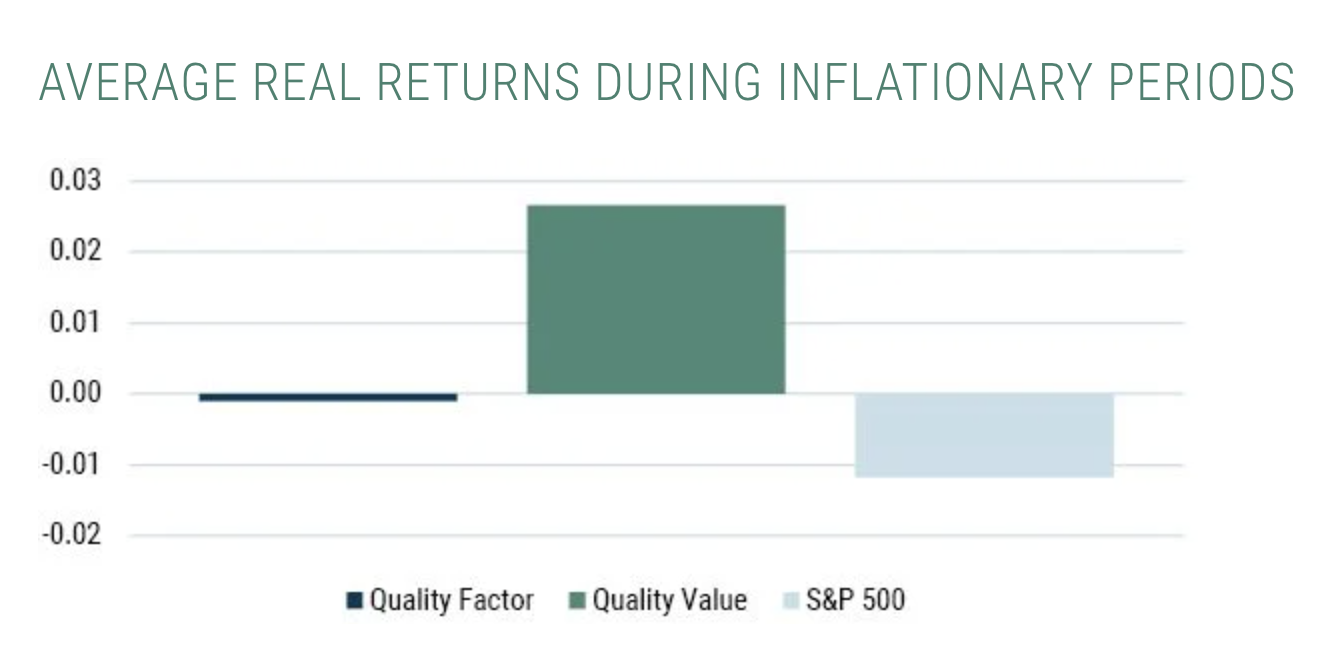

With inflation spiking as the world adjusts to the post-Covid regime, investors are naturally interested in how their portfolios might perform in an inflationary world.

In a new Insights piece, GMO’s Asset Allocation Team addresses a common response to bearishness in the current markets.

Speculative booms provide both entertainment and outsized profits while they are happening, but they do generally burst painfully,” Inker writes. “Speculative booms provide both entertainment and outsized profits while they are happening, but they do generally burst painfully. This is particularly true in equity markets, where the demand growth is ordinarily met with increased supply from savvy capitalists. Maintaining excess demand in the face of growing supply becomes ever more difficult and eventually proves impossible.

April 3rd marked the 1-year anniversary of the first investments deployed by GMO’s Quality Cyclicals Strategy,1 within a fortnight of the trough that ended 2020’s quickfire bear market.

It is commonly assumed that growth stocks are bigger beneficiaries of falling interest rates than value stocks, an assumption driven by a belief that growth stocks are much longer “duration” than value stocks due to the fact that more value in growth companies comes from relatively more distant cash flows.

Global stocks and bonds are both expensive. U.S. stocks are trading at particularly elevated valuations with the CAPE ratio standing at 35x (vs. a 10-year average of less than 27x) while the Barclays Bloomberg U.S. Aggregate index offered a negative real yield at the end of February.

In a new piece from the GMO Event-Driven Team, Doug Francis and Sam Klar discuss the growing supply-demand imbalance in the asset class that has driven focus towards the SPAC boom and away from the opportunity in other investments like merger arbitrage.

The GMO Asset Allocation Team has released its latest 7-Year Asset Class Forecasts through January 2021.

GMO 7-Year Asset Class Forecasts: Value vs. growth is coming off its worst year ever.

Featuring extreme overvaluation, explosive price increases, frenzied issuance, and hysterically speculative investor behavior, I believe this [bull market] event will be recorded as one of the great bubbles of financial history, right along with the South Sea bubble, 1929, and 2000.

While real return forecasts for broader markets are not particularly promising, there are some pockets that look more attractive than others. As GMO put it in the firm's recent Quarterly Letter, "Value is cheap, no matter where you look."

With a COVID-19 vaccine rolling out and markets enjoying a post-election relief rally, credit investors may be asking “is there any opportunity left?”