U.S.-listed ETFs locked in a record-breaking first half of the year. Read the analysis on active ETFs, fixed income shifts, and equity flows.

Former Fed Chair Alan Greenspan’s passing has brought a stream of retrospectives on his approaches to managing the economy. He erred on the side of parsimony, favoring short public statements. Greenspan’s vague communication style offered little clarity over the future path of interest rates.

The second quarter wraps up today, and it was a good one. With the S&P 500 having returned more than 14% (including dividends) with just one trading day left, it will almost certainly end up being the best quarter for the index since the second quarter of 2020. Technology was the leader despite the June weakness.

The Mag 7 has been the single largest driver of the stock market’s performance three straight years, accounting for over 20% of the S&P 500’s performance. However, there is a performance divergence happening in 2026 as the S&P 500 continues to go up, while the Mag7 go down.

A look at the resilient global economy, evolving market opportunities, and key risks shaping the investment outlook.

At first glance, allocating to emerging markets appears to add diversification to a portfolio. Look more closely, and the reality is more nuanced. In the late 1990s, the MSCI EM index was dominated by materials and telecoms, driven by the growth of mobile telephony and the internet bubble.

Markets weathered turmoil in the first half, helped by solid earnings with signs of broadening beyond a few AI beneficiaries. If the war in Iran eases, oil prices could normalize, reducing inflation pressure. Still, growth, inflation and policy risks may be underestimated.

Global stocks surged during the second quarter as oversold conditions in March and de-escalation in the Middle East created ripe conditions for a rally. In the United States, the large-cap S&P 500 index climbed by 13%, while the small-cap Russell 2000 index increased by nearly 25% (yCharts).

There’s no doubt the most important aspect to the June FOMC meeting was the fact that policymakers kept the Fed funds rate unchanged and removed its prior easing bias. But, this was not just your normal, run-of-the-mill policy gathering. It was Kevin Warsh’s first meeting as Fed Chair and instead of being a ‘rubber stamp’ for rate cuts, as some market observers were opining, the new FOMC leader put his stamp on the Fed in a different way.

June saw strong market fundamentals once again in conflict with macroeconomic uncertainties, creating a choppy market. While a durable peace plan with Iran is seemingly underway, investors have regarded the negotiations with caution, pricing in potential setbacks.

Markets may have ended the first quarter with a thud, but stocks put another record run in the books to close out the first half of 2026. The U.S. ETF market had already shattered records, crossing the $15 trillion threshold and cruising past $1 trillion in net inflows right before summer officially began.

It’s been a long time coming for the asset management world, but ETF share classes are now a reality. Fidelity Investments has joined that movement, with the launch of its first ETF share classes for some of its mutual funds.

As growth stumbled, the S&P 500 Momentum Index captures a 7.5% gain in June and a 44% gain in the second quarter.

While the Middle East is still far from calm, it does appear the worst of the volatility in the region is in the past. The U.S.-Iran ceasefire is in place, with negotiations underway for a more durable peace.

A strong quarter across major indexes. The second quarter is winding down and what a quarter it has been with the S&P 500 up 12.6% quarter to date, while the Nasdaq-100 and Russell 2000 are both up over 20%. Despite some twists and turns, the path of least resistance for stocks broadly remained up and to the right for much of the last three months.

Startup equity decisions often happen before a founder has a full advisory team in place. Formation documents get signed, vesting schedules are approved, and the tax consequences may not feel urgent because the company is still young.

In our view, this divergence continues to reflect how the buildout of artificial intelligence (AI) is influencing both the economy and markets as it progresses across the value chain, even as the associated costs continue to climb.

The sharp retreat in oil prices has dramatically altered the market narrative. Just weeks ago, investors feared a renewed inflation shock from the conflict with Iran. Instead, crude has fallen back toward pre-conflict levels, Treasury yields have declined, and markets have begun rotating aggressively away from the large tech hyperscaler, the Magnificent Seven, that dominated recently and toward more cyclical and value-oriented sectors.

Benchmarks are broken. That was the premise established in a conversation with Samarth Sanghavi, head of fixed income index product at TMX VettaFi, when the problem was first addressed in a previous article. TMX VettaFi creates innovative index solutions, and with the premise established that benchmarks are indeed broken, here is the fix.

Geopolitics, artificial intelligence, and inflation each took their turn commanding market attention last week. U.S. equities were mixed, as a pullback in technology names masked broadening performance beneath the surface.

Insurance investors face a broader opportunity set than ever across public and private credit—from corporate lending to asset-based finance. But those investments come in many forms. In our view, a all-encompassing approach can better assess relative value, pivot to new avenues and align investments with portfolio, liability and regulatory considerations.

For decades, financial advisors have built strong relationships by helping clients manage IRAs, taxable accounts, and rollover assets after they leave an employer. Meanwhile, a significant, often the largest pool, of client wealth has quietly remained out of reach: assets inside workplace retirement plans.

The ETF ecosystem is always changing and growing. Thanks to the ETF’s flexibility, transparency, and tradability, it can help investors achieve plenty of bespoke goals. That even includes investing with an eye towards philanthropic causes as with philanthropic ETFs ASD and DUTY.

The money is REAL. The question was never whether it exists. It’s who’s spending it, and what they borrowed to do it. When the wall of cash and the bottom half finally commit to risk at the same moment the Fed turns hawkish, that’s not the start of something. That’s the part of the cycle where the careful investor gets paid to be careful.

Ten years ago this week, the world watched the United Kingdom vote to walk away from the European Union. While the political class was clutching its pearls and every talking head on television was promising Armageddon by Christmas, I told you something different.

Alan Greenspan passed away last week at the ripe old age of 100. Other than presidents, few Americans have wielded as much power in the arena of economic policy as Greenspan did during his roughly eighteen years and five months at the helm of the Federal Reserve.

Chris Galipeau discusses high-conviction insights that go beyond media headlines.

Despite strong gains in 2026 so far, commodities have remained supported by constrained supply, resilient demand and long investment lead times, pointing to a cycle that seems to remain fundamentally intact.

Whether you’re a seasoned RIA owner looking to accelerate organic growth or a next-gen Advisor building your practice from the ground up, the same fundamentals apply: say clearly who you help, show up consistently where prospects look, and make sure your online presence tells the right story.

Investing is hard enough - This video explains why avoiding overpaying for stocks is one of the most important principles of successful long-term investing. Chuck Carnevale argues that while investing is never risk-free, many costly mistakes can be avoided by understanding a company's intrinsic value rather than reacting to market emotions.

A widening confidence gap in non-traded investment vehicles is testing private credit valuations, sharpening the case for manager selection and diversification beyond direct lending.

It’s hard to believe we’re nearing the halfway point of 2026 – and what an eventful start it’s been. Markets have pushed through a geopolitically driven energy shock, rising inflation pressures and accelerating disruption from the artificial intelligence boom.

AI infrastructure spending is driving record equity market raisings and has lifted expectations for long-term GDP growth in the US. But what will happen to growth when the AI capex surge has peaked? Today’s elevated long-bond yields suggest that the market expects AI-related productivity gains to support faster growth over the longer term.

What has started to stand out more recently is not the opportunity itself, but the behavior forming around it. The conversation has shifted. It is no longer centered on understanding what is being built or how it will be monetized over time.

The top 10 active ETFs YTD by fund flows show some intriguing trends and successful names that may pique the interest.

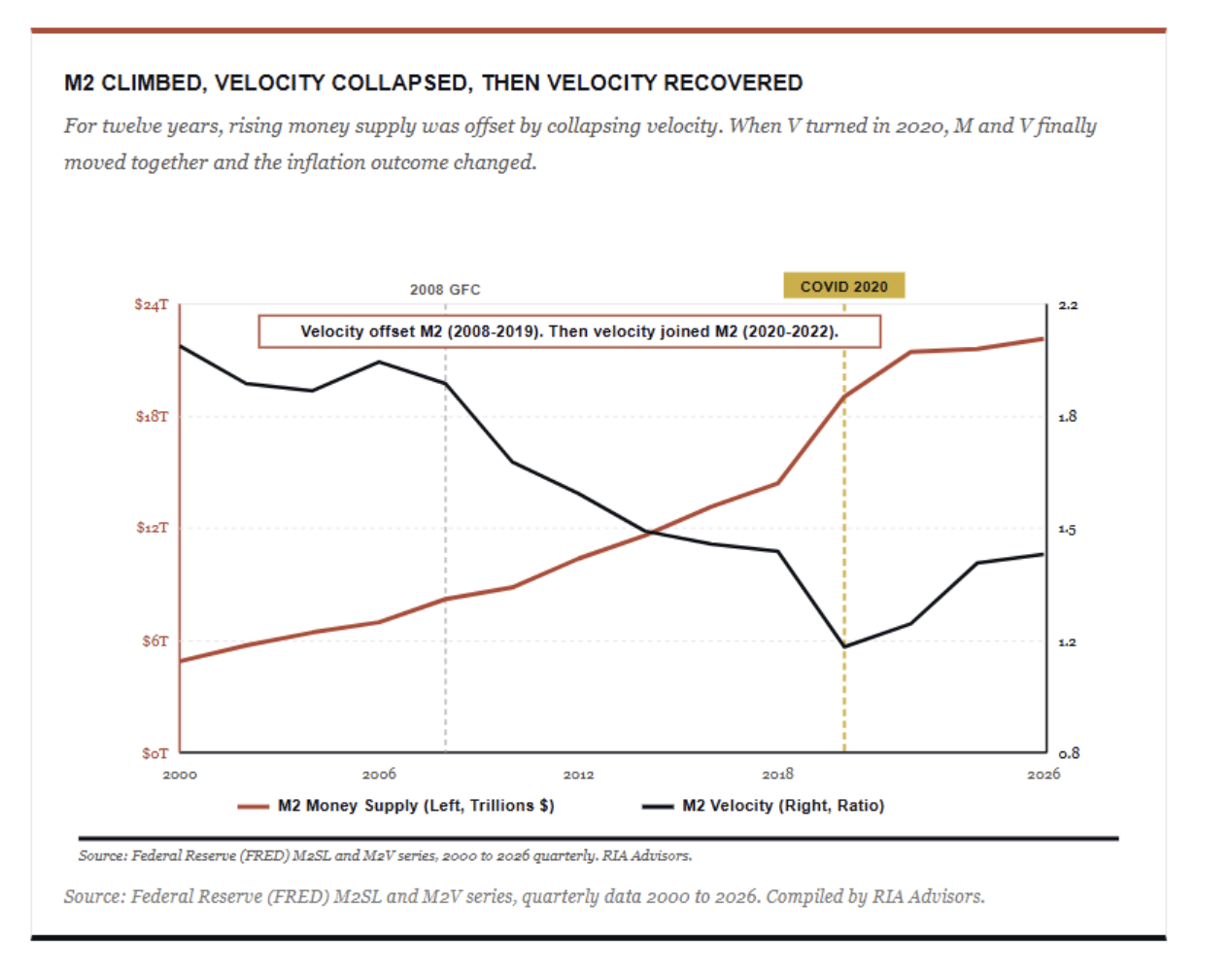

Friedman was reasoning from the equation of exchange, MV = PQ. Money times velocity equals prices times real output. It’s an identity, not a theory. Where it gets interesting is when you ask which variable does the work.

Transformative new technologies and geopolitical tensions have become powerful disruptive forces, redefining business models, global supply chains and the economy. These seismic shifts are upending competitive dynamics across industries and drawing trillions of dollars in capital flows that we believe are reshaping the sources of long-term equity returns.

The dominant theme this week was a tug of war between improving macroeconomic conditions and weakness in parts of the technology sector.

From our experience participating in Fed meetings, we know that the dot plot has never been universally embraced within the institution. The concern was not that it lacked informational value, but rather that markets interpreted it as a forecast, which was never its intended purpose. Forward guidance is meant to shape expectations and influence behavior, not to serve as a firm prediction of future policy decisions.

Markets have been hyper-focused on AI, crypto and buffer ETFs, but REIT ETFs have quietly staged an impressive comeback. The REIT terrain has shifted rapidly over recent years, and forward-looking investors and advisors have taken notice.

As expectations have shifted toward slower growth, higher inflation, and higher rates, investors have rotated back to sectors like large-cap technology and semiconductors, capable of delivering durable earnings in a tougher macro environment.

Circumstances since 2020 have repeatedly demonstrated how adaptable the economy is in the face of new challenges. We see no reason for that resilience to fade in the balance of the year.

During the past month, the ETF market has seen a wave of excitement surrounding a concentrated group of companies. While investors still want exposure to the tech giants that have dominated the past few years, the successful launch of SpaceX in early June created widespread anticipation for planned IPOs like Anthropic and OpenAI.

Last week’s data reaffirmed that inflation pressures remain the defining narrative across the economic landscape.

I’m hopeful new chair Kevin Warsh will help change the Fed’s inflation-tolerating institutional culture. Early signs look positive. Today we’ll talk about how insidious inflation is and why those who think a little inflation is fine should have their heads examined. It is not fine… for anyone.

The AI boom goes from strength to strength. Big technology companies are pouring hundreds of billions of dollars into chips, data centers and power-hungry infrastructure. One estimate puts annual AI infrastructure investment above $650 billion in 2025 and potentially over $800 billion in 2026..

Model portfolios have helped many advisors solve for scale. The next challenge is more nuanced: how do advisors keep that scale while delivering more personalization, tax awareness and differentiated value to clients?

Before your firm starts using AI across operations, client service, reporting, or advisor workflows, there’s one basic question leadership needs to answer: what kind of AI are we talking about?

Investors now have more optionality when looking for Nasdaq 100 exposure. State Street Investment Management (SSIM) just launched the State Street SPDR Portfolio Nasdaq 100 ETF (QNDX). It will invariably go heads up with the Qs, namely the Invesco QQQ ETF (QQQ) and the Invesco NASDAQ 100 ETF (QQQM).

Private credit is having a moment in the headlines. Higher interest rates and a pullback in certain types of bank lending have pushed more financing activity into private markets. Investors may be left with a simple question: What exactly is private credit?