If you have an aging parent whose bills are starting to be neglected, or a client who needs more hands-on financial oversight than a planner provides, you might consider hiring a daily money manager. The American Association of Daily Money Managers can help you find someone in your area.

Every year, hundreds of thousands of life insurance policies lapse or are surrendered for cash. The policyholders walk away with whatever the carrier offers. Their advisors sign off. Their attorneys see nothing. And nobody asks the obvious question. Could this policy have sold for more?

No one likes that heart-drop feeling of missing an important detail. And yet, this happens all too often when it comes to healthcare planning. Healthcare and health insurance are complex topics. Without an expert or the right resources, it can be very difficult for financial advisors to do on their own.

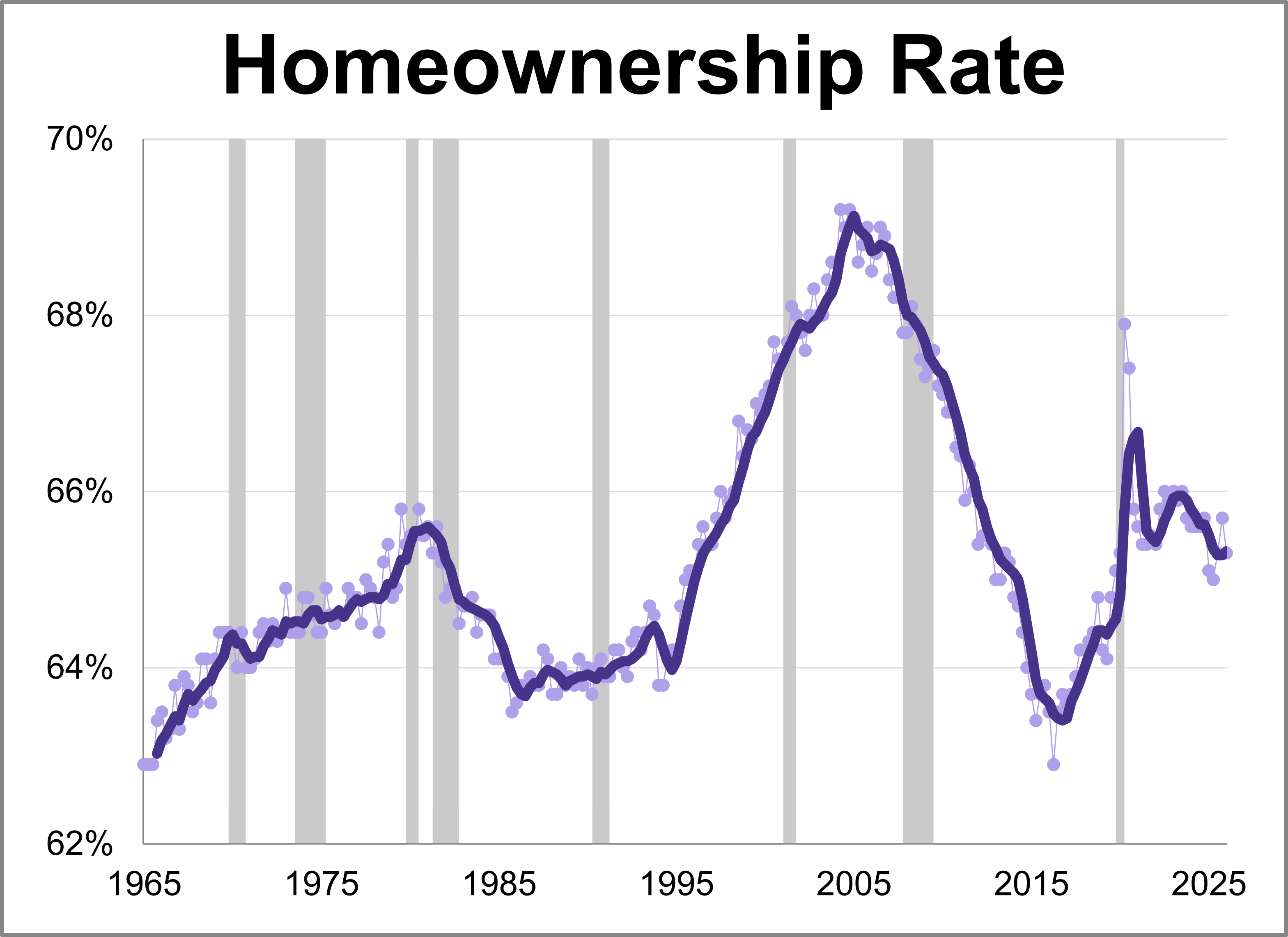

The Census Bureau released its latest quarterly report for Q1 2026 showing the latest homeownership rate is at 65.3%.

Technology megacaps are pushing benchmark indexes to new records while the rest of the market is lagging behind. Traders can be forgiven for feeling like they’ve seen this movie before.

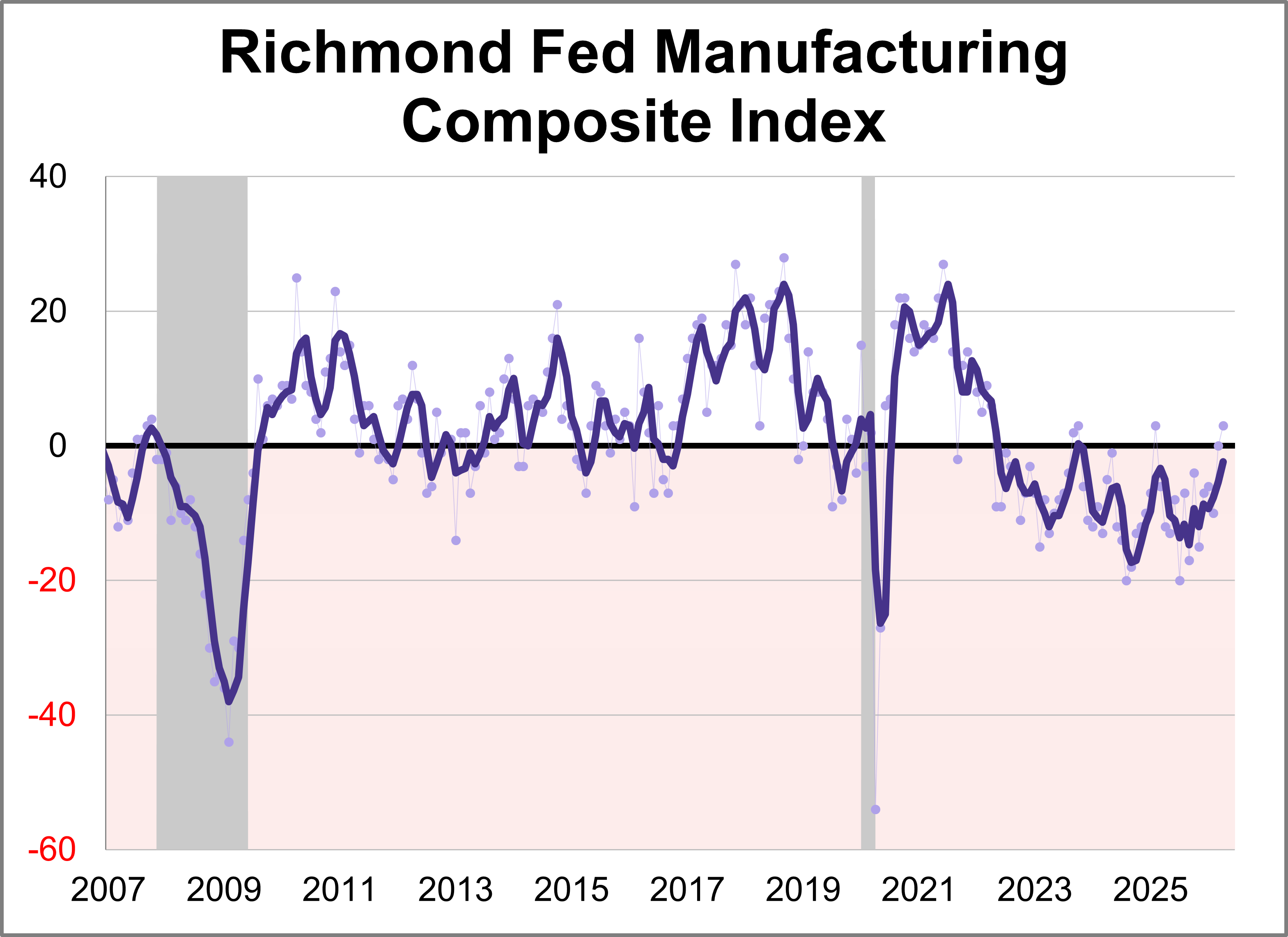

Fifth district manufacturing activity increased in April according to the most recent survey from the Federal Reserve Bank of Richmond. The composite manufacturing index rose three points points to 3, marking the highest level for the index in 20 months. This month's reading was above the forecast of 2.

BlackRock Inc. is bringing its roughly $2.5 billion money market fund to cryptocurrency exchange operator OKX, with Standard Chartered Plc holding the underlying assets — the latest sign that Wall Street infrastructure and digital-asset markets are converging.

European stocks started the year much stronger than their US peers but the tantalizing prospect of the euro area clawing back some of its persistent gap in earnings growth, and the higher company valuations that come with it, looks to have slipped through its grasp again.

The chip industry seems to be the only game in town lately. The Philadelphia Semiconductor Index, known as the SOX, has risen 48% this year. Bourses in Taiwan, South Korea and Japan are riding the wave and hitting record highs, brushing away potential energy shocks from the military conflict over Iran.

The Iran conflict has turned energy markets into a moving target, with oil prices adjusting as expectations around Strait of Hormuz supply risk shift.

In elevated financial markets, risk is rarely eliminated. It is usually only relocated. During the run-up to the 2008 financial crisis, mortgage risk did not disappear. It was transformed, repackaged, and spread across the system in ways that made it appear safer than it was.

The “American Industrial Renaissance” is an investment theme investors and allocators alike have probably been pitched several times, or at the very least heard about. Supply chains for manufactured goods have evolved to become more complex, while U.S. manufacturing employment as a share of total employment has steadily declined, leaving policy makers to grapple with the ramifications of a shrinking manufacturing base.

For all the chatter about Artificial Intelligence lifting economic growth, GDP isn’t showing it yet. We are projecting that real GDP grew at a 2.0% annual rate in the first quarter, matching the average annualized pace of growth since the peak back in late 2007, right before the Financial Panic and so-called Great Recession. In other words, mediocre growth.

Economic data released last week continued to highlight the same tension investors have been grappling with for months: moderating growth, inflation that remains “stuck” near 3 percent, and interest rates that remain the key swing factor for markets.

Cook has spent 15 years focused on the King — the thousands of decisions about industrial design, manufacturing, and supply chains that make the iPhone an iPhone. Racing in AI would have meant counting pieces while leaving the King unguarded. Ballmer counted pieces, and it cost Microsoft $5.5 billion.

Markets continue to ebb and flow with every headline out of Iran and the Strait of Hormuz, but the most important message from the markets is resilience. Earnings season is off to a very strong start, with roughly a 75% beat rate, and the AI investment cycle continues to provide a powerful tailwind for equities.

Many people seem surprised by the US stock market’s resilience during the Iran war. I’m not one of them, and I don’t see the war becoming a significant threat to the market, even if it drags on.

It’s the big story so far in 2026. Alongside AI, geopolitical market volatility is creating dislocations for investors to target. While some are more immediate and some are longer term, the ETF wrapper offers strategies that can attack all kinds of sectors. In corporate bonds, for example, growing volatility could create opportunities.

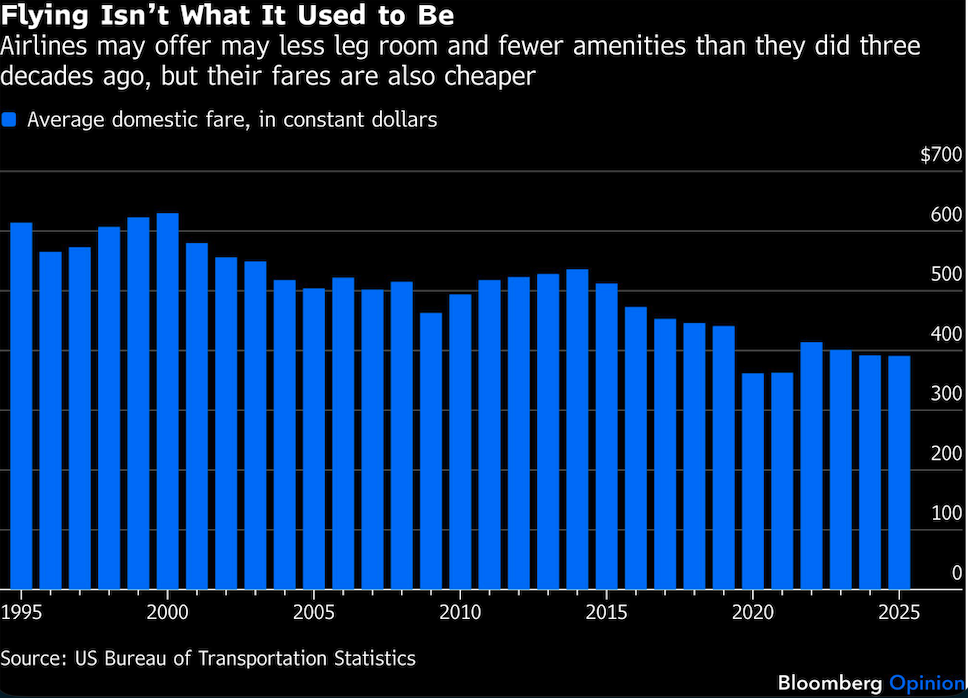

Despite the turbulence, the global LCC market remains an enormous force. Four of the world’s 10 largest airlines—Ryanair, Southwest, IndiGo and easyJet—operate on a low-cost model. The broader budget travel market is projected to exceed $315 billion by 2028, according to Statista.

When silver demand outstrips mining and recycling output, silver users must tap into aboveground stocks. That generally means rising prices to incentivize those holding silver to give it up.

The midstream energy arena, which includes master limited partnerships (MLPs), has long lured income-hungry investors. A new ETF amplifies that proposition. The MLP & Energy Infrastructure High Income ETF (MLPI) debuted last December. It’s generating buzz, helped by the White House’s rhetoric on bolstering American energy independence, which is viewed as a potential boon for MLPs.

The Middle East war has entered a fragile ceasefire, offering tentative relief to energy and financial markets. Oil prices have eased and volatility has subsided, feeding hopes that the worst disruptions may be passing.

Join the experts at Pictet for a product due diligence session covering how PBOT opens portfolios to direct exposure to AI and automation, from semiconductors and software to advanced manufacturing and autonomous systems.

You don’t have to agree with Chater and Loewenstein’s “crowding-out” hypothesis or their policy prescriptions to benefit from It’s on You, which will, at a minimum, allow the reader to identify and deconstruct i-frame PR when they come across it.

With a better understanding of the derivatives and leverage that led to the GFC, we now explore private credit — a small “niche” financial sector, such as subprime mortgages — which is being called the next match to light a financial bonfire.

It’s tax season, and we’ve been reading a lot about taxes — and strategies for mitigating them. In this note, we’ll take a close look at one such strategy, known as leveraged long/short direct index tax-loss harvesting (LSDI), and explain how investors being pitched the strategy can assess whether it’s right for them.

If the first quarter of 2026 taught us anything, it's that markets are dynamic and that the factors shaping them extend well beyond corporate fundamentals. The road ahead presents a wider range of outcomes than investors have faced in some time. The outlook remains fluid and highly dependent on how several key factors evolve.

The world’s most important central banks will potentially hand investors fresh reasons to sell government bonds this week as policymakers find themselves forced to confront the risk of a war-driven inflation shock.

On Monday, the index returned to record highs, eclipsing the previous peak hit before the war started in Iran. Yet, when compared with the US market, emerging-market shares screen as cheaper than at the start of the war, reinforcing the case for investors to add exposure.

United Airlines Holdings Inc. Chief Executive Officer Scott Kirby confirmed he approached American Airlines Group Inc. and that talks have ended, laying out the virtues of a merger that he said could have strengthened corporate America and won approval from regulators.

US stock futures were little changed on Monday after a four-week rally, starting a busy week of corporate earnings and the US central bank’s policy meeting with a relative calm while investors monitor the reopening of the Strait of Hormuz amid stalled Iran peace talks.

A data center developer is seeking $4.54 billion in junk-debt financing for an artificial intelligence project tied to Nvidia Corp., testing investor appetite after a recent surge in offerings.

As of this writing, the Strait of Hormuz remains effectively closed since February 28. Roughly 20% of the world’s seaborne oil stopped moving through the chokepoint. T

As the Q1 2026 earnings season enters its most frantic stretch, the market stands at a critical crossroads between resilient corporate fundamentals and macro-driven anxiety. While the high percentage of early beats suggests that American business remains surprisingly nimble, the coming days will determine if that momentum can withstand the Mag 7’s massive spending requirements.

Like many of you, I am inundated with information. Most of it is not useful or repetitive. Today, were going to do something different. Rather than one theme, let’s look at various bits of data that I found interesting this week.

Leaders often have trouble focusing on the longer-term. In the corporate arena, pressure to produce quarterly earnings can truncate planning horizons. In public life, popular opinion and election cycles can impose myopia. It takes a unique set of ingredients to set, and stick to, a lasting vision.

Congressional confirmation hearings tend to generate far more noise than signal, and this one was no exception. Between politicians posturing for the cameras in hopes of becoming their party’s next rising star, and nominees exercising extreme caution to avoid missteps under oath, these hearings rarely produce actionable insights.

Back-and-forth developments over the weekend around the Strait of Hormuz have added near-term volatility to energy markets. That uncertainty is feeding into oil prices and reinforcing questions about how persistent energy-driven inflation pressures could become, particularly if disruption risks continue to ebb and flow.

Maharrey identified October 2025 as the turning point when a full-scale silver squeeze took hold. Tight inventories collided with logistical disruptions and surging physical demand.

Last week’s economic data was defined by conflicting signals from the consumer. While retail figures suggest resilience, sentiment levels have plummeted to record lows. Meanwhile, the S&P 500 continued its historic rally as markets prepare for the upcoming Fed decision.

After positive earnings releases from peer semiconductors like Texas Instruments, Taiwan Semiconductor, and ASML, it was Intel’s turn to further support the notion that the semiconductor industry is doing just fine amid the recent volatility.

The primary contagion risk is sector concentration. Software and tech-enabled services represent roughly 15-20% of direct lending portfolios. A meaningful portion of these loans also resides in the Broadly Syndicated Loan (BSL) market – the bedrock of CLO ETFs – leading to a software weighting of 12–18% in typical CLO collateral pools.

There’s no shortage these days of stories, posts and videos warning of the robot armies readying to vacuum up white-collar jobs in technology, finance, marketing, you name it. And there’s no doubt that artificial intelligence is rapidly changing how we live and work. Amid all this, though, a relative calm has descended on the labor market and should persist for the rest of this year, at least.

The index is on the verge of doubling for the first time in this bull market – currently up ~99% – a move that would take just under 3.5 years, slightly faster than the historical average of 3.9 years. While all sectors are in positive territory over this period, leadership has been narrow with only three – technology, communication services and industrials – posting gains above 100%.

Budget airlines are going broke. Spirit Airlines may go under or get a government bailout, and JetBlue is just barely avoiding bankruptcy this year. It didn’t need to be this way. They tried to merge in 2024, but the merger was blocked because President Joe Biden’s administration was concerned that greater consolidation would lead to higher prices.

The bigger the vacuum becomes, the longer it will take to refill those inventories whenever whatever passes for normality finally arrives. Oil prices along the curve would need to rise accordingly to encourage excess production — or, conversely, achieve the same outcome by destroying demand.

Clients may love the relative safety of cash, but many advisors know those assets could do more. A multisector bond approach for example, offers plenty of rewards for those willing to dive in. The right ETF can give tax efficient exposure to the space, providing both yield and total return.

Even before the first active dual share class fund from Dimensional launched, active mutual funds and ETFs were already roommates rather than existing in separate silos. Ben Johnson, head of client solutions at Morningstar, revealed in a LinkedIn post that active managers are increasingly using ETFs as essential tools for building portfolios.

Elon Musk’s SpaceX is no stranger to the stratosphere, and neither is its coming initial public offering.

As a more than $20 billion borrowing frenzy to build out data centers descended on the junk-bond market this year, some issuers offered up a rare sweetener: an early cash payback.